How Much House Can I Afford on a $70k Salary in Michigan? (2026 Guide)

What if I told you that a $70,000 annual income in the Great Lakes State doesn’t just keep you grounded, but actually gives you the clearance to land a home priced up to $300,000? Determining how much house can I afford on $70k salary in Michigan requires more than a basic calculator; it requires a specialized flight path. You’ve likely felt the turbulence of 6.49% mortgage rates and heard whispers about the Michigan property tax “pop-up” effect. It’s natural to worry that your budget might stall before you reach the closing table. You want a home that fits your life, not a mortgage that leaves you feeling house-poor.

We’re here to help you engineer a precise plan for your home-buying journey. You’ll discover how local market trends and the 28/36 rule impact your purchasing power in 2026. We’ll also explore how MSHDA programs can provide up to $10,000 in down payment assistance to give your budget extra lift. This guide breaks down the essential numbers, from property tax rates to specific loan limits, to ensure you start your pre-approval process with a clear view of the horizon.

Key Takeaways

- Learn how the 28/36 rule sets your target monthly housing budget at approximately $1,633 based on a $5,833 gross monthly income.

- Pinpoint the exact price range and market variables that dictate how much house can I afford on $70k salary in Michigan without becoming house-poor.

- Identify high-value neighborhoods in West Michigan, including Kalamazoo and Battle Creek, where your income provides the most purchasing power.

- Understand how strategic tools like MSHDA Down Payment Assistance and FHA mortgages provide the necessary lift to overcome credit and cash-on-hand barriers.

- See why local lending expertise is the critical component for navigating the final approach to a successful closing in a competitive environment.

Calculating Your Michigan Home Buying Power on $70,000

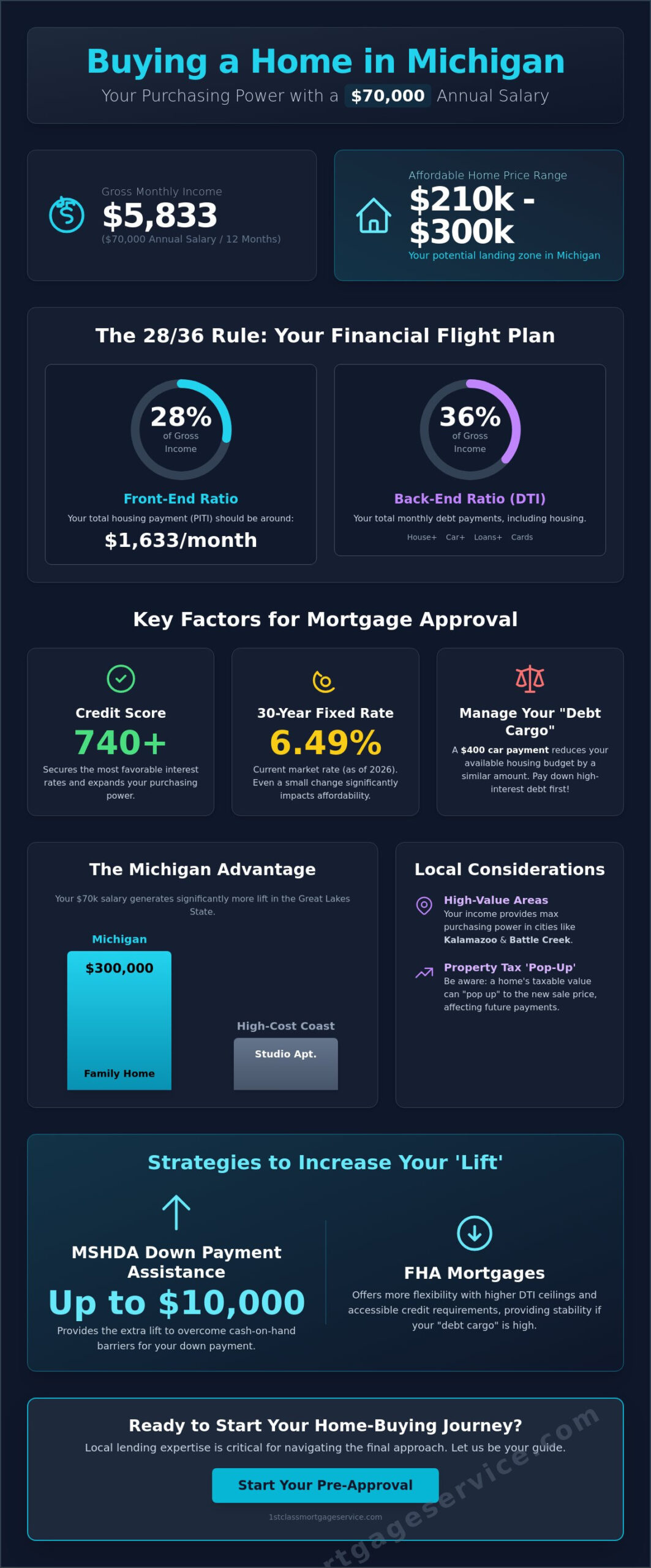

Your $70,000 annual salary serves as the primary fuel for your homeownership journey. When we break the math down, that is roughly $5,833 in gross monthly income. Understanding how much house can I afford on $70k salary in Michigan starts with viewing this number through the same lens as a mortgage lender. They don’t look at your take-home pay initially; they focus on your gross earnings to establish your baseline capacity.

Michigan provides a distinct advantage compared to high-cost coastal regions. Here, your dollar generates significantly more lift. While that same income might barely cover a studio apartment in Seattle, in the Great Lakes State, it positions you to look at a purchase price range between $210,000 and $290,000. Your specific landing spot within that range depends on your current interest rate and how much other debt you carry.

The 28/36 Rule: Your Standard Flight Path

Think of the 28/36 rule as your essential flight instruments. The front-end ratio focuses on the 28% mark. This means your total housing payment, including taxes and insurance, should stay around $1,633 per month. The back-end ratio, typically capped at 36%, considers your total Debt-to-income ratio (DTI). This includes car loans, credit card minimums, and student debt. If your other monthly payments are low, you have more cargo space for a larger mortgage. However, you must account for the cash needed for the transition. We recommend calculating closing costs in Michigan early so you aren’t surprised by the funds required at the finish line.

Gross vs. Net Income: Navigating Your Real Cash Flow

Lenders qualify you based on gross income, but your daily life happens in the “net” world. Your take-home pay is what actually sustains your household. Determining how much house can I afford on $70k salary in Michigan requires you to look at local headwinds like state income tax. If you are searching in cities like Battle Creek, you’ll also need to factor in local municipal taxes. These small deductions can impact your monthly breathing room. Additionally, 2026 utility cost projections in West Michigan suggest a slight uptick in seasonal heating and cooling expenses. Accounting for these real-world costs ensures your flight remains steady and you never feel pressured by your mortgage payment.

The Mechanics of Mortgage Approval: DTI, Credit, and Rates

Think of your mortgage approval as a flight clearance. Your income provides the necessary lift, but your existing debt represents the cargo weight. Determining how much house can I afford on $70k salary in Michigan requires a precise look at your Debt-to-Income (DTI) ratio. This metric is how lenders measure your ability to manage monthly payments alongside your recurring financial obligations. In 2026, lenders are looking for a balanced manifest; they want to see that your total monthly debts don’t overwhelm your $5,833 gross monthly income.

Your credit score acts as the fuel quality for your journey. A score of 740 or higher typically secures the most efficient interest rates, which directly expands your purchasing power. In the current market, where the 30-year fixed rate is verified at 6.49%, every fraction of a percent matters. Reviewing current mortgage rates in Kalamazoo allows you to adjust your navigation before you start touring homes, ensuring your budget remains realistic as market conditions shift.

Managing Your Debt Cargo

Student loans, car payments, and credit card balances act as heavy ballast. They reduce the amount of income available to support a mortgage payment. For instance, a $400 car payment effectively lowers your available housing budget by a similar amount. FHA loans often provide more flexibility here, allowing for a higher DTI ceiling than Conventional loans. If you want to increase your housing lift, paying down high-interest revolving debt before applying is a strategic move. You might find that exploring an FHA mortgage offers the stability you need if your debt cargo is currently higher than you’d like.

Michigan Property Taxes: The ‘Pop-Up’ Effect

One unique Michigan headwind that national calculators often miss is the property tax “pop-up” or uncapping. Under state law, property tax increases are limited for the current owner. However, when a home is sold, the taxable value resets to 50% of the home’s true cash value. This means your neighbor’s $2,000 tax bill isn’t a reliable indicator of what you’ll pay. Without expert navigation, this surprise can add hundreds of dollars to your monthly payment, potentially grounding your budget. In Kalamazoo County, we help you estimate these future costs so your escrow account remains stable throughout your first year and beyond.

What a $70k Salary Buys in the 2026 Michigan Real Estate Market

National real estate headlines often paint a bleak picture of affordability, but West Michigan offers a much smoother flight path for buyers. While the average home value in Michigan sits at $263,590 as of April 2026, your $70,000 income remains a powerful asset in our local landscape. Determining how much house can I afford on $70k salary in Michigan becomes much clearer when you look at the specific runways available in Kalamazoo, Portage, and Battle Creek. Each city offers a different level of lift depending on your priorities for space, school districts, and neighborhood character.

Neighborhood Comparison: West Michigan Value

Kalamazoo remains a prime destination for the $70k earner. In neighborhoods like Milwood or the Edison district, you can frequently find well-maintained 3-bedroom, 2-bathroom homes within your $210,000 to $290,000 target range. Portage offers a slightly higher altitude of competition. Because of the high demand for its school districts, you might find yourself choosing between a smaller, move-in-ready ranch or a larger home that requires some cosmetic updates. Battle Creek serves as a reliable safe harbor for budget-conscious buyers. Here, your dollar often stretches the furthest, allowing you to secure more square footage or a larger lot while keeping your monthly payment well below the 28% threshold.

2026 Market Trends: Inventory and Competition

The current market moves quickly. Verified data from March 2026 shows that Michigan homes go to pending in an average of just 14 days. With 27% of sales closing above list price, you cannot afford a delayed takeoff. This environment makes your pre-approval letter more than just paperwork; it is your official boarding pass. Without it, your offer likely won’t even be considered by sellers who are navigating multiple bids. To gain an edge, many buyers are looking at “renovation-ready” properties. These homes allow you to build equity faster by making improvements over time rather than paying a premium for someone else’s recent upgrades.

If your down payment savings feel like they are stalling, remember that Michigan offers specific tools to help you gain altitude. Programs like the MI 10K Down Payment Assistance provide $10,000 in support for eligible buyers. This extra capital can be the difference between settling for a starter home and landing the property that truly fits your long-term needs. We monitor these local inventory shifts daily to ensure our clients are positioned for a successful landing, no matter how competitive the market becomes.

Strategies to Increase Your ‘Lift’: Down Payment Assistance and Loan Programs

Securing a home on a $70,000 income often requires more than just a standard savings plan; it demands the right mechanical advantage. Many buyers stall because they believe a 20% down payment is the only way to clear the runway. In reality, several specialized programs act as flight boosters, allowing you to gain altitude with significantly less cash upfront. Understanding how much house can I afford on $70k salary in Michigan involves evaluating these tools to see which one provides the most efficient path for your specific financial profile.

The FHA Mortgage remains a popular choice for Michigan residents because of its accessible 3.5% down payment requirement and flexible credit standards. If you are looking in more rural areas surrounding Kalamazoo or Battle Creek, a USDA mortgage might offer a 0% down option, provided the property meets geographic requirements. For those with higher credit scores, a Conventional mortgage with just 3% down can offer lower long-term costs by reducing private mortgage insurance (PMI) faster.

MSHDA: Your Michigan Flight Booster

The Michigan State Housing Development Authority (MSHDA) offers a secret weapon for those in the $70,000 income bracket. With household income limits for 2026 reaching approximately $121,320 in areas like Wayne County, a $70k earner is well-positioned to qualify. The primary benefit is the MI 10K DPA, which provides up to $10,000 in assistance. This is structured as a 0% interest loan with no monthly payments, only requiring repayment when you sell or refinance. You can often combine this with other Michigan first-time home buyer programs to maximize your initial lift. Some specific “Zip” codes even offer increased assistance amounts to encourage growth in targeted neighborhoods.

The Renovation Route

If the move-in-ready market feels too crowded, you can engineer your own equity by choosing a renovation mortgage. This specialized tool allows you to purchase a “fixer-upper” and include the costs of repairs and upgrades into a single monthly payment. On a $70,000 salary, this strategy can be highly effective. It allows you to buy a property at a lower initial price point and use the loan to fund the “lift” needed to modernize the home. This process doesn’t just give you a customized living space; it builds immediate net worth through forced appreciation. To see which of these programs fits your current budget best, explore our purchase mortgage options today.

Navigating Your Closing: Why Local Expertise Matters in West Michigan

As you prepare for your final approach to homeownership, the partner you choose for your financing becomes your most critical navigator. While national “big box” lenders might offer sleek apps, they often lack the local coordinates needed for a smooth touchdown in West Michigan. When calculating how much house can I afford on $70k salary in Michigan, a local expert ensures your escrow and property taxes are calculated with precision. This prevents “payment shock” later on, as local professionals understand the specific tax nuances of Kalamazoo and Portage that national algorithms often overlook. We don’t just process a file; we guide you through the specific terrain of our local market.

The approach at Jeremy Drobeck – Treadstone Mortgage is built on personalized navigation from takeoff to touchdown. By verifying your $70,000 income and debt cargo early, we ensure your flight manifest is accurate before you ever tour a home. This level of preparation provides a sense of calm during what can be a high-stress process, replacing anxiety with expert guidance. We remain present throughout the entire duration of the process, acting as a steady ally to ensure your financial transition is handled with care and empathy.

The Local Advantage in a Competitive Market

Listing agents in Kalamazoo and Battle Creek prioritize offers backed by local names they trust. In a market where homes move at a rapid pace, your choice of lender serves as a signal of your offer’s stability. A local mortgage expert provides accountability that a call center cannot match. If the flight path gets bumpy, you have a navigator you can actually call or meet in person. This local connection often provides the necessary lift to get your offer accepted over competitors using generic, national providers. Proactive preparation allows us to avoid common closing delays, ensuring you reach your destination on schedule.

Your Next Steps: Pre-Approval and Beyond

Your journey toward a new home officially begins with gathering your flight documents. You will need your recent W2s, bank statements, and tax returns to verify your $5,833 gross monthly income. It is vital to understand the difference between a simple pre-qualification and a verified pre-approval. A pre-qualification is a preliminary scan based on unverified data. A verified pre-approval is your confirmed clearance to land. It tells sellers that your financing is engineered for success. Ready to secure your clearance? Start your Michigan home-buying journey with Jeremy Drobeck – Treadstone Mortgage today!

- Review your credit score to ensure you have the best fuel for low rates.

- Confirm your MSHDA eligibility to potentially secure $10,000 in assistance.

- Calculate your total debt-to-income ratio to establish your maximum purchase price.

- Obtain a verified pre-approval from a local West Michigan expert.

Chart Your Final Approach to Michigan Homeownership

Securing a home in the current market is less about guessing and more about engineering a precise plan. You now have the instruments to understand how much house can I afford on $70k salary in Michigan, from the 28% housing ratio to the unique tax uncapping rules that define our local landscape. By leveraging tools like MSHDA and choosing the right loan program, you can maximize your lift and land safely in a neighborhood that fits your lifestyle. Whether you are eyeing a historic home in Kalamazoo or a quiet ranch in Battle Creek; the right preparation ensures your budget remains stable long after the moving trucks depart.

Jeremy Drobeck – Treadstone Mortgage has served as a steady ally for Michigan families since 2002, specializing in local assistance programs and personalized navigation. As part of the Division of Neighborhood Loans, Inc. (NMLS #222982), we provide the expert guidance needed to turn a complex financial transaction into a celebrated life milestone. Don’t leave your journey to chance when you can have a seasoned navigator by your side. Get your personalized Michigan Home Affordability Flight Plan from Jeremy Drobeck – Treadstone Mortgage and start your pre-approval process with total confidence. Your new front door is closer than you think.

Frequently Asked Questions

Is $70,000 a good salary to buy a house in Michigan in 2026?

Yes, $70,000 remains a very stable income for the Michigan housing market. With a gross monthly income of $5,833, you have the financial clearance to look at homes in the $210,000 to $290,000 range. This aligns well with the state’s average home value of $263,590. You aren’t priced out; you simply need to navigate the current 6.49% interest rate environment with a precise budget.

Can I get a Michigan home loan with 0% down on a $70k salary?

You can achieve 0% down through specific programs like USDA or VA mortgages. USDA loans are available for properties in designated rural areas, while VA loans serve veterans and active duty members. If you don’t qualify for those, MSHDA down payment assistance provides up to $10,000. This effectively reduces your out of pocket costs to nearly zero for many homes across the state.

How much will my monthly mortgage payment be on a $250k house in Michigan?

Your payment will likely land around $2,000 to $2,200 per month. This estimate includes principal and interest at 6.49%, along with Michigan’s 1.25% effective property tax rate and homeowners insurance. While this might feel like a heavy lift, a local navigator can help you adjust your down payment or debt cargo to ensure the monthly payment remains manageable and safe.

What is the minimum credit score for a mortgage in Michigan with a $70k income?

You typically need a minimum score of 580 for an FHA mortgage or 620 for a Conventional loan. However, MSHDA programs require a 640 for government backed loans and a 660 for Conventional paths. Aiming for a score of 740 or higher provides the best fuel for your flight. Higher scores unlock lower interest rates, which directly increases how much house can I afford on $70k salary in Michigan.

Does the MSHDA program have an income limit for $70,000 earners?

MSHDA does have income limits, but a $70,000 salary is well within the eligible range for most Michigan counties. For 2026, household income limits in areas like Wayne County reach approximately $121,320. This means you are comfortably positioned to qualify for their $10,000 down payment assistance. It is a powerful tool for maintaining your cash reserves while securing a stable home.

How do Michigan property taxes affect how much house I can afford?

Michigan’s property taxes are higher than the national average and can significantly impact your monthly escrow payment. The “pop-up” effect means your taxes will reset based on the new purchase price rather than the previous owner’s rate. We calculate these future costs during your pre-approval process. Proper navigation ensures you don’t stall out when the first tax bill arrives after closing.

Should I pay off my car loan before applying for a mortgage on $70k a year?

Paying off a car loan can significantly increase your available housing “lift” by lowering your debt to income ratio. If your car payment is $400 a month, removing that obligation could potentially allow you to qualify for a higher mortgage amount. However, you shouldn’t drain your down payment savings to do it. We can help you analyze which move provides the smoothest flight path for your goals.

Can I use a renovation loan if I only make $70,000?

You can absolutely use a renovation mortgage on a $70,000 salary to customize a fixer upper. This program combines the purchase price and the cost of repairs into one single monthly payment. It is an excellent strategy for buyers who want to build equity quickly in competitive West Michigan markets. We help you engineer the loan so your total payment remains within your affordable clearance.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”