FHA vs Conventional Loan for First Time Buyer in Portage MI: Your 2026 Flight Plan

What if the traditional advice you’ve heard about down payments is actually the very thing keeping your homeownership dreams grounded? Deciding between an FHA vs conventional loan for first time buyer in Portage MI often feels like preparing for a high-stakes takeoff. It’s completely natural to feel a bit of turbulence when you’re staring down credit requirements or confusing mortgage insurance terms. You want to ensure your financial foundation is secure before you leave the runway, yet the fear of rejection can make the whole process feel like a gamble rather than a significant life milestone.

We believe every neighbor deserves a clear flight plan that replaces anxiety with expert guidance. In this detailed comparison, you’ll discover which mortgage path provides the smoothest ascent for your specific situation in the 2026 market. We’ll break down the latest loan limits, compare monthly costs, and show you how to layer MSHDA assistance to give your down payment some extra lift. By the time we finish, you’ll have the confidence to choose the right loan and successfully pilot your way to a new front door in Portage.

Key Takeaways

- Prepare your 2026 pre-flight checklist by understanding the unique inventory of Portage neighborhoods and the latest lending limits for Michigan single-family homes.

- Compare the technical mechanics of an FHA vs conventional loan for first time buyer in Portage MI to see which path aligns with your specific credit profile and financial reserves.

- Decode the long-term costs of mortgage insurance and learn the exact maneuvers required to eventually remove these premiums as you build equity in your new home.

- Discover how to layer MSHDA down payment assistance into your loan structure, providing up to $10,000 in momentum to help you clear the hurdle of initial costs.

- Learn why a local mortgage navigator is essential for avoiding the appraisal turbulence that often grounds applications from large, impersonal online lenders.

Navigating the Portage Real Estate Market as a First-Time Buyer

Portage is a community built on precision and preparation. Entering the 2026 housing market without a strategic pre-flight checklist is like trying to pilot a plane without a flight plan. You’ll find a diverse inventory here, ranging from the established ranch homes in the 49002 area to the newer, multi-story builds spreading through 49024. Each property type reacts differently to your financing choice. When you’re weighing an FHA vs conventional loan for first time buyer in Portage MI, you aren’t just looking at interest rates. You’re analyzing how a local seller perceives your ability to reach the closing table without turbulence.

A local mortgage navigator acts as your air traffic controller. In a competitive multi-offer environment, the difference between being “cleared for landing” and a rejected offer often comes down to the strength of your pre-approval. While some sellers might prefer conventional loans for their perceived simplicity, an FHA insured loan is a powerful tool that provides the necessary lift for many buyers in our community, provided your navigator knows how to present it effectively to the listing agent. Your loan type dictates your offer’s momentum, and we’re here to ensure you have enough thrust to beat out the competition.

The 2026 Portage Housing Landscape

Kalamazoo County continues to see steady demand, and Portage remains a top-tier destination for first-time buyers. Home values have remained resilient, making the area a prime location for long-term equity growth. If you’re hunting for “FHA-friendly” properties, look for homes that have been well-maintained; FHA appraisals focus on safety and structural integrity. With the MSHDA sales price limit for most of Michigan sitting at approximately $251,699 in 2026, many Portage starters fit perfectly within these assistance parameters, allowing you to maximize your financial stability from day one.

Setting Your Homeownership Altitude

Before you start touring homes in West Michigan, you must define your budget with surgical precision. The shift from renter to owner is a significant life milestone. It requires moving from a mindset of a “monthly expense” to one of “asset management.” Neighborly reassurance is vital during this phase. You need a partner who views you as a future neighbor, not just a loan number. This supportive guidance ensures that when you find “the one,” your financial mechanics are already locked in, giving you the confidence to make a bold, winning offer.

FHA vs Conventional: The 2026 Technical Breakdown

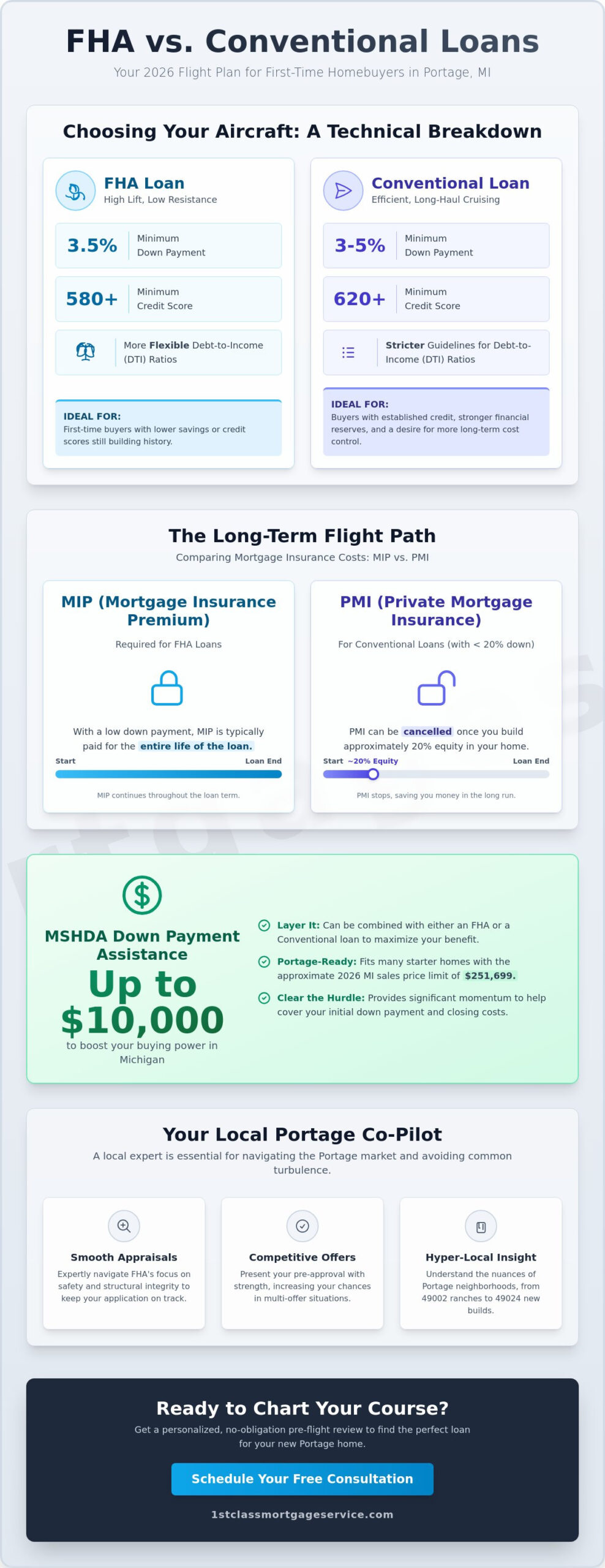

Choosing between an FHA vs conventional loan for first time buyer in Portage MI is like selecting the right aircraft for your specific payload. Each engine is designed for a different type of lift. FHA loans act as a powerful booster for buyers who might have a few marks on their credit history or limited cash reserves. Conversely, conventional loans offer an efficient cruise for those with established credit who want more control over their long-term costs. Understanding these mechanics is the first step in ensuring a successful takeoff.

The most immediate difference lies in the credit floor. An FHA loan typically requires a minimum score of 580 to qualify for the low down payment option. Conventional loans usually set the bar higher at 620. Beyond the score, FHA provides more flexibility with your Debt-to-Income (DTI) ratio. It allows for a “heavier” debt load, meaning you can often qualify even if you’re still paying down student loans or a car note. This flexibility is a vital component for many young professionals in West Michigan who are just starting their careers. If you’re unsure where your numbers land, you can schedule a pre-flight review to see which path fits your current financial standing.

FHA Loan Mechanics: High Lift, Low Resistance

The FHA path is famous for its 3.5% down payment standard. This low entry point serves as a reliable launchpad for many in Kalamazoo County. Because the federal government backs these loans, lenders feel more secure offering competitive terms to buyers with less-than-perfect credit. However, keep in mind that FHA appraisals are slightly more rigorous. Inspectors will look for specific safety issues in Portage homes, such as peeling paint or handrail stability, to ensure the property is sound. You can even combine this with Michigan Down Payment Assistance to further reduce your out-of-pocket costs at closing.

Conventional Loan Mechanics: Precision and Efficiency

Conventional loans aren’t just for those with 20% down. Many first-time buyers qualify for specialized programs requiring only 3% down. The primary advantage here is the “fuel efficiency” of your monthly payment. While FHA requires government insurance (MIP) for the life of the loan in many cases, conventional Private Mortgage Insurance (PMI) can eventually be cancelled once you reach 20% equity. Stronger credit scores unlock lower interest rates, which act as a tailwind for your long-term wealth. It’s a precise tool for those ready to maximize their financial momentum from the moment they get their keys.

Comparing the Long-Term Flight Path: MIP vs. PMI

Once you’ve cleared the initial hurdles of credit and down payments, you need to look at your long-term flight path. Mortgage insurance is the extra fuel needed to keep your loan airborne when you have less than 20% equity. For an FHA vs conventional loan for first time buyer in Portage MI, these insurance types function with very different mechanics. FHA requires a Mortgage Insurance Premium (MIP), while conventional loans utilize Private Mortgage Insurance (PMI). One is a permanent copilot for your journey, while the other can eventually be dropped to lighten your financial load.

FHA loans carry a unique upfront cost known as the Upfront Mortgage Insurance Premium (UFMIP). In 2026, this fee remains 1.75% of your base loan amount. Most Portage buyers choose to roll this into their total loan balance, but it’s important to remember that this increases your overall debt from day one. Conventional loans, by contrast, typically have zero upfront insurance fees. This difference often shifts the “break-even” point for homeowners depending on how long they plan to stay in the property. If you’re comparing the math, this FHA vs. Conventional Mortgage: The Real Cost Comparison provides a deeper look at the numbers for our local West Michigan market.

The Lifetime Cost of FHA Insurance

In 2026, if you put down the minimum 3.5% on an FHA loan, that MIP is a permanent fixture. It stays for the entire life of the loan. While the annual rate for most 30-year FHA loans is 0.55%, that monthly cost never disappears unless you eventually refinance into a conventional product. This is a common strategy for Portage residents; they use the FHA “boost” to get into the home and then switch flight paths once their equity has grown. For a neutral perspective on these requirements, you can consult this Consumer Financial Protection Bureau guide to FHA loans.

The Flexibility of Conventional PMI

Conventional PMI is far more agile. Your monthly PMI rate is tied directly to your credit score performance; higher scores mean lower insurance costs. The best part is the exit strategy. Once your loan-to-value ratio reaches 80%, you can request to drop the insurance. At 78%, the lender must terminate it automatically. Some buyers even opt for Lender Paid Mortgage Insurance (LPMI), where the insurance cost is baked into a slightly higher interest rate, allowing for a cleaner monthly statement without a separate insurance line item. It’s about choosing the level of precision that fits your financial comfort zone.

Layering Your Loan with Michigan Down Payment Assistance

Choosing between an FHA vs conventional loan for first time buyer in Portage MI is only half the battle. Even with a 3% or 3.5% down payment requirement, the initial cash outlay can feel like a heavy weight keeping you grounded. This is where the Michigan State Housing Development Authority (MSHDA) provides the necessary momentum. By layering your primary mortgage with state-level assistance, you can significantly reduce the amount of liquid capital you need to bring to the closing table. It’s about adding an extra engine to your aircraft to ensure you clear the runway with ease.

The MI Home Loan program is a standout feature for 2026. It offers up to $10,000 in down payment assistance as a zero-interest, zero-monthly-payment loan. This isn’t just a financial tool; it’s a stabilizer that allows you to keep more of your savings for life’s unexpected turbulence. You only repay this assistance when you sell the home, refinance, or pay off your primary mortgage. In Portage, where starter homes often fall within the MSHDA sales price limit of approximately $251,699, this program is a game changer. It requires a minimum credit score of 640 for FHA loans or 660 for conventional loans, ensuring that those who have prepared for the journey are rewarded with extra lift.

To see if your specific flight path qualifies for these state-level boosters, you can apply for a personalized MSHDA eligibility review today.

The MSHDA Flight Plan

Navigating MSHDA requirements requires attention to detail. In Kalamazoo County, there are specific income limits and purchase price caps you must stay within to maintain eligibility. Think of these as the technical specs for your aircraft. Additionally, you’ll need to complete a homebuyer education course. We view this as your “flight school,” where you learn the mechanics of homeownership to ensure a safe journey. For a deeper dive into these local options, check out our guide on Michigan First Time Home Buyer Programs: Your 2026 Kalamazoo Flight Plan.

Zero Down Payment Alternatives

If the MSHDA path doesn’t fit your coordinates, other zero-down options might provide the lift you need. For those looking at the outskirts of Portage or nearby rural areas, a USDA loan can be an excellent path, provided the property falls within designated zones. Veterans in West Michigan have access to VA loans, which remain the ultimate zero-down option with no monthly mortgage insurance. Finally, don’t overlook seller concessions. In the 2026 market, many Portage sellers are willing to cover a portion of your closing costs, giving your offer even more thrust toward the finish line.

Charting Your Course: Why a Local Portage Mortgage Expert Matters

Deciding between an FHA vs conventional loan for first time buyer in Portage MI is a significant financial maneuver. However, even the most advanced aircraft needs a seasoned navigator to handle the specific conditions of the local terrain. While national big-box lenders might offer a generic automated response, they often lack the community expertise required to anticipate the unique turbulence of the West Michigan market. You aren’t just looking for a loan; you’re looking for a partnership that ensures your offer is respected and your closing is secure.

This is where the “Jeremy Drobeck” difference becomes your greatest asset. We combine professional authority with neighborly reassurance, treating your home purchase as a shared mission rather than a cold transaction. Local expertise matters most when it comes to appraisals and seller negotiations. A local navigator understands why a home near West Lake might be appraised differently than a new build near Celery Flats. We provide end-to-end support, staying present from the initial pre-flight check until you’re safely across the threshold of your new home.

The Treadstone Advantage in West Michigan

We treat your closing date as a mission-critical deadline. In our office, meticulous care is the standard. There is no hidden fine print or unexpected cargo in your loan estimate; we prioritize directness and integrity above all else. This disciplined approach ensures that when you enter a multi-offer situation in Portage, your financing is a source of strength, not a point of failure. We remain by your side throughout the entire journey, providing a steady hand to guide you through every complex application step.

Your Next Steps to Homeownership

To get your custom flight plan started, you’ll need to gather your essential flight documents. This typically includes your most recent paystubs, tax returns, and bank statements. Our goal is to provide a 24-hour pre-approval, giving you the momentum needed to make an offer the moment you find the right property. Don’t let confusion over mortgage mechanics keep you grounded. You can Schedule your Portage mortgage consultation with Jeremy Drobeck today and take the first step toward a successful landing in your first home.

Clearing the Runway for Your First Portage Home

Your journey toward homeownership doesn’t have to be a solo flight through turbulent weather. By now, you understand that the choice between an FHA vs conventional loan for first time buyer in Portage MI depends on your specific financial altitude and long-term goals. Whether you need the high-lift boost of an FHA loan or the efficient cruise of a conventional mortgage, layering your path with MSHDA assistance can provide the momentum needed to clear the initial hurdles of costs and credit.

With over 20 years of West Michigan lending expertise, Jeremy Drobeck and the team are ready to act as your dedicated navigators. As an expert in MSHDA and first-time buyer programs, Jeremy provides the neighborly reassurance and professional precision you deserve. We’re a division of Neighborhood Loans, Inc. (NMLS #222982), and we’re committed to being present for every mile of your trip. Don’t leave your financial future to chance when you can have a seasoned guide at the controls. It’s time to Start Your Portage Homeownership Flight Plan with Jeremy Drobeck and secure your place in the local community. Your new front door is waiting for a smooth landing.

Frequently Asked Questions

Is FHA or Conventional better for a first-time buyer with a 640 credit score?

FHA is typically the more efficient path for a 640 score because it often provides lower interest rates and more flexible debt-to-income limits. While you can qualify for a conventional loan at 620, the private mortgage insurance costs for a 640 score can be quite high. Choosing an FHA vs conventional loan for first time buyer in Portage MI with this score often results in a lower monthly payment, giving you more financial lift as you start your journey.

Can I use MSHDA down payment assistance with a Conventional loan in Portage?

Yes, you can layer MSHDA assistance with a conventional mortgage, but the technical requirements are stricter. MSHDA requires a minimum credit score of 660 for conventional loans, compared to 640 for FHA. This combination is an excellent way to drop the “extra weight” of a down payment while still securing the long-term benefit of cancellable mortgage insurance once you reach 20% equity in your home.

What is the minimum down payment for an FHA loan in Michigan in 2026?

The standard launchpad for an FHA loan in 2026 is a 3.5% down payment. This applies to any borrower with a credit score of 580 or higher. For a typical starter home in Kalamazoo County, this lower entry point makes homeownership accessible without requiring years of aggressive saving. It’s a reliable way to get your flight plan off the ground with minimal resistance.

Does a Conventional loan always require a 20% down payment?

No, first-time buyers can often secure a conventional loan with as little as 3% down. Programs like HomeReady or Home Possible are designed to provide maximum momentum for those with established credit but limited cash reserves. While 20% down allows you to bypass private mortgage insurance entirely, the 3% option is a popular alternative that helps you enter the Portage market much sooner.

How do FHA appraisal requirements differ for older homes in Kalamazoo?

FHA appraisers follow a specific safety checklist that can be more rigorous than conventional standards, especially for the historic properties found in West Michigan. They prioritize “health and safety” issues like peeling lead-based paint, lack of handrails on stairs, or outdated electrical systems. We suggest viewing these requirements as a safety inspection for your aircraft; they ensure your new home is structurally sound and safe for your family.

Can I remove the mortgage insurance from an FHA loan without refinancing?

For most FHA loans with a 3.5% down payment, the mortgage insurance premium is a permanent copilot for the life of the loan. If you put down 10% or more, the insurance can be removed after 11 years. Otherwise, the only way to drop this cost is to eventually refinance into a conventional loan once your home’s value has increased enough to reach 20% equity.

What are the closing costs for a first-time buyer in Portage, MI?

Closing costs typically range between 2% and 5% of the home’s purchase price. These costs cover essential flight services like title insurance, government recording fees, and property tax escrows. We always look for ways to minimize your out-of-pocket expenses, such as negotiating seller concessions or using MSHDA grants to cover these technical fees at the end of your journey.

How long does the mortgage approval process take with Jeremy Drobeck?

We aim for a 24-hour pre-approval to ensure you’re ready to make an offer the moment you find the right property. Once you have an accepted offer, the full journey to the closing table usually takes between 30 and 45 days. Our team provides end-to-end support throughout this duration, keeping you informed of every milestone so there are no surprises during your final approach.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”