FHA vs VA Loan Michigan: Your 2026 Homeownership Flight Plan

You might assume a zero-down VA loan is the only way to fly, but in the shifting 2026 market, the most efficient route to a West Michigan home isn’t always the most obvious one. When comparing an FHA vs VA loan Michigan, many buyers feel stuck in a holding pattern of high interest rates and complex mortgage insurance rules. It’s natural to feel some turbulence when looking at the new MSHDA income limits for Kalamazoo County or worrying if a dip in your credit score will ground your homeownership dreams before you even reach the runway.

I understand that you want the most lift for your money without being weighed down by unnecessary fees. This guide provides your 2026 homeownership flight plan, stripping away the jargon to help you secure the best financing for your life in Portage or Battle Creek. We’ll examine the latest 2026 loan limits, explain how to navigate “hidden” insurance costs, and show you how to pair these government-backed programs with Michigan assistance for a perfectly timed landing.

Key Takeaways

- Identify your eligibility for government-backed financing by understanding the specific requirements for veterans and first-time Michigan homebuyers.

- Compare the “lift” of a 0% down VA loan against the 3.5% down payment of an FHA mortgage to find the right FHA vs VA loan Michigan strategy for your savings.

- Discover how MSHDA programs can provide the momentum needed to cover down payments, effectively creating a zero-down path for FHA buyers.

- Contrast the ongoing costs of FHA mortgage insurance with the one-time VA funding fee to ensure your monthly budget stays on course.

- Follow a clear, step-by-step flight plan to navigate 2026 income limits and secure the best mortgage for your West Michigan home.

The Pre-Flight Briefing: Understanding FHA and VA Loan Mechanics in Michigan

Buying a home in 2026 feels different than it did just a few years ago. In West Michigan, where inventory remains tight and interest rates require careful planning, choosing between an FHA vs VA loan Michigan isn’t just a paperwork decision; it’s about selecting the right propulsion for your financial future. Both programs are government-backed, meaning the federal government provides a safety net for your lender. This “insurance” reduces the risk for banks, allowing them to offer you more favorable terms, lower down payments, and more flexible credit requirements than a traditional conventional loan. In today’s market, these programs act as the wind beneath your wings, making homeownership attainable even when economic conditions feel heavy.

The VA Loan: A Benefit Earned Through Service

For those who’ve served, the VA loan is the gold standard of mortgage financing. It isn’t just a loan; it’s a hard-earned benefit for active-duty members, veterans, and eligible surviving spouses. The primary advantage is the ability to achieve full lift with zero down payment. To start this journey, you’ll need your Certificate of Eligibility (COE), which proves to lenders that you’ve met the service requirements. In the 2026 Michigan market, this zero-down feature is a powerful tool, allowing veterans to keep their cash reserves for moving costs or home improvements rather than locking every cent into the foundation of the house.

The FHA Loan: Accessible Lift for All Michigan Buyers

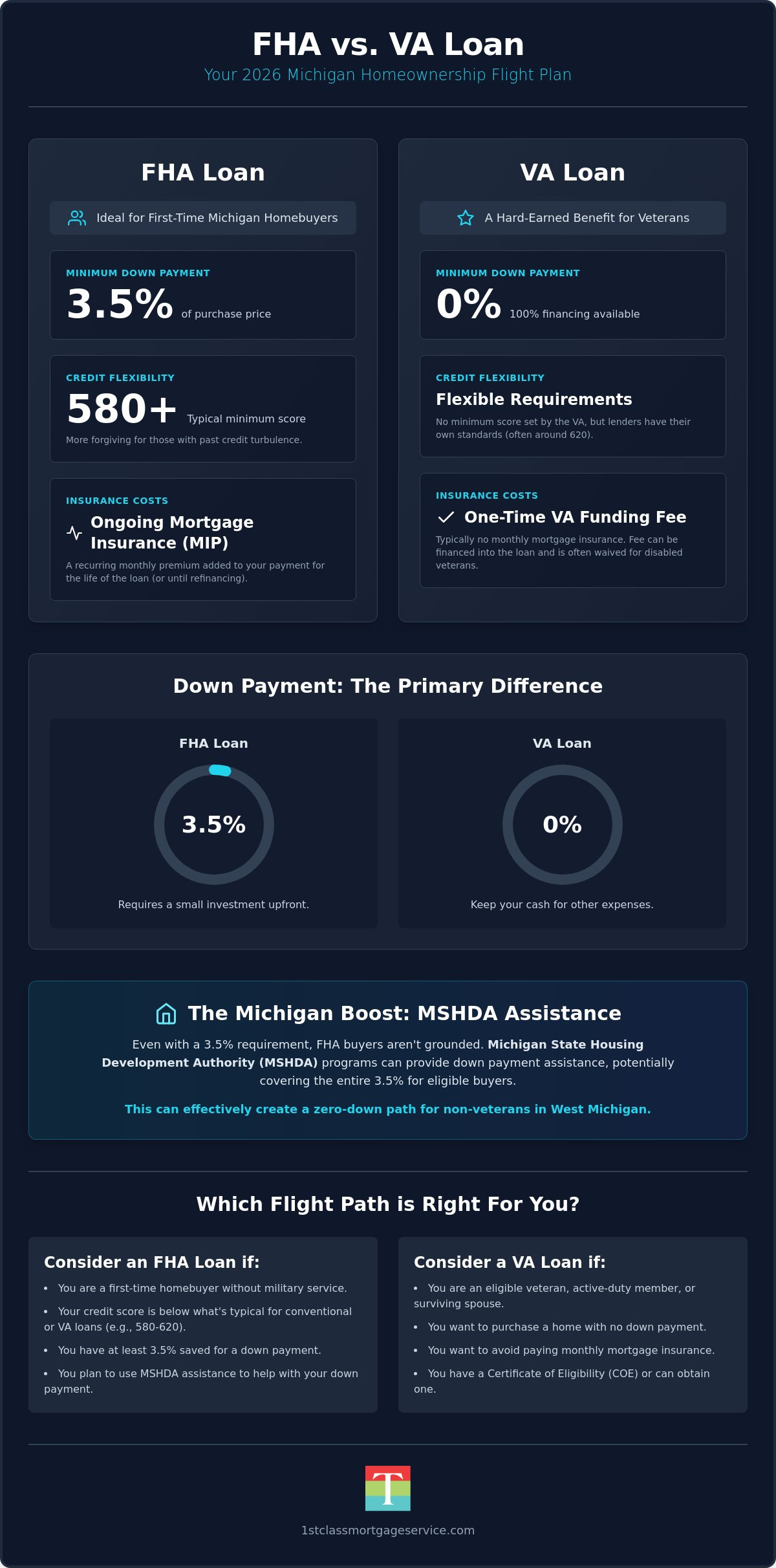

If you haven’t served in the military, the FHA insured loan remains the most popular alternative for securing a home. These fha loans michigan are designed to help residents who might face credit turbulence or don’t have a massive pile of cash for a down payment. With a minimum requirement of just 3.5% down, the FHA path is a low-weight entry point into homeownership that doesn’t require a perfect financial history to clear the runway.

In places like Kalamazoo and Portage, the FHA program is often the first choice for first-time buyers because the guidelines are more forgiving. If your credit score has seen some turbulence, the FHA’s flexible thresholds often allow for a safe landing when other programs might deny your application. When you’re weighing an FHA vs VA loan Michigan, remember that while the FHA requires a small down payment, it opens the door for a much wider range of borrowers to enter the cockpit of homeownership. This accessibility ensures that more families in our community can achieve the milestone of owning a home without waiting years to build a perfect credit profile.

Lift vs. Drag: Comparing Down Payments and Credit Requirements

Every pilot knows that weight impacts how quickly you can get off the ground. In the mortgage world, your down payment is that weight. If you’re weighing an FHA vs VA loan Michigan, the most immediate difference is how much cash you need to bring to the cockpit on closing day. For eligible veterans, the VA loan offers 100% financing, meaning you can achieve lift with zero down payment. This is a massive advantage in the 2026 Michigan market, where saving for a traditional deposit can feel like fighting a constant headwind while prices in areas like Kalamazoo and Portage continue to climb.

The Zero-Down Advantage of VA Loans

The ability to secure a home without a down payment changes your entire financial trajectory. While there are other zero down payment home loan alternatives in Michigan, such as USDA loans or specific assistance programs, the VA loan remains unique because it doesn’t typically require monthly mortgage insurance. You should review the Official VA Loan Eligibility Requirements to ensure your service time meets the current standards for 2026. Some buyers wonder if 0% down is always the best move. While it preserves your cash for emergencies or home repairs, it does mean you’ll start your journey with less equity. If you have the funds, putting even a small amount down can reduce your monthly payment and lower your overall interest costs over the life of the loan.

Credit Flexibility in the FHA Flight Path

If your credit history has experienced some turbulence, the FHA loan provides much sturdier landing gear. In 2026, FHA guidelines generally allow for a 3.5% down payment with a credit score as low as 580. Think of your credit score like the visibility on a runway. While a perfect score makes for an easy approach, FHA guidelines provide the sophisticated instruments needed to land safely even when your financial “weather” is less than ideal.

Local West Michigan expertise is vital when navigating these requirements. Unlike a national call center that might ground your application based on a single automated scan, a neighborly lender can help you analyze credit “turbulence” and find a path forward. We view your credit as a journey rather than a fixed point. If you’re worried about your debt-to-income (DTI) ratio, both FHA and VA loans allow you to carry more “cargo” (monthly debt) than conventional loans. This flexibility is often the difference between a rejected application and a successful takeoff. If you’re ready to see how much cargo your financial flight plan can carry, talking to a mortgage specialist in Kalamazoo can help you map out the most efficient route for your budget.

Navigating the Michigan Landscape: MSHDA Boosts and Local Nuances

While the national rules for an FHA vs VA loan Michigan provide a solid baseline, the local terrain in West Michigan offers unique boosters that can change your entire trajectory. If you aren’t eligible for a zero-down VA loan, don’t assume you’re grounded by a large down payment requirement. By utilizing michigan first time home buyer programs, you can often bridge the gap. These state-level initiatives act like an auxiliary engine, providing the necessary thrust to overcome the initial cost of entry into the housing market.

One of the most powerful maneuvers for FHA buyers is the MSHDA MI Home Loan program. In 2026, this program offers up to $10,000 in down payment assistance. For a borrower looking at a home in Kalamazoo or Battle Creek, this assistance can cover the entire 3.5% FHA down payment. This creates what we call a “synthetic” zero-down loan. It allows non-veterans to compete on similar footing with VA buyers who already enjoy 100% financing. Understanding these FHA vs. VA Loan Differences is essential for choosing the path that preserves your cash reserves without sacrificing your ability to buy in a competitive neighborhood.

MSHDA Down Payment Assistance: The Extra Engine

The $10,000 MI Home Loan boost isn’t just a financial tool; it’s a stabilizer for your flight plan. To access this, you’ll need to stay within specific 2026 income limits for Kalamazoo and Calhoun counties. Working with a MSHDA-certified navigator like Jeremy Drobeck is critical here. These programs have specific flight paths regarding credit scores, requiring a minimum of 640, and property price ceilings. In Portage and Battle Creek, these limits are designed to keep homes affordable, but they require precise navigation to ensure your application doesn’t veer off course during the underwriting process.

Appraisal Turbulence in West Michigan

Our local landscape is dotted with beautiful, historic neighborhoods, particularly in the Vine or Westnedge Hill areas of Kalamazoo. These older homes often come with “Minimum Property Standards” challenges for both FHA and VA loans. Common inspection hurdles include peeling exterior paint or missing handrails on steep basement stairs. Sellers sometimes fear these government-backed loans because of these strict safety requirements.

This is where your choice of lender acts as your co-pilot. We don’t let a bit of peeling paint ground your deal. By identifying these issues early and negotiating repairs with the seller, we keep your flight on schedule. A seasoned local expert knows how to communicate these requirements to sellers and listing agents, turning potential “no-go” situations into a successful landing for everyone involved. Whether you’re choosing an FHA vs VA loan Michigan, having a navigator who knows the local housing stock is just as important as the loan program itself.

Managing Mid-Flight Costs: Mortgage Insurance and Funding Fees

Every long-haul flight requires a calculation of fuel efficiency and maintenance costs. When comparing an FHA vs VA loan Michigan, you must look beyond the initial takeoff to see how much your mortgage will cost over the duration of the journey. While both programs offer excellent accessibility, they handle “insurance” costs in very different ways. FHA loans carry an ongoing maintenance fee in the form of mortgage insurance, while VA loans typically favor a one-time upfront cost. Understanding these mechanics helps you determine which path offers the most stability for your 30 year flight plan.

The FHA MIP Trap vs. VA Savings

The FHA program uses a two-tiered insurance system to protect lenders. First, there’s the Upfront Mortgage Insurance Premium (UFMIP), which is 1.75% of your loan amount in 2026. Most Michigan buyers choose to roll this into their total loan balance rather than paying it at closing. Second, you’ll face an annual Mortgage Insurance Premium (MIP), usually around 0.55% for most borrowers. This is the “MIP trap” many talk about. If you put down less than 10%, this monthly fee stays with you for the entire life of the loan. It never drops off automatically, even as your equity grows.

VA loans offer much cleaner air for your monthly budget because they have zero monthly mortgage insurance. Instead, you pay a one-time VA Funding Fee. For a first-time user with no down payment in 2026, this fee is 2.15%. While it adds to your initial balance, the lack of a monthly insurance bill means your “burn rate” is much lower. Over a decade of homeownership in Kalamazoo, the savings from avoiding monthly insurance can amount to tens of thousands of dollars. When you factor in that current mortgage rates for VA loans are often the most competitive in the market, the long-term cost advantage for veterans becomes clear.

Exemptions and Stability

There are ways to bypass these “takeoff fees” entirely. Veterans receiving compensation for a service-connected disability are exempt from the VA Funding Fee, making the VA mortgage the most cost-effective financial vehicle available. Even for those who aren’t exempt, we often use a “Navigator” strategy to negotiate seller concessions. In Michigan’s 2026 market, sellers can contribute up to 4% of the purchase price toward a VA buyer’s closing costs, which can effectively cover that funding fee for you.

Think of closing costs like the weight of your cargo. If the seller helps carry that load, your flight becomes much easier to manage. FHA loans also allow for seller concessions, but the ongoing monthly MIP remains a fixed cost of your flight. If you’re ready to see a side-by-side comparison of your monthly payments, contact our West Michigan office to run a custom flight plan for your specific budget.

Safe Landing: How to Choose the Right Michigan Mortgage Path

Bringing your homeownership journey to a successful conclusion requires a final look at your flight instruments to ensure you’ve chosen the correct approach. Deciding between an FHA vs VA loan Michigan comes down to your personal history and your current cash position. If you’ve served in the military, the VA path is almost always the most efficient route due to its zero-down requirement and lack of monthly mortgage insurance. However, if you haven’t served, or if you need to stay within the 2026 MSHDA income limits for Kalamazoo County to secure down payment assistance, the FHA route provides the necessary lift to reach your destination.

To finalize your decision, follow this four-step sequence for a safe landing:

- Step 1: Confirm Eligibility. Veterans and active-duty members should prioritize the VA benefit. All other buyers should look toward FHA as their primary vehicle.

- Step 2: Evaluate Cash Reserves. If your savings are low, check if you qualify for the $10,000 MSHDA boost. This can stabilize an FHA flight plan by covering the down payment.

- Step 3: Analyze Credit Health. Both programs handle turbulence well, but FHA is particularly forgiving for scores in the high 500s.

- Step 4: Consult Your Navigator. A local expert can run the numbers for both paths to see which one saves you more money over the next 30 years.

The Jeremy Drobeck – Treadstone Mortgage Advantage

Choosing the right loan is only half the battle; you also need a co-pilot who knows the local terrain. Jeremy Drobeck – Treadstone Mortgage, a division of Neighborhood Loans, Inc. (NMLS #222982), brings over 20 years of local lending experience to your cockpit. Unlike national lenders who view you as a transaction, we provide neighborly reassurance throughout the entire process. We are MSHDA-certified specialists who understand the specific nuances of the Kalamazoo, Portage, and Battle Creek markets. We stay in the cockpit with you from the initial pre-approval until you have the keys in your hand, ensuring total transparency and a stress-free experience.

Final Flight Checklist

Before you start touring homes in Westnedge Hill or Portage, you need your “Clear to Takeoff” signal. This starts with a robust pre-approval. This document proves to sellers that your financing is engineered for success. You’ll also want to decide if a standard Purchase Mortgage fits your needs or if you require a renovation loan to update an older property. Whether you’re weighing an FHA vs VA loan Michigan or exploring other assistance programs, the goal is a safe landing in a home you love. Let’s map out your 2026 flight plan together and turn your homeownership dreams into a reality.

Clear the Runway for Your West Michigan Home Purchase

Your 2026 homeownership journey doesn’t have to be a solo flight through heavy fog. Whether you choose the zero-down efficiency of a VA loan or the accessible lift of an FHA mortgage paired with MSHDA assistance, you now have the instruments to make an informed decision. We’ve explored how the right choice between an FHA vs VA loan Michigan can save you thousands in monthly insurance costs and how local expertise helps you navigate appraisal hurdles in Kalamazoo’s historic neighborhoods.

Choosing a mortgage is a significant life milestone that requires precision and a steady hand. At Treadstone Mortgage, a Division of Neighborhood Loans, Inc. (NMLS #222982), we provide more than just numbers; we offer neighborly support from our local Kalamazoo office. As a MSHDA Certified Specialist, Jeremy Drobeck is ready to stay in the cockpit with you from takeoff to landing. Don’t let credit turbulence or complex income limits ground your dreams.

Chart your course to homeownership with Jeremy Drobeck today and secure the financing that fits your unique flight plan. We’re ready to help you land safely in your new West Michigan home.

Frequently Asked Questions

What is the minimum credit score for an FHA vs VA loan in Michigan for 2026?

In 2026, the minimum credit score for an FHA loan with 3.5% down is typically 580, while VA loans technically have no set minimum score from the government. However, most local lenders look for a score of at least 620 to ensure a stable flight path. If you’re comparing an FHA vs VA loan Michigan, remember that pairing either with MSHDA assistance requires a minimum score of 640 to clear the runway.

Can I use MSHDA down payment assistance with a VA loan in Kalamazoo?

Yes, you can combine MSHDA down payment assistance with a VA loan for your Kalamazoo home purchase. Even though VA loans allow for 100% financing, MSHDA’s $10,000 MI Home Loan program can be utilized to cover your closing costs or prepaid items. This strategy preserves your cash reserves for home improvements or emergencies, giving your financial plan extra stability during the initial takeoff phase of homeownership.

Is an FHA loan better than a VA loan if I have a high down payment?

A VA loan is almost always more cost-effective than an FHA loan, even with a high down payment. This is because VA loans don’t require monthly mortgage insurance, whereas FHA loans typically require mortgage insurance for the entire loan term if you put down less than 10%. Unless you aren’t eligible for VA benefits, the long-term savings of avoiding monthly insurance premiums make the VA flight path much lighter on your wallet.

How much is the VA funding fee in 2026?

For 2026, the VA funding fee for a first-time user with zero down payment is 2.15% of the total loan amount. This fee increases to 3.3% for subsequent uses, though it can be reduced if you provide a down payment of 5% or more. Veterans with a service-connected disability or certain surviving spouses are often exempt from this fee entirely, allowing for a much lower cost of entry into the West Michigan market.

Are FHA or VA loan rates lower in Michigan right now?

VA loan rates are generally the lowest in the Michigan market, often sitting slightly below FHA and significantly below conventional rates. Both FHA and VA programs provide better interest rate stability because the government backing reduces the risk for your lender. When navigating an FHA vs VA loan Michigan, the lower interest rate of the VA loan combined with the lack of monthly insurance usually results in the lowest monthly payment available.

What property types qualify for FHA vs VA loans in West Michigan?

Both programs qualify for single-family homes, multi-unit properties up to four units, and specific FHA or VA-approved condominiums. In West Michigan, these loans are perfect for the traditional housing stock found in Kalamazoo and Battle Creek. The property must serve as your primary residence and meet “Minimum Property Standards” to ensure it’s safe and sound. We recommend checking the approved condo list early in your search to avoid any mid-flight delays.

Do VA loans take longer to close than FHA loans in Kalamazoo?

No, VA loans don’t inherently take longer to close than FHA loans when you’re working with a local West Michigan navigator. While there’s a common misconception that government appraisals cause delays, most applications reach a safe landing in 30 days or less. Our team handles the communication with appraisers and underwriters directly, ensuring your paperwork stays on schedule and your closing date remains firm without any unexpected turbulence.

Can I get an FHA loan in Portage with a 550 credit score?

Technically, you can get an FHA loan with a 550 credit score if you provide a 10% down payment, though most lenders in Portage prefer a score of 580 or higher. At 580, you only need the standard 3.5% down payment to achieve lift. If your score is currently sitting at 550, we can help you identify the specific credit turbulence holding you back and create a plan to reach the necessary thresholds for approval.

Latest Blog Post

EARNEST MONEY VS. DOWN PAYMENT: WHAT KALAMAZOO BUYERS MUST KNOW

Did your agent ask for a Earnest Money Deposit?

Are you planning to make an offer on a home in Kalamazoo, Portage, or Texas Township this week?