7 Signs I’m Financially Ready to Buy a House: Your 2026 Readiness Flight Plan

The 20% down payment isn’t a safety requirement; it’s an outdated flight manual that keeps too many capable pilots grounded. In a 2026 market where Michigan home values have climbed to a median of $273,300, waiting to save a massive lump sum can feel like chasing a horizon that keeps moving. You’re likely looking for the specific signs I’m financially ready to buy a house while staring at 30-year fixed rates averaging 6.57%. It’s natural to feel some turbulence when headlines describe the current housing climate as shifty. However, your readiness depends on your own cockpit instruments rather than just the national weather.

We know that the transition from renting to owning feels like a high-stakes takeoff. You want to ensure you have enough lift to clear hidden costs like property taxes or PMI without draining your emergency reserves. This article provides a clear flight plan to validate your financial stability. We’ll debunk the down payment myth by exploring 3.5% FHA options and give you a definitive checklist to help you decide if it’s time to taxi to the runway. You’ll gain total control over the mortgage process and the confidence to know exactly when you are cleared for departure.

Key Takeaways

- Calibrate your financial cockpit by aiming for a 740+ credit score and keeping your debt-to-income ratio light enough for a safe takeoff.

- Discover the specific signs I’m financially ready to buy a house by measuring your cash liquidity and debt management against current 2026 market standards.

- Understand how low-down programs like FHA or Conventional loans provide the necessary lift for today’s buyers, proving the 20% down rule is an outdated manual.

- Prepare for the maintenance runway by setting aside 1% to 2% of your home’s value for repairs while accounting for the 2.7% property tax inflation cap in Michigan.

- Upgrade from a pre-qualification glider to a pre-approval jet engine to prove you have the mechanical power to close in a competitive seller’s market.

The Pre-Flight Checklist: What Financial Readiness Looks Like in 2026

Financial readiness in 2026 isn’t just about a single number on a screen. It’s the moment when your debt management, credit health, and cash liquidity all align to provide a stable platform for takeoff. In previous years, you might have been able to fly on a wing and a prayer, but the current 2026 market demands a more disciplined flight check. Gaining a baseline understanding mortgage loans is your first step toward ensuring your financial instruments are calibrated correctly. It’s about knowing your specific numbers before you ever step into a showroom or an open house.

There’s a critical distinction between being ‘Mortgage Ready’ and ‘Life Ready.’ A lender might clear you for a purchase mortgage based on your paperwork, but only you can decide if the monthly payment feels like a comfortable glide or a stressful climb. This shift from tenant to owner requires a new psychological perspective. As a tenant, someone else handles the maintenance turbulence. As an owner, you are the chief engineer. This is why your ’emergency altitude’—the cash reserve you keep after closing—is one of the most vital signs I’m financially ready to buy a house.

The Difference Between ‘Can Buy’ and ‘Should Buy’

A bank’s maximum loan amount represents your absolute ceiling, but it shouldn’t necessarily be your safe cruising altitude. You need to account for long term career stability and the economic outlook of 2026. If your industry is facing headwinds, taking on a 30 year mortgage anchor might not be the right move. Assess your lifestyle choices carefully. If you value the flexibility to move across the country on short notice, the commitment of homeownership might feel more like a weight than a wing. Real readiness means your mortgage fits into your life; your life shouldn’t have to shrink to fit your mortgage.

Why 2026 is the Year of the ‘Strategic Buyer’

Strategic buyers understand that 2026 presents unique challenges and opportunities. In areas like Kalamazoo, local market conditions and 30 year fixed rates averaging between 6.3% and 6.57% influence your monthly buying power every single day. You must also account for the 2.7% property tax inflation multiplier recently confirmed for Michigan homeowners. These factors impact your initial escrow requirements and your long term budget. If you’re looking for signs I’m financially ready to buy a house, look for a deep understanding of these local variables. Waiting for the perfect economic climate often means missing the right house while inventory remains tight.

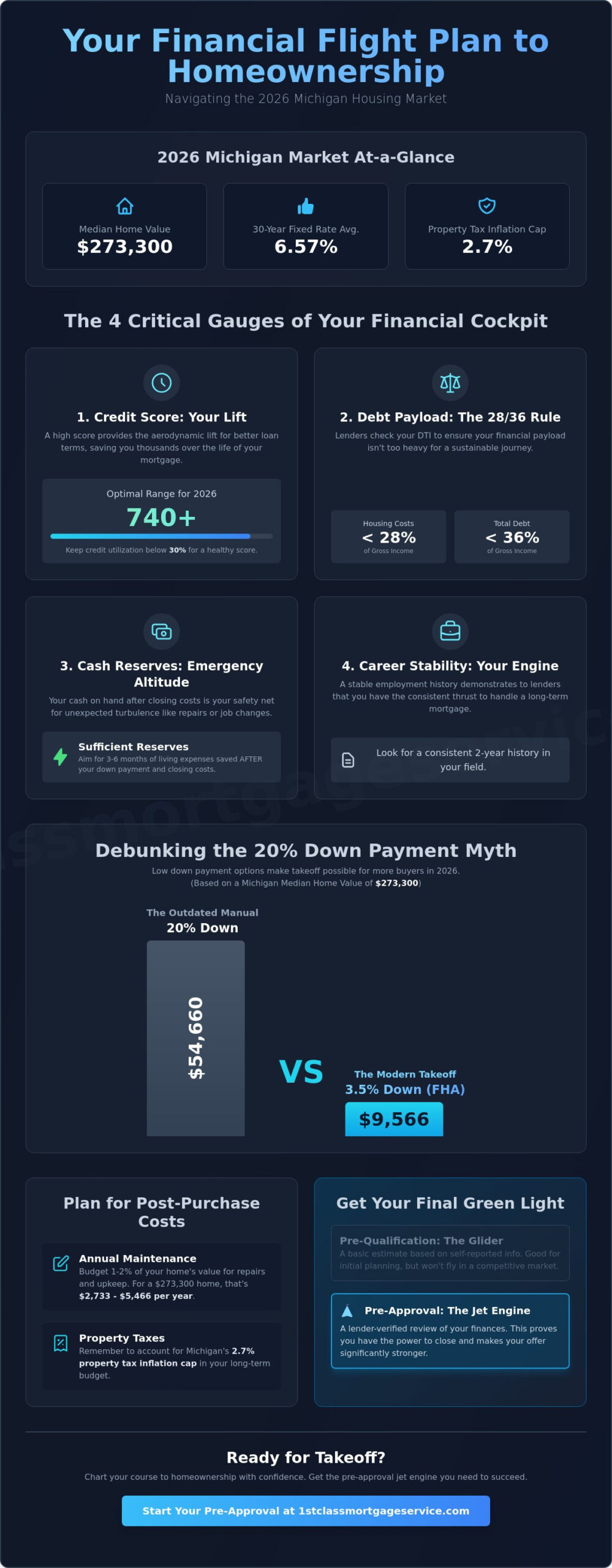

The 4 Critical Gauges of Your Financial Cockpit

Before you clear the tower for takeoff, you must ensure your internal instruments are reading correctly. Reviewing a financial readiness checklist helps you identify the specific signs I’m financially ready to buy a house before you commit to a long term loan. In the 2026 market, where 30 year fixed rates sit between 6.3% and 6.57%, precision is your best ally. Your credit, debt, cash, and career are the four engines that keep your homeownership journey airborne. If even one engine is sputtering, your entire flight plan could face an unscheduled landing.

Calibrating Your Credit Score for Maximum Lift

Your credit score is the primary source of lift for your mortgage application. While you can technically qualify for an FHA mortgage with a score as low as 580, aiming for 740 or higher is the goal for 2026. This higher calibration allows you to access the most competitive interest rates, potentially saving you tens of thousands of dollars over the life of the loan. You should also practice credit seasoning by avoiding any new lines of credit or large purchases in the six months leading up to your application. Credit utilization is the ratio of your outstanding credit card balances to your total credit limits, and keeping this under 30% is a primary driver of a healthy mortgage score. If you’re unsure where your gauges currently sit, a quick consultation for a purchase mortgage can provide the clarity you need.

The 28/36 Rule: Measuring Your Debt Payload

Lenders look at your debt to income (DTI) ratio to ensure your financial payload isn’t too heavy for a safe flight. The 28/36 rule is a neighborly guideline: your housing costs shouldn’t exceed 28% of your gross monthly income, and your total debt payments shouldn’t exceed 36%. In 2026, many buyers find that student loans and car payments act as significant drag on their eligibility. These monthly obligations reduce the amount of capital available for your mortgage payment. To lighten the load, consider paying down high interest credit cards or smaller installment loans before approaching a lender. This improves your back end ratio and gives you more breathing room in your monthly budget.

Finally, your liquid reserves and employment trajectory provide the fuel and thrust for your journey. You’ll need cash for closing costs and a maintenance runway of 1% to 2% of the home’s value, which in Michigan means having several thousand dollars ready for unexpected repairs. Consistent employment is one of the ultimate signs I’m financially ready to buy a house because it guarantees the ongoing thrust needed to maintain your investment. Lenders typically look for a two year history of stable income to ensure you can handle the long term commitment of a mortgage.

Debunking the 20% Down Payment Barrier in Michigan

Many prospective pilots believe they need a massive fuel reserve before they can even pull onto the runway. The idea that you must have 20% down is an outdated flight manual that doesn’t reflect the 2026 housing market. For a median priced Michigan home of approximately $273,300, a 20% down payment would be nearly $55,000. That’s a high altitude for most first time buyers to reach. Instead of waiting years to save that amount, modern programs provide the lift you need with much lower entry requirements. Understanding these options is one of the clearest signs I’m financially ready to buy a house because it shows you’ve moved beyond myths into practical planning.

Programs like the FHA mortgage allow for down payments as low as 3.5%, while certain conventional mortgage options require only 3%. These pathways significantly lower the barrier to entry, allowing you to begin building equity sooner. While you’ll likely pay Private Mortgage Insurance (PMI) with less than 20% down, this cost is often lower than the rate of home price appreciation. In Michigan, average home values increased by 4.2% over the past year. If you wait to save an extra $40,000, the house you want might cost $11,000 more by the time you’re ready to buy.

MSHDA and Local Assistance: Your Extra Engine

Local resources can act as a secondary engine to help you clear the tree line. There are several Michigan first time home buyer programs designed to bridge the gap for buyers in Kalamazoo and Portage. MSHDA down payment assistance can provide the necessary capital to cover your initial costs, making homeownership accessible even if your personal savings are still growing. For those in eligible rural areas, a USDA mortgage offers a zero down flight path, while veterans can utilize the VA mortgage to achieve 100% financing without the burden of monthly PMI. These specialized tools ensure your journey doesn’t stall due to a lack of upfront cash.

Calculating the Real Cost of Waiting

Renting is essentially paying a 100% interest rate with zero equity buildup. When you compare the cost of PMI, which typically ranges from 0.46% to 1.50% of the loan amount, against the 4.2% appreciation we’ve seen in Michigan, the math often favors an earlier purchase. Waiting for the perfect financial scenario can result in being priced out of the market entirely. Use the table below to see how different down payment levels impact your initial investment for a median priced Michigan home of $273,300.

| Down Payment % | Cash Required | Monthly PMI | Equity Path |

|---|---|---|---|

| 3% (Conventional) | $8,199 | Required | Immediate |

| 3.5% (FHA) | $9,565 | Required | Immediate |

| 20% (Traditional) | $54,660 | $0 | Immediate |

Seeing these numbers clearly is one of the primary signs I’m financially ready to buy a house. It proves you are looking at the total cost of the journey rather than just the ticket price. By leveraging the right assistance programs, you can achieve a stable takeoff much sooner than you think.

Beyond the Mortgage: Signs You Can Afford the ‘Hidden’ Costs

Your flight plan isn’t complete until you account for the weight of your cargo. While your monthly principal and interest payment is the most visible part of your budget, the hidden costs of homeownership can cause a sudden loss of altitude if you aren’t prepared. True signs I’m financially ready to buy a house include having a dedicated maintenance runway. Industry experts suggest setting aside 1% to 2% of your home’s value every year for repairs and upkeep. For a median priced Michigan home of $273,300, this means budgeting between $2,733 and $5,466 annually just to keep your property in peak flying condition.

Escrow realities in 2026 also require careful navigation. Michigan property taxes are subject to a 2.7% inflation multiplier for existing owners, but as a new buyer, you must prepare for the “uncapping” event. When a property changes hands, its taxable value resets to the current market value, which can lead to a significant jump in your monthly payment. Combining this with rising home insurance premiums means your all-in housing cost might be higher than a generic online calculator suggests. If your budget can’t absorb these fluctuations without stress, you might need more time to stabilize your finances.

The Kalamazoo & Portage Escrow Forecast

Local millage rates in Battle Creek, Portage, and Kalamazoo vary significantly, impacting your monthly “all-in” payment. You shouldn’t just look at the list price; you must look at the specific tax history of the neighborhood. Because market conditions shift quickly, you should check current mortgage rates in Kalamazoo weekly before you lock in your loan. This ensures your escrow calculations are based on the most recent data available, preventing any surprises during the final approach to closing.

The Post-Closing Safety Net

One of the most reliable signs I’m financially ready to buy a house is the presence of a post-closing safety net. Your bank account shouldn’t hit zero the moment you get the keys. You need an “Emergency Altitude” fund of three to six months of living expenses to survive a temporary stall in income or a major mechanical failure, like a furnace replacement. Additionally, plan for the “New Home Tax,” which includes the inevitable trips to the hardware store for tools, window treatments, and furniture. A well-prepared buyer has the thrust to handle these initial expenses while maintaining a safe financial cushion. If you’re ready to see how these costs fit into your specific scenario, it’s time to explore a purchase mortgage with a guide who understands the local landscape.

Charting Your Course: Why Pre-Approval is Your Final Green Light

You have checked your gauges, calculated your payload, and accounted for the maintenance runway. One of the most definitive signs I’m financially ready to buy a house is the transition from self-assessment to professional validation. While your personal spreadsheets provide a sense of direction, a mortgage pre-approval is the official flight clearance that proves to sellers you have the thrust to reach the finish line. In a Michigan market where homes often spend only 14 days on the market, this document is your most powerful tool for securing a property in a competitive landscape.

It is vital to understand the difference between a pre-qualification and a pre-approval. Think of a pre-qualification as a glider. It is based on unverified information and provides a general idea of your path, but it lacks the mechanical power to handle high-pressure situations. A pre-approval is a jet engine. It involves a rigorous review of your actual financial documents, providing a verified commitment that carries weight with sellers and real estate agents alike. When you present a pre-approval letter, you aren’t just expressing interest; you’re proving that your financial instruments are fully operational.

Your Navigator’s Role in the Journey

A local Michigan lender acts as your Air Traffic Controller, guiding you through the complex airspace of lending regulations and market shifts. Jeremy Drobeck and the Treadstone team provide end-to-end support specifically tailored to the West Michigan landscape. Whether you are looking in Kalamazoo, Portage, or Battle Creek, having a navigator who understands local millage rates and property tax nuances is invaluable. Personalized care beats a big bank algorithm every time because a local expert can handle unconventional scenarios that automated systems might reject. We view the mortgage process as a partnership, ensuring you remain in total control of your flight path from application to closing.

Ready for Takeoff? Your Next 3 Steps

If you have identified the signs I’m financially ready to buy a house, it is time to prepare for your final approach. Follow these three steps to secure your clearance:

- Step 1: Organize your Flight Log. Gather your W2s, recent bank statements, and tax returns. Having these documents ready allows for a smoother, faster verification process.

- Step 2: Review specialized options. Explore programs that fit your specific needs, such as FHA loans in Michigan, which offer flexibility for those with smaller down payments.

- Step 3: Schedule your meeting. A professional consultation will confirm your readiness and help you lock in a strategy that aligns with 2026 interest rates.

Your journey toward homeownership doesn’t have to be a solo flight. With the right preparation and a seasoned navigator by your side, you can clear the obstacles and achieve a safe, successful landing. Schedule your 2026 Mortgage Flight Plan with Jeremy Drobeck today!

Clearing the Runway for Your 2026 Home Purchase

You have mapped out the 2026 landscape and calibrated your financial gauges. You now know that the outdated 20% down payment rule doesn’t define your capacity to fly. Instead, true readiness comes from a disciplined approach to credit, a solid maintenance runway, and a clear understanding of local escrow realities. Recognizing these signs I’m financially ready to buy a house is the first step toward a successful landing in the West Michigan market. You’ve moved beyond the anxiety of the unknown and into a position of expert control.

It’s time to move from the planning phase to the cockpit. Jeremy Drobeck has served the Kalamazoo, Portage, and Battle Creek communities since 2002. As an expert in MSHDA and local Michigan assistance programs, he provides the steady, neighborly guidance you need to navigate this journey. We are a division of Neighborhood Loans, Inc. (NMLS #222982) and remain present throughout the entire duration of your process. Start your personalized 2026 Mortgage Flight Plan with Jeremy Drobeck today. We look forward to helping you achieve your homeownership goals with precision, transparency, and care.

Frequently Asked Questions

Is a 620 credit score really enough to buy a house in 2026?

Yes, you can qualify for an FHA mortgage or certain conventional loans with a 620 score, but it isn’t the ideal altitude for the best rates. In 2026, a 580 score is the minimum for a 3.5% down FHA loan. However, a 620 score often results in higher monthly premiums and interest costs compared to the 740 goal discussed earlier. It is a functional starting point, but not the peak performance level for your flight plan.

Can I buy a house if I have significant student loan debt?

You can certainly buy a house with student loan debt as long as your total debt to income (DTI) ratio remains within acceptable limits. Lenders calculate a portion of your balance as a monthly obligation, which acts as a payload on your borrowing power. If your income provides enough thrust to cover both your mortgage and your student loan payments, your debt won’t ground your homeownership journey.

How much cash do I actually need for closing costs in Michigan?

You should generally prepare for closing costs to range between 2% and 5% of the home’s purchase price. For a median priced Michigan home of $273,300, this means having extra liquid fuel beyond your down payment. These costs cover appraisals, title insurance, and initial escrow deposits. Checking for signs I’m financially ready to buy a house involves ensuring these funds are available before you commit to a purchase.

What is the ’28/36 rule’ and does every lender use it?

The 28/36 rule is a standard navigation guide where 28% of your gross income goes to housing and 36% to total debt, but not every lender follows it strictly. Some programs, like FHA mortgages, may allow for a DTI as high as 43% or even more in specific scenarios. It’s a baseline for stability, but your specific flight path might allow for more flexibility depending on your credit and cash reserves.

Should I pay off all my credit cards before applying for a mortgage?

You don’t necessarily need a zero balance on every card, but lowering your credit utilization is one of the primary signs I’m financially ready to buy a house. Paying off high interest balances improves your DTI and can boost your credit score for better lift. However, you should avoid closing old accounts or making major changes right before applying, as this can cause turbulence in your credit history.

What happens if my financial situation changes during the mortgage process?

If your income or debt changes during the process, you must notify your navigator immediately. Any new large purchases or a change in employment can stall your mortgage approval even after you’ve received a pre-approval. Lenders perform a final check of your financial instruments just before closing to ensure you are still cleared for takeoff. Keeping your finances stable during this period is critical for a successful landing.

Is MSHDA down payment assistance only for first-time buyers?

MSHDA down payment assistance is primarily for first time buyers, but it is also available to repeat buyers in certain targeted areas across Michigan. Eligibility depends on your income, the purchase price of the home, and your intended location. This program provides the extra momentum needed to clear the down payment barrier for many families in our local communities, regardless of their previous ownership history.

How long does a mortgage pre-approval stay valid in the Michigan market?

A mortgage pre-approval typically stays valid for 60 to 90 days in the Michigan market. Because interest rates and your financial data can shift, your lender will need to refresh your flight clearance if your home search takes longer. Staying in close contact with your guide ensures your pre-approval jet engine is always ready for a quick response when the right house appears in Kalamazoo or Portage.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”