FHA Loans in Michigan: Your 2026 Guide for Kalamazoo & Portage Homebuyers

Imagine standing on the edge of the 2026 Michigan housing market, watching prices climb while your savings account feels stuck on the tarmac. For many families in Kalamazoo and Portage, the dream of homeownership feels grounded by a credit score that isn’t perfect or the daunting 20% down payment myth. It’s true that the current market moves fast. The turbulence of rising costs can make anyone feel like they’re flying solo without a map. You deserve a co-pilot who understands the local terrain and the technical mechanics of a successful landing.

This guide shows you how fha loans michigan act like the extra lift provided by airplane flaps, helping you gain altitude with as little as a 3.5% down payment. We’ll break down the updated 2026 requirements, explain how to bypass credit turbulence, and outline your clear flight path to a new home in West Michigan. By the time we’re done, you’ll have the GPS coordinates needed to move from the waiting room to your new front door with total confidence.

Key Takeaways

- Understand how FHA loans provide the extra lift needed to overcome high-stress barriers and reach your homeownership goals with expert guidance.

- Learn the 2026 pre-flight requirements for fha loans michigan, including how a 3.5% down payment and specific credit scores determine your eligibility for takeoff.

- Pinpoint the exact 2026 loan limits for Kalamazoo and Calhoun Counties to ensure your financing strategy is perfectly aligned with local HUD regulations.

- Identify common appraisal “red flags” in older West Michigan homes that could stall your progress, from peeling paint to essential safety standards.

- Discover how partnering with a local co-pilot can integrate MSHDA assistance into your mortgage, providing a smooth landing for your new home.

What is an FHA Loan? The Extra Lift for Michigan Homebuyers

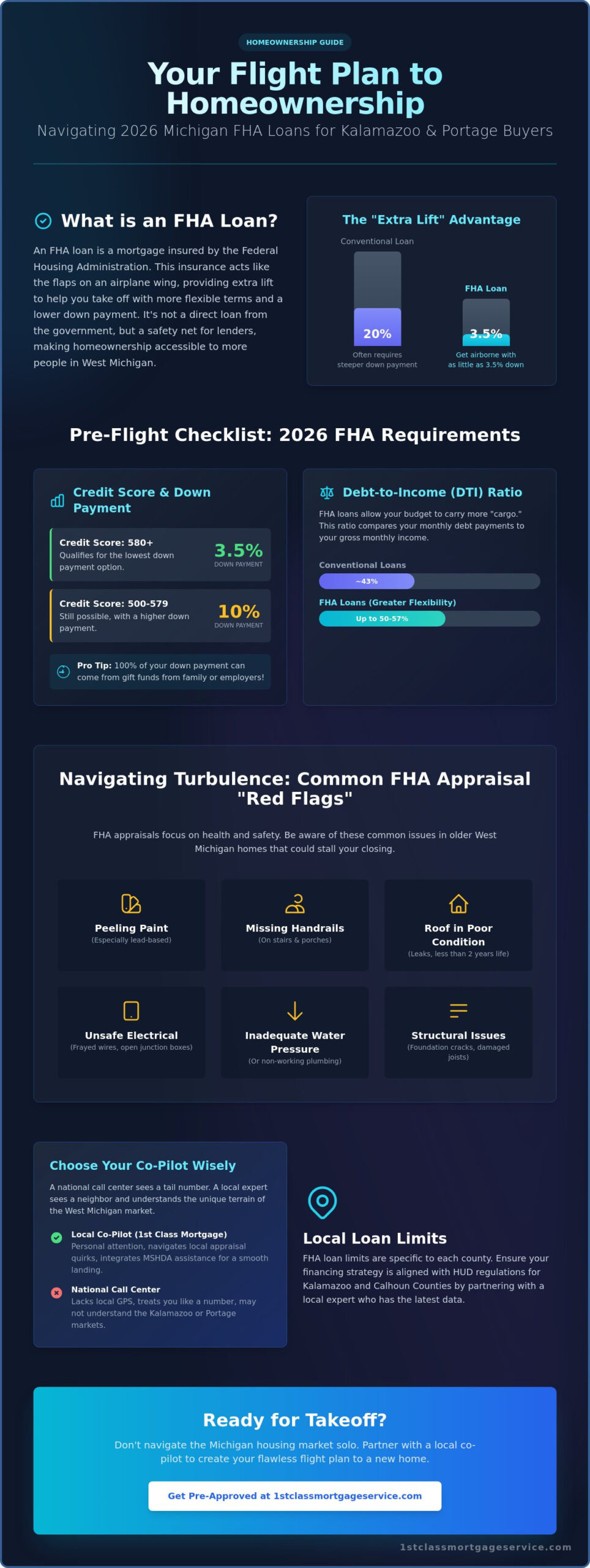

Taking flight toward homeownership in Southwest Michigan doesn’t require a massive inheritance or a perfect credit score. In the 2026 real estate market, an FHA insured loan serves as the essential aerodynamics for buyers who need a bit more lift. At its core, an FHA loan is a mortgage insured by the Federal Housing Administration. This isn’t a direct loan from the government. Instead, the FHA acts as a safety net, providing insurance to lenders like Treadstone Mortgage. This protection allows us to offer more flexible terms to neighbors in Kalamazoo and Portage who might not fit the rigid criteria of traditional banking financing.

Think of the FHA program as the flaps on an airplane wing. When you’re trying to get a heavy aircraft off the ground, you need that extra surface area to generate lift at lower speeds. For a homebuyer, that lift comes in the form of a low 3.5% down payment requirement. While some conventional programs demand a steeper ascent, FHA guidelines allow you to reach cruising altitude with significantly less cash upfront. In 2026, as West Michigan property values maintain their steady climb, this accessibility is the difference between staying grounded and finally taking flight with fha loans michigan.

How FHA Loans Work in the 2026 Michigan Market

The mechanics are straightforward; the government guarantee lowers the risk for the lender, which translates to more inclusive credit score requirements for you. For first-time buyers in Kalamazoo, this program creates a reliable runway. You will pay a Mortgage Insurance Premium (MIP), which funds the safety net that keeps the program viable for everyone. It’s a small price for the stability of a fixed-rate mortgage in a growing market like Portage. We see these loans as the primary engine for local neighborhood growth this year.

FHA vs. the “Big Banks”: The 1st Class Difference

Choosing your lender is like choosing your co-pilot. A national call center treats you like a tail number in a crowded sky. They lack the local GPS needed to navigate the specific appraisal quirks of older homes in the Vine neighborhood or the fast-moving listings in Portage. At Treadstone, we provide personal attention and respect. We don’t just process paperwork; we help you calibrate your financial instruments. Our team understands that fha loans michigan require a steady hand and local expertise to ensure a smooth landing at the closing table. Working with experienced fha lenders in Michigan who know the Kalamazoo and Portage markets can make the difference between a delayed departure and a seamless closing. We’re here every step of the way to ensure your flight plan is flawless.

2026 FHA Loan Requirements in Michigan: Clearing the Clouds

Before you taxi onto the runway, you need to know if your financial aircraft is cleared for takeoff. Meeting the FHA loan requirements in 2026 isn’t about having a perfect record; it’s about demonstrating stability and preparation. These loans remain a top choice for Kalamazoo families because they offer more lift with less initial capital. We see many buyers who assume they are grounded due to past credit turbulence, only to find that the FHA path is wide open for them.

Credit Scores and the 3.5% Down Payment Rule

The 2026 credit landscape for fha loans michigan is tiered to reward different levels of readiness. To qualify for the signature 3.5% down payment, you typically need a minimum credit score of 580. If your score lands between 500 and 579, you can still get airborne, but the down payment requirement increases to 10% to offset the risk. You don’t have to save every penny yourself. FHA guidelines allow for 100% of your down payment to come from gift funds provided by family members or employers. Think of this as extra fuel provided by your ground crew to help you reach the proper altitude sooner.

If you are currently below the 580 flight minimum, don’t panic. You can often boost your score by focusing on two specific areas. First, ensure no payments are more than 30 days late for at least 12 consecutive months. Second, keep your credit card balances below 30% of their limits. These small adjustments can provide the necessary lift to move your application from “denied” to “cleared for departure.” For a comprehensive breakdown of every credit, income, and property standard you’ll face, review the detailed 2026 loan requirements for FHA in Kalamazoo to ensure your application is fully prepared before takeoff.

Income Verification and DTI Ratios

Your Debt-to-Income (DTI) ratio measures how much cargo your monthly budget can carry without stalling the engine. FHA guidelines are famously more flexible than conventional products. While many programs want your total debt payments to stay under 43% of your gross monthly income, FHA can allow for ratios as high as 50% or even 57% in specific cases with strong compensating factors. This is a massive advantage for Portage residents balancing student loans or car payments alongside a new mortgage.

Stability is the name of the game for income. You generally need a two-year history of steady employment. It doesn’t mean you must be at the same job for 24 months, but your career path should show a logical progression. For self-employed buyers in the Kalamazoo area, we will look at your tax returns from 2024 and 2025 to calculate a reliable income average. We act as your co-pilot during this process, helping you organize your pay stubs and W-2s so the underwriter sees a clear, safe flight path. If you want to see how your specific numbers measure up, start your pre-flight check here with our local team.

The 2026 standards for fha loans michigan are designed to be inclusive. Whether you are a first-time buyer in Portage or looking to move closer to downtown Kalamazoo, these requirements provide a realistic runway for homeownership. We’re here to help you check your gauges and ensure you’re ready for a smooth landing in your new home.

Kalamazoo vs. Portage: Navigating Local FHA Loan Limits

Every successful flight requires a clear understanding of the ceiling. In the mortgage world, the Federal Housing Administration (FHA) sets specific altitude limits on how much you can borrow. These caps aren’t arbitrary; they’re calculated annually by HUD based on a percentage of the median home price for each county. For those looking into fha loans michigan, these limits provide the boundaries for your property search in West Michigan. If you’re eyeing a home in the 269 area code, knowing these numbers helps you determine if your dream home is within reach or if you need to adjust your flight path.

In the competitive West Michigan market, these limits act as your GPS. They ensure you don’t overextend while providing enough lift to compete with cash buyers or conventional offers. Because the median home price in Kalamazoo and Portage currently sits between $285,000 and $315,000, the local FHA limits offer a generous runway for most buyers. Understanding how current mortgage rates interact with these limits is equally important, as even a small rate shift can meaningfully change your monthly payment on a loan near the ceiling. Buyers searching in the outskirts of Kalamazoo or in smaller surrounding communities may also want to explore the USDA rural development loan as a zero-down alternative for eligible areas.

Understanding FHA Loan Limits in Kalamazoo County

For 2026, the FHA loan limit for a single-family home in Kalamazoo and Calhoun Counties is set at the national floor of $498,257. This cap is designed to cover the vast majority of local real estate without requiring a massive down payment. HUD calculates these figures by taking 115 percent of the local median home price, ensuring the program stays accessible for the average neighbor. If you’re interested in “house hacking,” the limits increase significantly for multi-unit properties:

- Duplex (2-unit): $637,950

- Triplex (3-unit): $771,125

- Four-plex (4-unit): $958,350

You can verify the exact current figures for any Michigan county by checking the official Kalamazoo and Portage FHA loan limits database. Having this data early in your journey prevents mid-flight corrections during the bidding process. For a deeper look at how local fha lenders in Michigan apply these limits alongside MSHDA stacking strategies, our dedicated guide breaks down every detail for Kalamazoo County buyers.

FHA vs. Conventional: Which Offers a Smoother Landing?

Choosing between fha loans michigan and a conventional mortgage often comes down to your current financial cargo. FHA loans are famous for their 3.5 percent down payment and flexible credit requirements. However, they do carry a lifetime mortgage insurance premium (MIP) if you put less than 10 percent down. Conventional loans might offer a lighter long-term cost if your credit score is high enough to ditch private mortgage insurance early.

For a detailed breakdown of how these options compare in our local market, check out our Conventional Mortgages in Kalamazoo comparison guide. While Portage properties often carry higher price tags that might tempt you toward conventional financing, the FHA program remains a steady, reliable co-pilot for buyers who want to keep more cash in their pockets for home improvements or emergency reserves. We’re here to help you weigh the upfront “lift” against the long-term interest costs to ensure you choose the most efficient route home.

The FHA Appraisal Process in West Michigan: Ensuring a Safe Flight

Think of the appraisal as your pre-flight safety check. Every pilot knows that a plane doesn’t leave the runway until the mechanics confirm it’s airworthy. When you utilize fha loans michigan, the appraisal serves a dual purpose. It verifies the home’s market value to protect your investment and ensures the property meets specific safety and habitability standards. This process prevents you from unknowingly purchasing a property with structural or safety defects that could ground your financial future.

In the Kalamazoo and Portage markets, we frequently see appraisals take about 8 to 12 days to complete. This timeline is a standard part of your flight plan. If the appraiser identifies issues, they will list them as “subject to” repairs. This means the loan can still move forward once the specific items are fixed and reinspected. It’s a common part of the journey, not a reason to cancel your trip.

What FHA Inspectors Look for in Battle Creek Homes

FHA inspectors focus on the three pillars of safety, security, and soundness. In older Battle Creek neighborhoods, we often encounter specific regional “red flags.” Peeling or chipping paint in homes built before 1978 is a major concern due to lead-based paint risks. Additionally, Michigan’s climate means inspectors look closely at basement dampness and roof integrity. A roof generally needs at least 24 months of remaining life to pass inspection. These standards act as a built-in safety net, ensuring your new home is a stable asset rather than a money pit.

How to Prepare for Your FHA Appraisal

Preparation is the key to a smooth takeoff. Sellers and buyers can work together to ensure the home is ready for the inspector’s walk-through. Simple fixes often prevent the most common delays. Check that all handrails on stairs are secure; ensure the HVAC system is fully operational; and verify that every level of the home has functioning smoke detectors. If repairs are required, they don’t have to end the deal. Buyers and sellers frequently negotiate who covers the costs of FHA-required fixes to keep the closing on schedule.

Our 1st Class approach involves identifying these potential hurdles before the appraiser even steps onto the porch. By addressing “red flags” early, we keep your mortgage moving toward a successful landing. We view ourselves as your seasoned co-pilots, providing the expert guidance needed to navigate these technical requirements with ease.

Don’t let appraisal questions keep you grounded. Reach out to Jeremy Drobeck today to start your FHA loan journey with a team that knows every inch of the West Michigan landscape.

Partnering with a Local Co-Pilot for Your Michigan FHA Loan

Choosing a mortgage shouldn’t feel like flying solo through a storm without a radar. When you’re looking for fha loans michigan, you need more than a digital portal; you need a seasoned co-pilot who knows the local terrain from the ground up. Jeremy Drobeck and the team at Treadstone Mortgage prioritize straight talk and radical transparency. We don’t hide behind industry jargon or fine print. Instead, we provide the clear visibility you need to make a confident decision for your family’s future.

One of the most powerful tools in our flight bag is the ability to integrate MSHDA down payment assistance with your FHA loan. Think of MSHDA as the extra lift provided by airplane flaps during a steep climb. It provides the necessary boost to get you off the runway when your savings might be a bit light. We handle the complex coordination between state programs and federal guidelines, ensuring your “flight” toward homeownership stays on course and under budget. We’re here every step of the way, from the initial pre-approval to the moment you receive the keys at the closing table.

Why a Local Kalamazoo Lender Makes the Difference

Our roots run deep in West Michigan, stretching from the sunset views in St. Joseph to the industrial heart of Battle Creek. This local expertise isn’t just about geography; it’s about understanding the specific appraisal standards and market cooling trends in Kalamazoo and Portage. Our “1st Class” commitment means you get neighborly reassurance backed by technical precision. For a broader look at the local market landscape, check out our Navigating Your Purchase Mortgage in Kalamazoo guide to sharpen your overall strategy.

Ready for Takeoff? Your Next Steps to Homeownership

Starting your journey with fha loans michigan is simpler than you might think. We’ve streamlined the process into three clear stages to ensure you’re airborne as quickly as possible:

- The Pre-Flight Check: Complete a secure online application to determine your buying power.

- Gather Your Cargo: Have your 2024 and 2025 W2s, recent paystubs, and bank statements ready for our flight crew to review.

- The Consultation: Meet with Jeremy Drobeck to review your options and lock in your flight plan.

Don’t let the complexity of the mortgage market keep you grounded. Whether you’re a first-time buyer in Portage or looking to upgrade in Kalamazoo, we have the tools and the local experience to guide you home safely. If you’re purchasing in a qualifying suburban or rural area, the USDA rural development loan program may offer 100% financing with lower mortgage insurance costs than FHA — another powerful option worth discussing during your consultation. Contact Jeremy Drobeck today for a personalized mortgage consultation and let’s get your homeownership dreams cleared for takeoff.

Clear the Runway for Your New Michigan Home

Navigating the 2026 housing market doesn’t have to feel like flying through a storm. Whether you’re eyeing a quiet street in Portage or a historic neighborhood in Kalamazoo, fha loans michigan offer the steady lift needed to get your dreams off the ground. Our team brings over 20 years of local experience to your side of the cockpit, helping you master 2026 loan requirements and MSHDA Down Payment Assistance programs. We treat every appraisal and limit check as a vital part of your pre-flight inspection. As a division of Neighborhood Loans, Inc. (NMLS #222982), we provide the technical precision and personal respect you deserve during this major life milestone. You’ve studied the requirements and mapped out the local limits between Kalamazoo and Portage. Now it’s time to stop watching from the terminal and start your own ascent into homeownership. We’re here to handle the heavy lifting so you can enjoy the view from your new front porch.

Start your flight plan with a 1st Class mortgage consultation today!

Frequently Asked Questions

What is the minimum credit score for an FHA loan in Michigan in 2026?

The Federal Housing Administration requires a minimum credit score of 580 to qualify for the 3.5% down payment program in 2026. If your score sits between 500 and 579, you can still gain lift, but HUD guidelines require a 10% down payment. Think of your credit score as the flight plan for your mortgage; a higher score creates a smoother takeoff with better interest rates. We’re here every step of the way to help you navigate these credit requirements.

Can I use MSHDA down payment assistance with an FHA loan?

You can absolutely pair MSHDA down payment assistance with fha loans michigan to lower your initial costs. MSHDA currently offers up to $10,000 in assistance for eligible homebuyers in Kalamazoo and Portage. This program acts like extra lift from airplane flaps, providing the boost needed to reach the runway of homeownership. We’ll check your eligibility for these state-backed funds during your initial mortgage consultation to ensure you maximize your options.

How much is the FHA down payment for a home in Kalamazoo?

The standard FHA down payment for a home in Kalamazoo is 3.5% of the purchase price. For a $300,000 home, you would need a minimum of $10,500 for your down payment. This low entry requirement serves as a shorter runway for buyers who want to get airborne without waiting years to save. We provide a clear GPS for your closing costs so you know exactly what fuel you need for the journey.

Are FHA loans only for first-time homebuyers in Michigan?

FHA loans are available to any qualified buyer who plans to use the property as their primary residence, not just first-time buyers. While many new pilots in the housing market use this program, repeat buyers often utilize it to preserve cash for other investments. As long as you don’t have another FHA loan currently active, you can use this 1st Class financing option. It’s a reliable instrument for anyone looking for flexible credit and low down payments.

What are the FHA loan limits for Kalamazoo County in 2026?

For 2026, the FHA loan limit for a single-family home in Kalamazoo County starts at a floor of $498,257, based on recent HUD adjustments. These limits are updated annually to reflect the rising median home prices in West Michigan. This ceiling ensures you have enough room to purchase a quality home in Portage or Mattawan. We’ll verify the exact coordinates for your specific property type to ensure your loan stays within the approved flight path.

Does the FHA loan cover the cost of home renovations?

The FHA 203(k) program is designed specifically to cover both the purchase price and the cost of home renovations. This specialized financing allows you to roll repair costs into one monthly payment, rather than taking out a separate high-interest loan. It’s the perfect tool for engineering a home that fits your vision. For a complete breakdown of how to combine your purchase price and repair costs into one manageable payment, explore our renovation mortgage guide for Kalamazoo and Portage homebuyers. Our team manages the technical details of the renovation escrow so your project stays on schedule and your budget remains balanced.

How long does the fha loans michigan approval process take in West Michigan?

The fha loans michigan approval process typically takes 30 to 45 days from the time you submit your application to the final closing. Our team at Treadstone Mortgage performs a rigorous pre-flight check on your documents to accelerate this timeline. By staying proactive and transparent, we avoid the turbulence that often delays big bank approvals. We maintain a steady rhythm to ensure you land in your new home exactly when you planned.

Can I buy a fixer-upper with an FHA loan in Battle Creek?

You can buy a fixer-upper in Battle Creek using an FHA 203(k) loan, which is tailored for properties needing repairs. A standard FHA loan requires the home to be in move-in condition, but the 203(k) option allows for structural or cosmetic upgrades. If you’re considering this route, our renovation mortgage financing guide for Kalamazoo and Portage walks through exactly how to navigate contractor bids and inspection requirements for a successful project. We’ll help you navigate the contractor bids and inspection requirements to ensure a successful renovation journey.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”