2026 Loan Requirements for FHA: Your Kalamazoo Homeownership Flight Plan

What if a 600 credit score isn’t a “no-fly” zone, but simply a slightly shorter runway for your homeownership dreams? Most West Michigan buyers feel a surge of turbulence when they look at their credit report or worry about the 2026 loan requirements for fha. It’s stressful to think a few past mistakes or a confusing new loan limit could keep your family grounded while prices in Kalamazoo and Portage continue to climb. We understand that a mortgage isn’t just a transaction; it’s the engine for your family’s future.

You deserve a clear flight path, so we’ve detailed the specific credit, income, and property standards that will help you secure approval without the typical banking stress. We’ll examine the updated debt-to-income ratios, the latest 2026 Kalamazoo County limits, and the “flaps” you can deploy through local assistance programs to get your application airborne. This checklist provides the expert GPS you need to move from pre-approval to the closing table with total confidence. We’re here to help you handle the heavy lifting so you can focus on where to put your furniture.

Key Takeaways

- Identify why the FHA program serves as the ideal runway for first-time buyers in Kalamazoo and Battle Creek seeking an accessible path to homeownership.

- Master the 2026 loan requirements for fha, including the specific credit score “magic numbers” and debt-to-income ratios required to clear for takeoff.

- Learn how to pass the property hangar check by understanding the safety, soundness, and security standards required for every West Michigan home.

- Discover how MSHDA assistance acts as “flaps” to provide extra lift, helping you secure up to $10,000 for your down payment in 2026.

- Ensure a smooth final approach by learning why a local pre-flight briefing with a Kalamazoo expert provides more stability than a national big-box lender.

The 2026 FHA Pre-Flight Checklist: Basic Eligibility in Kalamazoo

Taking the leap into homeownership feels a lot like a first solo flight. You need the right equipment, a clear sky, and a reliable flight plan. In West Michigan, the FHA insured loan serves as the primary runway for thousands of residents in Kalamazoo, Portage, and Battle Creek. Backed by the Department of Housing and Urban Development (HUD), these mortgages provide the extra lift needed for those who might not fit the rigid criteria of a traditional conventional loan.

The 2026 loan requirements for fha are designed for accessibility. Instead of requiring a massive 20% down payment, this program allows you to clear the trees with as little as 3.5% down. It’s the standard choice for first-time buyers because it offers more “flaps” or flexibility regarding credit scores and debt ratios. Think of Jeremy Drobeck as your Seasoned Co-Pilot. With years of experience navigating the West Michigan market, Jeremy ensures your paperwork is airworthy before you ever hit the tarmac. He provides the personal attention needed to turn a complex government program into a smooth ascent toward your new front door.

Who Qualifies for an FHA Loan in West Michigan?

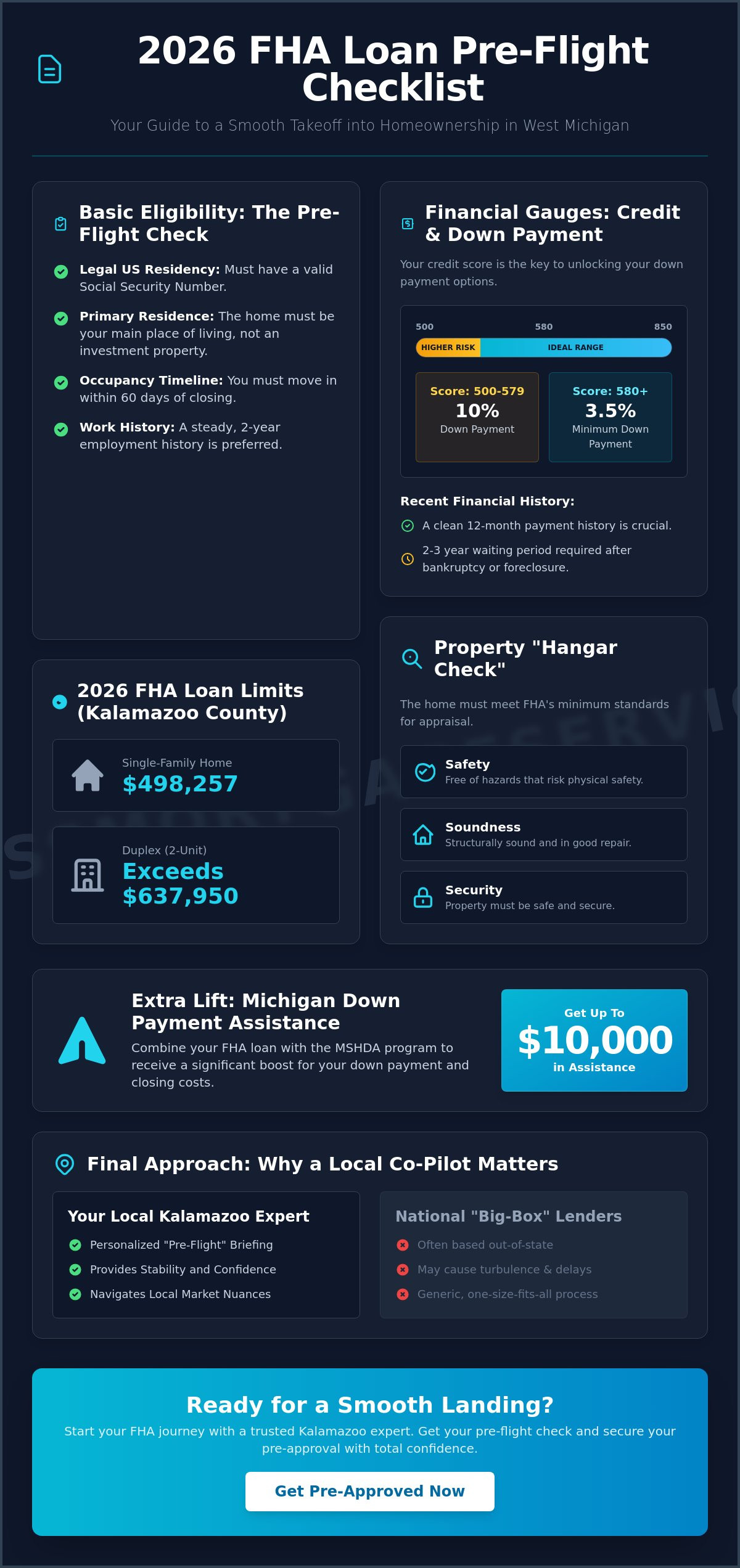

Eligibility starts with your status. You must be a legal resident of the United States with a valid Social Security number to apply. Your intended property must be your primary residence. This program isn’t for investors looking to flip a house in the Vine Neighborhood or build a rental empire in Battle Creek. You’re required to move into the home within 60 days of closing to satisfy the residency rules.

Employment stability is another critical component of the loan requirements for fha. Lenders typically look for a two-year steady work history. If you’ve spent the last 24 months working for local employers like Stryker, Pfizer, or Western Michigan University, you’re in a strong position. Gaps in employment don’t always ground your flight; however, they do require a clear explanation for the underwriters. Jeremy helps you document these transitions so the lender sees a trajectory of stability rather than turbulence.

2026 FHA Loan Limits for Kalamazoo and Portage

Every year, HUD adjusts the “floor” and “ceiling” for how much you can borrow based on regional home values. For 2026, the single-family home limit in Kalamazoo County has been updated to reflect the local market growth. In Kalamazoo and Portage, the current floor for a one-unit property is $498,257. This allows buyers to remain competitive even as prices in popular neighborhoods continue to climb.

If you’re looking at multi-unit properties in Battle Creek, the limits increase significantly to accommodate the higher purchase prices of 2-4 unit buildings. A duplex (2-unit) allows for a higher ceiling, often exceeding $637,950, which is a fantastic strategy for those looking to live in one unit and rent the other. For a deeper look at how these numbers impact your specific neighborhood, check out this FHA loans in Michigan guide. It provides the GPS coordinates you need for a successful landing in the 2026 market.

Financial Gauges: Credit Scores and Debt-to-Income Ratios

Before you hit the runway in Kalamazoo, you must check your financial gauges. The most critical indicators for loan requirements for fha are your credit score and your debt-to-income (DTI) ratio. Think of these as your fuel levels and weight distribution. For a standard 3.5% down payment, 580 is the “Magic Number” you want to see on the dashboard. If your score sits between 500 and 579, you can still get airborne, but federal guidelines require a 10% down payment to offset the increased risk. Understanding FHA loan basics helps you see why these standards exist to keep the housing market stable for everyone.

Credit Requirements and Recent Turbulence

Credit history is about more than just a three-digit number; it’s about your recent trajectory. If you’ve navigated a bankruptcy or foreclosure, you typically need a two to three-year waiting period before your 2026 eligibility resets. West Michigan lenders look for a clean 12-month payment history to prove you have regained control of your financial aircraft. A credit overlay is a lender’s additional safety margin that requires higher standards than the minimum HUD rules. While the government sets the floor, individual banks often set their own ceilings to ensure a safe landing for their portfolio.

Calculating Your DTI for a Smooth Ascent

Your DTI ratio measures how much of your gross monthly income goes toward debt. FHA typically looks for a 31% front-end ratio for housing costs and a 43% back-end ratio for total debt. However, if you have high credit scores or significant cash reserves, lenders might allow for higher ratios. High car payments or student loans can quickly trim your borrowing power. To see how your specific debts affect your monthly “lift” in the Kalamazoo market, use this FHA loan calculator to test different price points and interest rates.

Calculating qualifying income isn’t always a straight flight path, especially with overtime or self-employment. Your loan officer acts as your GPS, navigating the complex loan requirements for fha to ensure your income is documented with precision. We’re here to help you interpret these gauges so you don’t face unexpected headwind during underwriting. Choosing from the best FHA lenders Michigan has available can make a significant difference in how smoothly your income documentation is handled. If you are ready to review your financial dashboard, connect with a local mortgage expert for a personalized flight plan today.

The Property Hangar Check: FHA Appraisal Standards

Before we clear you for takeoff, your future home needs a thorough pre-flight inspection. An FHA appraisal is much more than a simple valuation to justify the purchase price; it’s a rigorous safety audit. Think of this as the “Property Hangar Check” where an appraiser ensures the home meets the Three S’s: Safety, Soundness, and Security. These loan requirements for fha are designed to protect you from moving into a “plane” that isn’t airworthy.

In Kalamazoo, our landscape is dotted with beautiful historic properties. While these homes have character, they often trigger “grounding” issues during an inspection. For example, any home built before 1978 is scrutinized for peeling or chipping paint due to lead-based paint hazards. Other common red flags include missing handrails on staircases, exposed wiring, or a roof that doesn’t have at least two years of remaining life. If these issues appear, the appraiser will mark the report “Subject-To,” meaning repairs must be completed before you can head to the closing table.

While you navigate these property standards, remember that financial tools like Michigan Down Payment Assistance can provide the extra lift needed to manage your upfront costs, allowing you to keep more cash in reserve for any necessary home maintenance after you move in.

FHA vs. Conventional Property Requirements

The standards for FHA loans are notably stricter than those for Conventional Mortgages. While a conventional appraiser might note a cracked window as a cosmetic flaw, an FHA appraiser sees it as a safety hazard. If a property requires significant work that the seller won’t fix, don’t worry. We can often pivot your flight plan to an FHA 203(k) Renovation Loan, which allows you to bundle repair costs directly into your mortgage.

Specific Issues for West Michigan Homes

Properties in rural Kalamazoo County or near the lakeshore face unique scrutiny. If you’re looking at a home with a private well and septic system, FHA guidelines require specific separation distances to ensure water safety. In our Michigan climate, the heating system is also a major focus. The appraiser must verify that the system is permanent and capable of maintaining a temperature of at least 50 degrees in all living areas to prevent pipe bursts during a deep freeze. Basements must also show no signs of active moisture or structural instability that could be worsened by our heavy snowmelt cycles.

Your journey to homeownership should be a controlled, engineered process. By understanding these loan requirements for fha properties early, we can identify potential turbulence before it affects your closing date. I’m here to act as your seasoned co-pilot, ensuring every detail of your “hangar check” is handled with precision.

Extra Lift: Combining FHA with Michigan Down Payment Assistance

Every pilot knows that lift is the key to a successful takeoff. If your savings account isn’t quite ready for the 3.5% down payment, the Michigan State Housing Development Authority (MSHDA) acts as your aircraft’s flaps. These programs provide the extra boost needed to get you off the ground. In 2026, the MSHDA MI 10K DPA program continues to be a primary tool for local buyers. It offers up to $10,000 in assistance. This can effectively cover the minimum cash investment needed to meet the loan requirements for fha in Kalamazoo. By combining these tools with other Michigan first time home buyer programs, you can significantly reduce your out-of-pocket costs.

Step-by-Step: Getting Approved for MSHDA + FHA

Securing this extra lift requires a specific pre-flight checklist. MSHDA isn’t a “one size fits all” program; it’s designed for those who meet specific household income and purchase price limits. In Kalamazoo County, these limits are updated annually to reflect local economic conditions. Following these steps ensures your application stays on course:

- Check Income Eligibility: Your total household income must fall below the Kalamazoo County median, which currently sits at specific thresholds for families of two or fewer, and higher for families of three or more.

- Complete Education: You’ll need to finish a state-approved homebuyer education course. These are available through local providers in Portage or can be completed via an online portal.

- Partner with an Expert: You must work with a MSHDA-approved lender who understands how to layer these funds with FHA guidelines. Jeremy Drobeck and his team provide the personal attention needed to manage this dual-approval process.

Gift Funds and Seller Concessions

The loan requirements for fha are remarkably flexible when it comes to where your money comes from. If you don’t have the full 3.5% saved, FHA allows 100% of your down payment to come from a family gift. This “gift fund” must be documented with a clear paper trail, showing the transfer from your relative’s account to yours. It’s a common way for first-time buyers to reach the runway faster.

Beyond the down payment, you also have to consider closing costs. This is where Kalamazoo sellers can help. FHA guidelines allow for a seller concession of up to 6% of the purchase price. In a balanced market, it’s common for sellers to pay for your appraisal, title insurance, and credit report fees to help close the deal. Seller concessions act as a tailwind, effectively covering your transaction costs so your personal savings stay in your pocket for future home repairs.

By negotiating for the seller to pay your closing costs, you drastically lower the total cash to close required at the final runway.

Ready to see how much lift you can get for your Kalamazoo home purchase? Apply now for a custom flight plan and see if you qualify for MSHDA assistance.

Final Approach: Starting Your FHA Journey with Jeremy Drobeck

Every successful flight begins on the ground with a rigorous pre-flight briefing. In the mortgage world, that is your pre-approval. While some buyers wait until they find a house to talk to a lender, the 2026 Kalamazoo market moves too fast for that strategy. You need to know exactly how the loan requirements for fha apply to your specific financial situation before you start touring homes in Winchell or Milwood. A pre-approval gives you the clearance to make a confident offer the moment you find the right property.

Big-box national banks often treat you like a flight number. You are a data point in a call center located three time zones away. Treadstone Mortgage operates differently. We focus on personal attention and 1st Class service because we live and work in the same neighborhoods you are looking to buy in. Local expertise means we understand Kalamazoo property taxes, local appraisal quirks, and the specific 2026 market conditions that national lenders often miss. Working with experienced FHA lenders in Michigan who know the Kalamazoo and Portage markets ensures your file receives the local insight and precision it deserves. We are here to ensure your file is handled with precision and respect.

Your West Michigan Mortgage Co-Pilot

Jeremy Drobeck brings over 20 years of experience to your cockpit. He has guided thousands of families through the Kalamazoo mortgage process, ensuring they reach their destination safely. Our “No-Turbulence” guarantee means you’ll get clear, proactive communication from the moment you apply until you are handed the keys at the closing table. We don’t hide behind fine print or leave you guessing about your status. We provide the steady hand you need to navigate any unexpected crosswinds during the underwriting process. Schedule your 1st Class Mortgage Consultation today to get started.

Preparing Your “Flight Bag” (Documentation)

To clear the 2026 loan requirements for fha, you’ll need your documentation organized and ready for inspection. Think of this as your flight bag; it contains everything necessary for a smooth ascent. Having these items ready for your 2026 review will prevent delays in your timeline. Please gather the following essentials:

- W2 forms from 2024 and 2025

- Your most recent pay stubs covering a 30-day period

- Complete bank statements for the last 60 days (all pages)

- Signed federal tax returns for the past two years

Before we throttle up, we will perform a final “GPS” check. This involves looking at the current mortgage rates and comparing different programs to ensure you’re on the most efficient path. Your Kalamazoo home isn’t just a dream; it’s a destination that’s well within reach when you have the right flight plan and a seasoned co-pilot by your side.

Clear the Runway for Your Kalamazoo Homeownership Journey

You’ve checked the financial gauges and inspected the property hangar. Now it’s time to put that knowledge into action. Understanding the loan requirements for fha in 2026 is your primary flight plan for securing a home in West Michigan. We’ve covered how specific credit benchmarks and debt-to-income ratios dictate your trajectory. You also know how MSHDA programs provide the extra lift needed for a successful takeoff. These aren’t just technical hurdles; they’re the coordinates for your new front door.

Jeremy Drobeck brings over 20 years of local lending expertise to your flight deck. As a division of Neighborhood Loans (NMLS #222982), the team specializes in integrating MSHDA assistance with FHA products to ensure a smooth landing. You don’t have to navigate these complex airspaces alone. With a seasoned co-pilot, the process becomes a controlled and predictable journey toward your goals. We’re here to monitor the radar while you focus on the destination.

Ready for takeoff? Get your FHA Pre-Approval from Kalamazoo’s 1st Class Mortgage Service today!

Your dream home is on the horizon. Let’s get you airborne and headed home.

Frequently Asked Questions

What is the minimum credit score for an FHA loan in Michigan in 2026?

The minimum credit score required for an FHA loan with a 3.5 percent down payment is 580. If your score falls between 500 and 579, you can still achieve lift-off by providing a 10 percent down payment. We help you calibrate your financial GPS to ensure your score meets these federal standards before we hit the runway in Kalamazoo. Our team provides the personal attention needed to navigate these credit benchmarks safely.

Can I use an FHA loan to buy a duplex in Kalamazoo?

You can purchase a duplex in Kalamazoo using an FHA loan as long as you occupy one of the units as your primary residence. This multi-engine strategy allows you to use 75 percent of the projected rental income from the second unit to help you qualify for the mortgage. It is a smart way to offset your monthly costs while building equity in local neighborhoods like Vine or Westnedge Hill.

How much is the FHA down payment requirement in Portage?

The standard down payment for an FHA loan in Portage is 3.5 percent of the home’s purchase price. For a property priced at $275,000, your required fuel for the transaction would be $9,625. We often look for extra lift through MSHDA programs or local grants that can cover these costs, ensuring your flight to homeownership doesn’t stall due to upfront cash requirements. We are here every step of the way to find these options.

Does the FHA require mortgage insurance for the life of the loan?

FHA mortgage insurance stays for the entire loan term if your initial down payment is less than 10 percent. If you provide a down payment of 10 percent or more, the annual Mortgage Insurance Premium (MIP) is removed after 11 years. This safety gear protects the lender, but we can plan a mid-flight refinance into a conventional loan once your home equity reaches the 20 percent mark to eliminate this cost early.

What is the maximum debt-to-income ratio for FHA approval?

The maximum debt-to-income ratio for FHA approval is generally 43 percent, though some borrowers reach a 56.9 percent ceiling with automated underwriting and compensating factors. We analyze your monthly obligations against your gross income to ensure your cargo weight doesn’t exceed safety limits. Understanding these loan requirements for fha helps us clear you for a smooth departure without financial turbulence. We focus on precision to ensure your file is flight-ready.

Are FHA loan limits higher in Kalamazoo than in other Michigan counties?

Kalamazoo County loan limits are lower than high-cost areas like Washtenaw County but remain competitive with the broader West Michigan market. In 2024, the floor for a single-family home was set at $498,257, and 2026 projections suggest a steady climb based on local appreciation. We monitor these altitude limits closely to ensure your target home in Portage or Texas Township fits within the established FHA flight path for our region.

Can I get an FHA loan if I have a recent bankruptcy?

You can qualify for an FHA loan 2 years after a Chapter 7 bankruptcy discharge or 1 year into a Chapter 13 payout with court approval. This waiting period acts as a necessary maintenance check to prove your financial systems are back in working order. We have helped many families in Southwest Michigan get back in the air after a financial setback by documenting a clean 12-month payment history and stable employment.

How do FHA appraisal requirements differ from a standard home inspection?

An FHA appraisal focuses on the property’s market value and specific safety standards, while a home inspection provides a deep dive into the home’s mechanical health. The appraiser checks for safety hazards like peeling lead paint or missing handrails to meet the loan requirements for fha. Think of the appraisal as a flight-readiness check for the bank and the inspection as your personal mechanic’s detailed report on the aircraft’s engine and structure.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”