FHA Loan Calculator for Kalamazoo, Michigan: Estimate Your 2026 Mortgage Payments

What if the biggest barrier to your 2026 home purchase isn’t your down payment, but the mystery of the monthly math? Many buyers in West Michigan feel like they’re flying through heavy fog when they try to estimate the true cost of a mortgage. You likely agree that buying a home in Kalamazoo or Portage should be a rewarding milestone, yet the anxiety over property taxes and Mortgage Insurance Premiums (MIP) often creates unnecessary turbulence. It’s frustrating to feel like you’re guessing at your financial future. My goal is to act as your seasoned co-pilot, helping you clear the runway for a successful move.

By using a specialized fha loan calculator, you can master the specific numbers required for our local market. This article provides a clear monthly payment estimate and a roadmap to homeownership that removes the guesswork. We’ll break down the hidden costs that often surprise buyers in Battle Creek and show you how to gain total confidence in your budget. You’ll learn exactly how to calculate your 2026 payments so you can prepare for takeoff with peace of mind.

Key Takeaways

- Understand how FHA loans provide the “extra lift” needed for West Michigan buyers navigating lower credit scores or smaller down payments.

- Use an fha loan calculator to map out your 2026 monthly payments and calculate the 3.5% down payment required to clear the runway.

- Navigate local airspace by identifying the specific 2026 FHA loan limits for Kalamazoo and Van Buren Counties before you start your home search.

- Compare FHA and Conventional flight paths to determine which mortgage option offers the most efficient “wind speed” for your unique credit profile.

- Discover how MSHDA programs act as “extra flaps” for first-time buyers, providing the additional support needed for a smooth landing in a new home.

Understanding the FHA Loan: Your Pre-Flight Checklist for Kalamazoo Real Estate

Think of the FHA loan as the extra lift provided by airplane flaps on a short runway. It’s a government-backed mortgage designed to help Michigan families get airborne when they might lack a massive down payment or a perfect credit score. Since its inception in 1934, the FHA insured loan has served as a critical tool to lower the barriers to entry for homeownership. By providing a safety net for lenders, it allows us to offer more flexible terms to buyers who are ready for the responsibility of a mortgage but need a slightly smoother path to takeoff.

While the Federal Housing Administration provides the insurance, they don’t actually hand you the keys or the cash. You still need a seasoned co-pilot to manage the technical aspects of your financing. Working with a local expert like Jeremy Drobeck at Treadstone Mortgage ensures your loan is structured correctly for the West Michigan market. We specialize in taking the stress out of the paperwork, providing personal attention that you simply won’t find at a massive, impersonal national bank. Our goal is to ensure your flight path toward a 2026 home purchase is stable, transparent, and successful.

Why Use an FHA Loan Calculator Before You Shop?

Before you head out to tour open houses in Winchell or Milwood, you need a reliable GPS. An fha loan calculator acts as your primary navigation tool, helping you avoid financial turbulence before you ever sign a purchase agreement. It’s about seeing the full horizon. A mortgage isn’t just a single number; it’s a combination of principal, interest, taxes, and insurance, often referred to as PITI.

Local tax rates in Kalamazoo and Portage can significantly change the altitude of your monthly payment. For instance, summer and winter tax bills in the City of Kalamazoo differ from those in Texas Township. Using a calculator allows you to plug in these specific variables so you aren’t surprised by “hidden” costs that could stall your momentum. It’s better to adjust your coordinates now than to realize mid-flight that your budget is stretched too thin.

The 2026 FHA Outlook for West Michigan

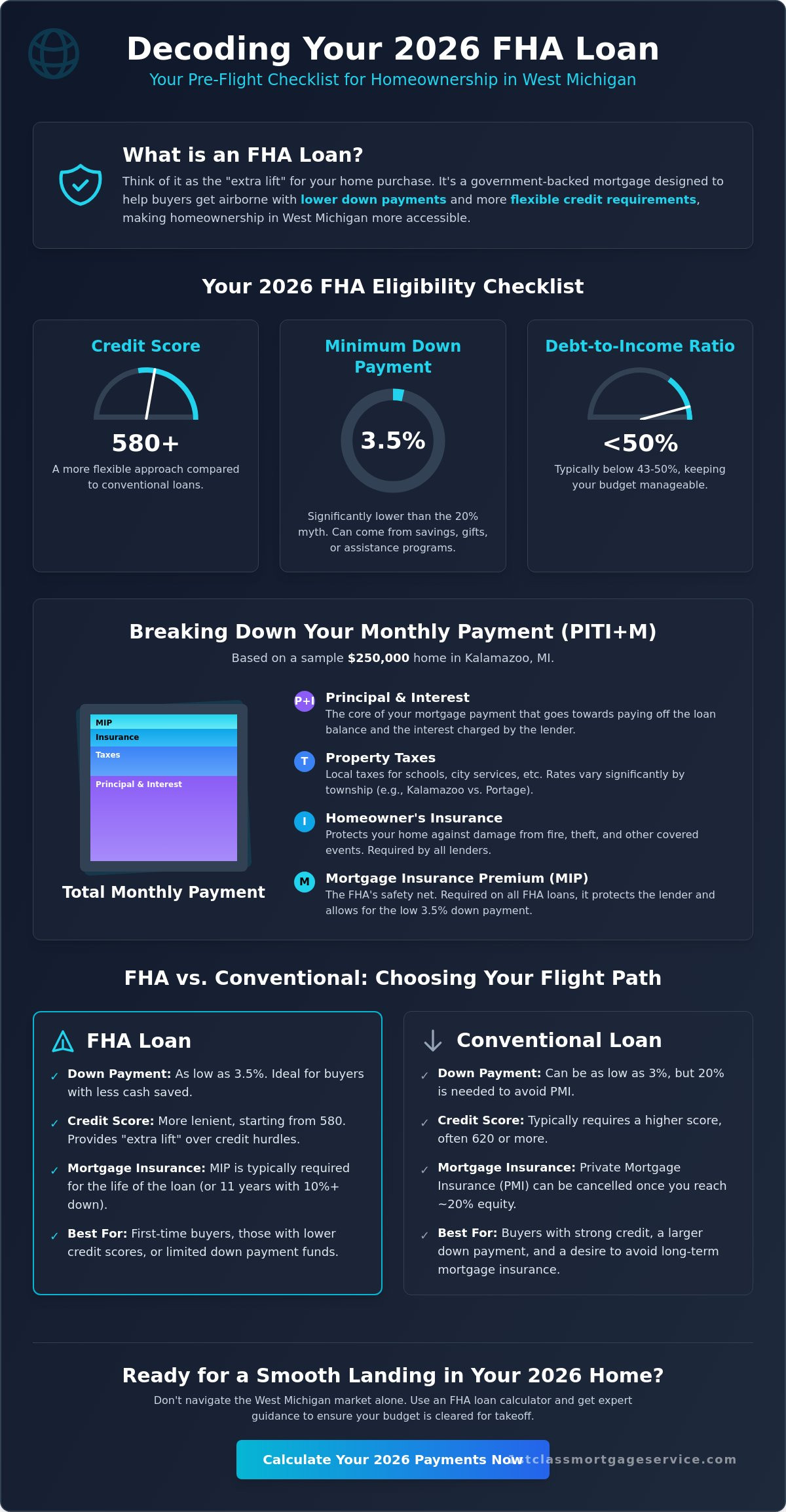

The Kalamazoo real estate market remains a beacon of stability for 2026, making it an ideal environment for FHA buyers. These loans remain a top choice because they allow for down payments as low as 3.5%. FHA loan eligibility in 2026 is a specific combination of maintaining a credit score of at least 580 and keeping your debt-to-income ratio within manageable limits, typically below 43% to 50% depending on your overall profile. Even if your situation feels “outside of the box,” we have the experience to help you find a solution. We’ve seen every type of headwind, and we’re here to help you navigate through it. For a comprehensive overview of how FHA loans in Michigan work for Kalamazoo and Portage homebuyers, our 2026 guide breaks down every requirement in detail.

Breaking Down the FHA Math: How to Calculate Your “Extra Lift”

Calculating your monthly obligation isn’t just about the sticker price on a Zillow listing in Winchell or Milwood. It requires a precise pre-flight check of four specific components. When you use an fha loan calculator, you’re essentially mapping out your flight path before you ever leave the gate. We start by identifying your purchase price based on current Kalamazoo market data. As of late 2024, median home prices in the area hovered around $245,000, providing a solid baseline for your estimates. From there, we calculate your 3.5% down payment, account for mortgage insurance, and factor in the local tax climate of West Michigan.

The Down Payment: Minimal Runway Required

Many first-time buyers in Michigan believe they need a 20% down payment to get airborne. That’s a myth that keeps too many pilots grounded. For an FHA loan, you only need 3.5% of the purchase price. On a $250,000 home, that’s $8,750. Think of this as the “extra lift” provided by airplane flaps; it helps you take off with less speed and cash than a conventional flight would require. You can source these funds from personal savings, documented gift funds from family, or even local down payment assistance programs. If you’re unsure where your fuel will come from, you can explore all options with a local expert who understands the Kalamazoo landscape.

Mortgage Insurance (MIP): The Safety Net for Your Flight

Because FHA loans allow for lower down payments and flexible credit scores, the U.S. Department of Housing and Urban Development (HUD) requires mortgage insurance to protect the integrity of the program. This comes in two parts. The Upfront Mortgage Insurance Premium (UFMIP) is 1.75% of the loan amount. Most Kalamazoo buyers roll this into their total loan balance rather than paying it at closing. The second part is the annual MIP, which is divided into 12 monthly installments. This monthly cost acts as your safety net, ensuring the government guarantee remains in place for the life of the loan.

- LTV greater than 95% (3.5% down): 0.55% annual rate

- LTV less than or equal to 95% (5% or more down): 0.50% annual rate

Finally, your fha loan calculator must include property taxes and homeowners insurance. Property taxes in Kalamazoo County vary by township, but estimating around 1.3% of the home’s value is a reliable starting point. These escrow items, combined with your principal and interest, form your total monthly payment. Having a seasoned co-pilot to verify these numbers ensures your budget stays on course and avoids any mid-flight surprises.

Navigating Local Airspace: FHA Loan Limits and Taxes in Kalamazoo

Before you taxi to the runway, you need to understand your weight limits. For 2026, the FHA loan limit for single-family homes in Kalamazoo and Van Buren Counties is $512,500. This ceiling represents the maximum amount the government will insure for a standard purchase. If you’re eyeing a larger estate in Portage, you might encounter “jumbo” FHA territory where different rules apply for multi-unit properties. Reviewing a reliable FHA loan overview helps clarify how these limits protect both your investment and the lender’s risk.

Local weather patterns change quickly, and so do tax obligations. A national bank might miss the fact that Michigan’s “homestead” property tax exemption can slash your annual tax bill by nearly 48% compared to a non-primary residence. This exemption significantly alters the results of your fha loan calculator. We provide the personal attention and respect needed to ensure your math reflects your actual zip code, not just a generic national average. A local lender understands these “wind shears” in the financial market and helps you adjust your flaps accordingly. Partnering with the right FHA lenders in Michigan who specialize in the Kalamazoo and Portage markets ensures these local nuances are fully accounted for in your loan strategy.

Kalamazoo vs. Battle Creek: Property Tax Variances

Your monthly payment depends heavily on your school district’s millage rate. A home in the Kalamazoo Promise area often carries a different tax profile than a property in Battle Creek or rural Van Buren County. These variances shift your debt-to-income ratio and impact your total “lift.” To get an accurate fha loan calculator result, look up specific parcel taxes on the local county treasurer’s website. We’re here every step of the way to help you decode these local tax codes so your closing costs don’t cause a bumpy landing.

FHA Property Standards in West Michigan

FHA appraisers prioritize safety and structural integrity. In historic Kalamazoo neighborhoods like the Vine or Westnedge Hill, older homes often have “flight deck” issues like peeling lead paint or outdated electrical systems. If a house doesn’t pass the initial inspection, don’t scrub the mission. A renovation mortgage acts as a better flight plan for fixer-uppers. This allows you to bundle repair costs into your primary loan. You can learn more about these options in our guide on Navigating Your Purchase Mortgage in Kalamazoo: A 2026 Buyer’s Guide. We’ll help you determine if a property is ready for takeoff or if it needs a stint in the hangar for repairs.

FHA vs. Conventional: Choosing the Right Flight Path

Think of your credit score as the wind speed on the tarmac. When you’re preparing for takeoff, certain “wind speeds” make one flight path much smoother than the other. Many West Michigan buyers assume FHA loans are strictly for those with low credit scores. That’s a myth we need to ground immediately. While FHA is forgiving, it’s often a strategic choice for borrowers with solid income who simply need more flexible debt-to-income (DTI) ratios.

The “break-even point” usually appears around a 720 credit score. Below that mark, the fha loan calculator often shows a lower monthly payment because FHA interest rates are typically lower than Conventional rates for mid-range credit profiles. However, as your score climbs, Conventional loans begin to offer better lift. We look at every angle to ensure you aren’t paying more than necessary for your Kalamazoo home.

When FHA is Your Best Co-Pilot

If your DTI ratio is higher because of student loans or a car payment, FHA is often the only program that provides enough “flaps” to get you airborne. FHA guidelines allow for a DTI up to 56.9% in some cases, whereas Conventional loans usually stall out around 43% to 50%. This extra room provides neighborly reassurance for families who have the income but also have existing monthly obligations. To see how these numbers stack up against other local options, check out our Conventional Mortgages in Kalamazoo: A 2026 West Michigan Comparison Guide.

The “Catch”: When Conventional Wins

Conventional loans win the long game for high-credit flyers. The primary reason is Private Mortgage Insurance (PMI). On a Conventional loan, PMI can be canceled once you reach 20% equity in the home. With an FHA loan, the Mortgage Insurance Premium (MIP) usually sticks with you for the life of the loan if you put down less than 10%. When you use an fha loan calculator and see a great rate, you must factor in that permanent insurance cost. For those with scores above 740, the interest rate savings and the ability to eventually drop insurance make Conventional the clear winner. We always explore all options to find your specific best fit, ensuring your mortgage doesn’t become a heavy anchor.

Choosing between these paths requires precision. If you plan to move in five years, the FHA’s lifetime insurance might not matter as much as the lower initial interest rate. If this is your “forever home” in Portage or Kalamazoo, the Conventional path might save you $25,000 or more in insurance costs over a decade. Let’s look at your dashboard together and find the right heading.

Beyond the Calculator: Preparing for Takeoff with Jeremy Drobeck

Using an fha loan calculator is like practicing on a high-end flight simulator. It’s a vital first step to understand the mechanics of your monthly payment, but it doesn’t actually get you off the ground. To reach the skies in the 2026 Kalamazoo housing market, you need a certified flight plan. A formal pre-approval is that plan. It transforms estimated numbers into a concrete budget you can present to local Realtors with total confidence. While the calculator gives you a glimpse of the horizon, a consultation ensures your engines are ready for the climb.

Combining FHA with MSHDA Assistance

In Michigan, the MSHDA program acts as the extra flaps on your wings, providing the necessary lift for a smooth departure. For many first-time buyers in Kalamazoo and Portage, the 3.5% down payment required by FHA loans is the biggest barrier to entry. MSHDA assistance can often cover this entire amount, allowing you to keep your savings intact for home repairs or moving costs. Eligibility is based on specific local criteria:

- Income Limits: Your total household income must fall within the designated limits for Kalamazoo County, which are adjusted periodically based on census data.

- Sales Price Caps: The home must stay below the maximum allowable purchase price set by the state for our specific region.

- Primary Residence: This program is designed for those intending to live in the home, ensuring the “lift” goes to families and individuals building roots in our community.

There’s a profound sense of emotional relief when you realize those flaps are fully extended. Knowing your down payment is handled allows you to focus on the excitement of homeownership rather than the stress of a dwindling bank account. We’ll help you determine if you meet the requirements for these programs during your initial strategy session.

Start Your 1st Class Journey Today

Generic online tools can’t account for the specific property tax nuances in the Stuart Neighborhood or the insurance variables for homes near West Lake. You need a seasoned co-pilot who understands the local terrain. My team provides the personal attention and respect you deserve, ensuring your “GPS” is calibrated for the Kalamazoo area. We’re here every step of the way to verify your numbers and troubleshoot any turbulence before it affects your closing date.

Take control of your financial future right now. Start by using the fha loan calculator to see what’s possible. Once you have your baseline, call today for your mortgage consultation. We’ll look at your specific situation, explore all options, and ensure you’re cleared for departure. Your journey to a new home in Kalamazoo starts with a single, well-planned step.

Clear the Runway for Your Kalamazoo Home

Navigating the Kalamazoo real estate market requires more than just a map; it needs a solid flight plan. You’ve explored how FHA math provides that extra lift for your down payment and how local tax rates in Kalamazoo County impact your monthly bottom line. While an fha loan calculator is a vital tool for your pre-flight check, the real precision comes from expert navigation. Jeremy Drobeck (NMLS #130762) brings over 20 years of local West Michigan mortgage expertise to your side of the cockpit. As part of the Division of Neighborhood Loans, Inc. (NMLS #222982), he ensures your transition from renter to homeowner is handled with 1st Class care.

Don’t leave your 2026 homeownership goals to chance. Whether you’re comparing flight paths between FHA and conventional loans or checking local limit updates, having a seasoned co-pilot makes all the difference. We’re here to monitor the gauges and handle the heavy lifting so you can focus on the view from your new front porch. Ready for takeoff? Get your personalized FHA loan consultation in Kalamazoo today!

We look forward to helping you reach your destination with confidence and local expertise.

Frequently Asked Questions

What is the minimum credit score for an FHA loan in Michigan in 2026?

To qualify for the maximum 96.5% financing in 2026, you generally need a minimum credit score of 580. If your score lands between 500 and 579, you can still get off the ground with a 10% down payment. Think of your credit score as your pre-flight weather report; it determines if we have a clear path for takeoff or if we need to adjust our flight plan for a smoother journey. For a complete breakdown of all the 2026 loan requirements for FHA in the Kalamazoo area, including updated credit, income, and property standards, our detailed guide has you covered.

Can I use an FHA loan to buy a house in Portage with 0% down?

You can’t get a standard FHA loan with 0% down in Portage, but you can pair it with MSHDA assistance to reach that goal. The FHA requires a 3.5% down payment by default. However, MSHDA offers up to $10,000 in down payment assistance for eligible Michigan buyers. These programs act like extra flaps on a wing, providing the necessary lift to reach your destination without a large cash reserve.

How much is the FHA mortgage insurance premium (MIP) monthly?

The monthly FHA mortgage insurance premium typically costs 0.55% of the loan amount annually for most buyers putting 3.5% down. For a $200,000 mortgage, this adds about $91.67 to your monthly payment. Using our fha loan calculator helps you see exactly how this fee impacts your monthly fuel burn so you can budget with total precision. It ensures there are no surprises once you are airborne.

What are the FHA loan limits for Kalamazoo County in 2026?

The 2024 FHA loan limit for single-family homes in Kalamazoo County is $498,257, which serves as the baseline for 2026 projections. These limits are adjusted annually by HUD based on local median home prices in the Michigan market. Staying within these boundaries ensures your loan remains eligible for FHA backing. It’s like checking the weight limits on a cargo plane before we clear you for departure from the runway.

Can I include my closing costs in the FHA loan amount?

You cannot directly roll your closing costs into the FHA loan amount, but you have other options to cover them. FHA guidelines allow sellers to contribute up to 6% of the purchase price toward your costs. This strategy keeps your out-of-pocket expenses low and manageable. Our team helps you navigate these negotiations so you don’t run out of runway before you even reach the closing table for your new home.

Is an FHA loan better than a conventional loan for a first-time buyer in Battle Creek?

An FHA loan is often better for Battle Creek buyers with credit scores below 680 or higher debt ratios. Conventional loans usually require higher scores to secure the best rates and lower insurance costs. If your financial profile has a few bumps, the FHA program provides a much smoother landing. We look at both flight paths to see which one gets you home with the most stability and safety.

How do I use an FHA loan calculator to estimate my MSHDA benefits?

You can use an fha loan calculator by entering the full purchase price and 3.5% down payment, then adjusting your cash to close for the MSHDA contribution. MSHDA provides a $10,000 flat-rate loan in many Michigan areas. Subtracting this amount from the calculator’s estimated total shows your true out-of-pocket cost. It’s like using a GPS to find the most efficient and affordable route to your final destination.

What happens if the house I want in Kalamazoo doesn’t pass the FHA inspection?

If a Kalamazoo home fails the FHA inspection, the seller must typically complete the required safety repairs before the loan can close. These inspections focus on health and safety, such as peeling paint or structural issues. If the seller won’t fix them, we can sometimes explore a repair escrow or a renovation loan. We won’t let a few mechanical issues ground your dreams of owning a home in our community.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”