Outside Of The Box Programs: Non-QM

Demystifying Non-QM Loans: Your Guide to Niche Financing Solutions

In the world of mortgages, “Qualified Mortgages” (QM) often get all the attention. These are the conventional loans you typically hear about, adhering to strict guidelines set by the Consumer Financial Protection Bureau (CFPB). But what happens when your financial situation or the property itself doesn’t fit neatly into those QM boxes? That’s where Non-QM loans come in.

Non-QM, or Non-Qualified Mortgage, loans are designed for borrowers and properties that don’t meet traditional lending criteria. They offer a much-needed alternative for a diverse range of scenarios, from self-employed individuals to investors and those dealing with unique property types. While they might seem “weird” or unconventional, they play a crucial role in providing access to financing that would otherwise be unavailable.

Let’s dive into some of the most common and intriguing types of Non-QM loans:

Let’s dive into some of the most common and intriguing types of Non-QM loans:

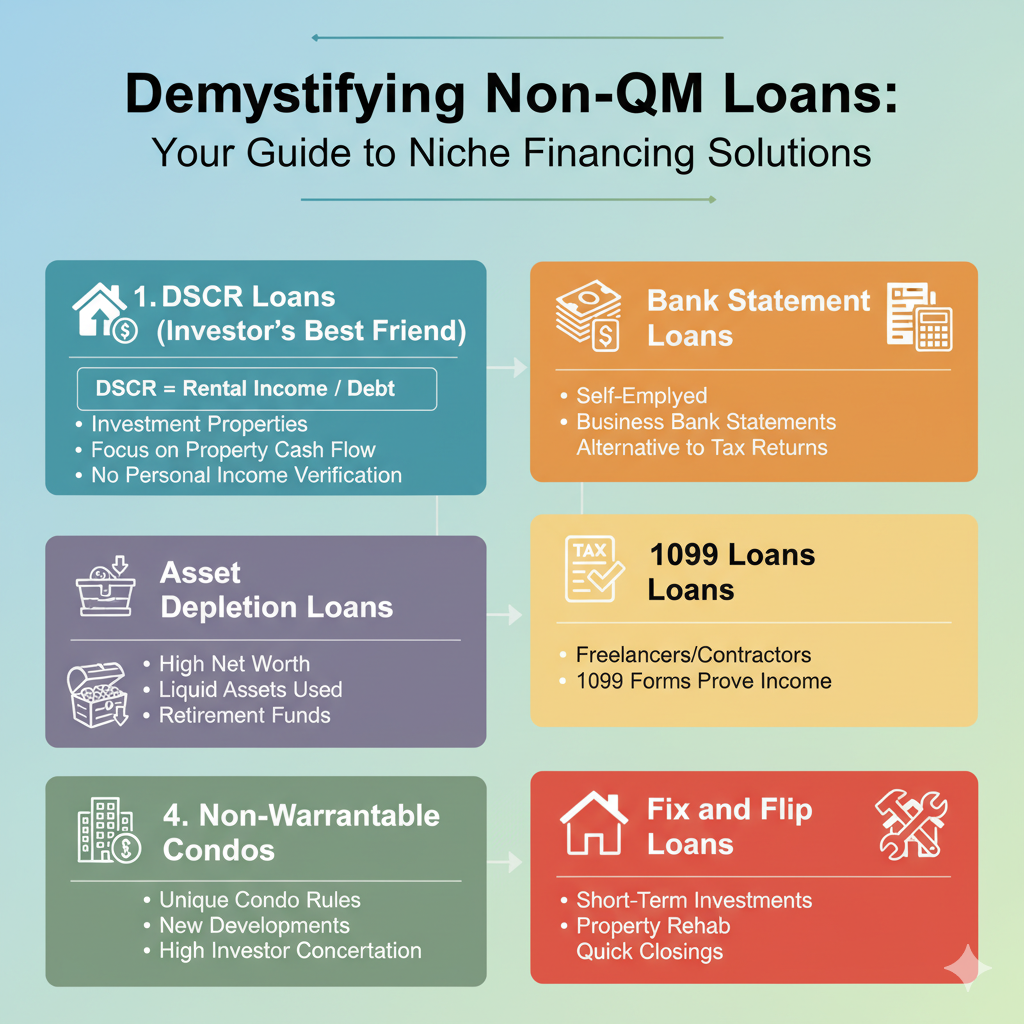

1. The Investor’s Best Friend: DSCR Loans

For real estate investors, the Debt Service Coverage Ratio (DSCR) loan is a game-changer. Instead of focusing on your personal income, lenders for DSCR loans primarily evaluate the income-generating potential of the investment property itself. The DSCR is calculated by dividing the property’s gross rental income by its monthly debt obligations (principal, interest, taxes, and insurance). If the rental income comfortably covers the debt, you’re likely a good candidate. This is fantastic for investors who might have multiple properties or a fluctuating personal income, as it streamlines the approval process significantly.

2. Tailored for the Self-Employed: Bank Statement Loans & 1099 Loans

Traditional programs often struggle with the irregular income streams of self-employed individuals, freelancers, and small business owners. Tax returns, while comprehensive, might not always reflect their true cash flow. This is where Bank Statement Loans and 1099 Loans shine:

- Bank Statement Loans: Instead of relying on W-2s or tax returns, we review your personal or business bank statements (typically 12 or 24 months) to determine your qualifying income. This is an excellent option for self-employed borrowers who write off many expenses, leading to a lower taxable income that wouldn’t qualify them for a QM loan.

- 1099 Loans: Specifically designed for independent contractors and gig economy workers who receive 1099 forms, these loans use the income reported on these forms to establish eligibility. It’s a straightforward way for these professionals to prove their earnings without the complexities of traditional income verification.

3. Leveraging Your Wealth: Asset Depletion Loans

For high-net-worth individuals with substantial liquid assets but perhaps a lower reported income, Asset Depletion Loans provide a viable path to homeownership. These loans allow borrowers to qualify based on their verifiable assets, such as retirement accounts, stocks, bonds, and other liquid investments, rather than traditional income. We essentially “deplete” a portion of these assets over a set period to calculate an imputed income, demonstrating the borrower’s ability to repay the loan.

4. Navigating Unique Property Challenges: Non-Warrantable Condos

Not all condos are created equal in the eyes of traditional lenders. Non-Warrantable Condos are properties that don’t meet Fannie Mae or Freddie Mac guidelines due to various factors, such as:

- A high percentage of investor-owned units

- A high concentration of commercial space within the building

- Ongoing litigation involving the homeowners’ association (HOA)

- Unique amenities or rules

While traditional financing might be off the table, Non-QM programs specialize in these properties, understanding their unique characteristics and offering solutions for buyers.

5. Fueling Real Estate Projects: Fix and Flip Loans

For real estate investors focused on acquiring, renovating, and quickly reselling properties, Fix and Flip Loans are essential. These short-term, interest-only loans are designed to provide rapid access to capital for both the purchase of the property and its renovation costs. They often come with quick closing times, which is crucial in a competitive real estate market where speed is paramount to securing deals.

The Benefits of Non-QM Loans

- Flexibility: They offer solutions for a wider range of financial situations and property types.

- Accessibility: They open up homeownership and investment opportunities for borrowers who wouldn’t qualify for conventional loans.

- Customization: Lenders often have more flexibility in underwriting, allowing for tailored solutions.

Things to Consider

While Non-QM loans offer incredible advantages, it’s important to be aware that they typically come with:

- Higher Interest Rates: Due to the increased risk for lenders.

- Higher Down Payments: Often required to mitigate risk.

- More Extensive Documentation (in some cases): While flexible on income, lenders still need to assess risk.

In conclusion, Non-QM loans are far from “weird” – they are innovative and vital tools in the modern mortgage landscape. They empower diverse borrowers to achieve their real estate goals, proving that there’s a financing solution for almost every unique scenario. If your situation doesn’t fit the conventional mold, exploring Non-QM options with a knowledgeable lender could be your key to unlocking the right financing. Give me a ring to discuss! (269) 360-7109

Latest Blog Post

EARNEST MONEY VS. DOWN PAYMENT: WHAT KALAMAZOO BUYERS MUST KNOW

Did your agent ask for a Earnest Money Deposit?

Are you planning to make an offer on a home in Kalamazoo, Portage, or Texas Township this week?

Visit Jeremy's Blog