MSHDA Down Payment Assistance: Your 2026 Michigan Homeownership Flight Plan

Imagine standing on the edge of the runway in Kalamazoo, watching neighbors take flight into their new homes while you stay grounded by a $10,000 shortfall in your savings. It’s a common frustration in May 2026. The desire to own a home in Portage or St. Joseph is high, but the upfront cash requirements often feel like a heavy headwind. You’re likely tired of the confusion surrounding different programs and the anxiety of navigating complex government paperwork. We understand that the hidden details of a mortgage can feel like flying through thick fog without a GPS.

This article will show you how MSHDA Down Payment Assistance acts as the extra lift your flaps need to get airborne. We’ll master the requirements for the MI 10K DPA program, which offers a 0% interest, non-amortizing loan to cover those initial costs. You’ll learn exactly how to qualify with a 640 credit score and navigate the application steps to clear your flight path. We are going to map out the entire journey from initial homebuyer education to the final closing signature so you can move into your Michigan home with total confidence.

Key Takeaways

- Discover how MSHDA Down Payment Assistance acts like a plane’s flaps, providing the extra lift needed to clear the runway when your savings are low.

- Compare the MI 10K DPA program with other specialized options to ensure you’re choosing the right aircraft for your long-term financial goals.

- Master the essential credit score and debt-to-income requirements to pass your pre-flight inspection with confidence.

- Identify the specific 2026 income limits and targeted zip codes in Kalamazoo and Portage that determine your eligibility for maximum assistance.

- Learn the exact steps to transition from your initial consultation to a full pre-approval so you can start shopping with total clearance.

What is MSHDA Down Payment Assistance? Gaining Extra Lift

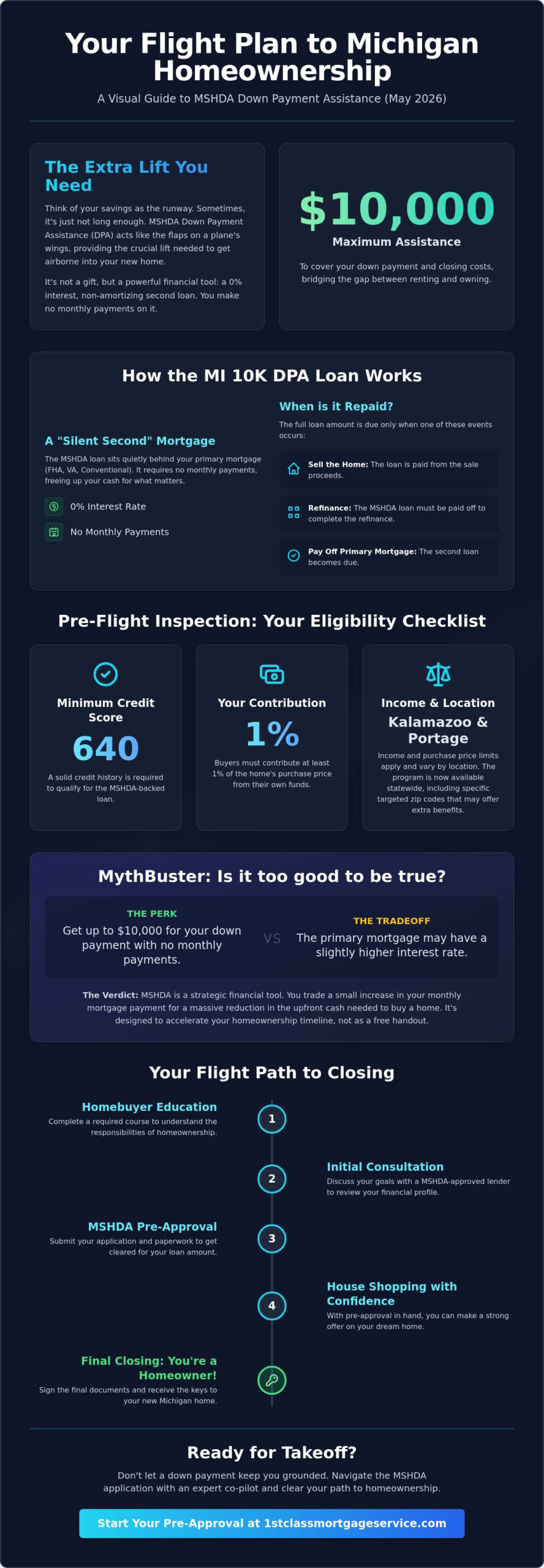

Getting a heavy aircraft off the ground requires more than just raw engine power; it requires the right configuration of the wings. In the mortgage world, your income and credit act as the engines, but your cash savings are often the weight holding you back. This is where MSHDA Down Payment Assistance comes in. Established by the Michigan State Housing Development Authority (MSHDA), this program acts as the “flaps” on your wings. It provides that essential extra lift by offering up to $10,000 to cover your down payment and closing costs. In May 2026, this assistance is more vital than ever as the program has expanded statewide, now accounting for more than 70% of all down payment assistance applications in Michigan.

This isn’t a gift, but it’s the next best thing for a prepared buyer. It’s a 0% interest, non-amortizing second mortgage. You don’t make monthly payments on this $10,000. Instead, the loan sits quietly in the background while you build equity in your home. You only settle the balance when you sell the property, pay off the primary mortgage, or choose to refinance. This structure allows you to keep your liquidity for home maintenance or emergencies rather than draining your bank account at the closing table. It’s a controlled, engineered way to bridge the gap between renting and owning.

How MSHDA Integrates with Your Primary Mortgage

Your home purchase flight plan usually begins with a primary loan. MSHDA assistance is designed to integrate seamlessly as a “silent second” behind standard financing options. Whether you are looking at Conventional, VA, or FHA loans in Michigan, this program fills the gap. However, you can’t fly entirely for free. The program requires a minimum contribution of 1% of the purchase price from your own funds. This small “skin in the game” ensures that every pilot is committed to the journey while MSHDA Down Payment Assistance handles the bulk of the heavy lifting. We’re here every step of the way to ensure these two loans work in perfect harmony.

The “Too Good to Be True” Myth-Busting

Skepticism is natural when someone offers you $10,000 with no monthly payments. You might wonder why the State of Michigan would do this. The answer is simple. Stable homeownership builds stronger communities in places like Kalamazoo and Portage, which benefits the state’s economy. There is a small tradeoff to consider. Loans paired with MSHDA assistance sometimes carry a slightly higher interest rate than a standard standalone loan. You are essentially trading a small amount of monthly payment for a massive reduction in your initial cash-to-close. MSHDA Down Payment Assistance is a strategic financial tool designed to accelerate your timeline, not a government handout for the unprepared. If you’re exploring every option to minimize your upfront costs, you may also want to learn about a zero down payment home loan and 100% financing options available in Michigan.

Choosing Your Aircraft: MI 10K DPA vs. First-Generation DPA

Every successful mission begins by selecting the right aircraft for the job. When you’re preparing for homeownership, you have two primary “models” of MSHDA Down Payment Assistance to consider. The first is the MI 10K DPA, which is the reliable workhorse of the Michigan housing market. The second is the First-Generation DPA, a specialized program designed for those who need a more powerful engine to clear significant financial obstacles. Your flight path will change based on which program fits your background, and understanding the specs of each is the best way to avoid turbulence during the application process.

The choice between these programs isn’t just about the dollar amount. It involves looking at your family history, your credit profile, and your long-term destination. While both programs provide the lift needed to reach a closing date, they have different fuel requirements and flight ceilings. We are here to help you weigh these options so you don’t feel like you’re flying solo through a storm of paperwork.

MI 10K DPA: The Standard Flight Path

The MI 10K DPA is the most common route for Michigan buyers. It is now available statewide, a major expansion from the previous limits that only covered 236 zip codes. This program provides up to $10,000 in assistance and is available to both first-time and repeat buyers if the home is located in a “targeted” area. For those looking in Kalamazoo or Portage, you’ll need to navigate specific income and purchase price limits. As of May 1, 2024, eligible income limits for MSHDA programs ranged from $91,200 to $174,720 depending on household size and location. You must also complete a MSHDA-approved homebuyer education course to ensure you’re fully prepared for the responsibilities of being a pilot of your own home. If you’re ready to see how these numbers apply to your situation, request a mortgage consultation to start your pre-flight check.

First-Generation DPA: Clearing Higher Obstacles

The First-Generation DPA program was designed as a high-altitude solution, historically offering up to $25,000 in assistance. To qualify for this specific flight plan, you must meet the definition of a “first-generation” homebuyer. This means your parents or legal guardians have never owned a home, or they lost their home to foreclosure and do not currently own one. While the initial round of funding for this grant was depleted in May 2025, it remains a vital program to monitor for 2026 renewals. This program is a major catalyst for building generational wealth, especially in areas like Battle Creek or specific zip codes in Kalamazoo. It provides the extra thrust needed for families who don’t have a history of homeownership to lean on for support.

The Pre-Flight Inspection: Your MSHDA Eligibility Checklist

Every pilot knows that the most critical part of a flight happens before the engines even start. A pre-flight inspection ensures the aircraft is mechanically sound and the flight plan is viable. When you apply for MSHDA Down Payment Assistance, the eligibility checklist serves as that final walk-around. We look at your credit score, your debt-to-income (DTI) ratio, and your household income to ensure you have the clearance needed for a safe ascent. Skipping these checks can lead to turbulence later in the underwriting process, so we handle this phase with precision and care.

Your credit score is your flight ceiling. To qualify for a stick-built home in Michigan, you need a minimum score of 640. If you are looking at a manufactured home, that ceiling rises to 660. Beyond the score, we must balance your financial weight. Your DTI ratio measures your monthly debt against your gross income. Keeping this ratio in check ensures you have enough fuel to handle your mortgage payments without stalling your budget. If your financial weight is too high, it might prevent you from getting airborne, but we’re here every step of the way to help you adjust your cargo.

MSHDA has specific rules about who counts toward your income limits. They calculate “household income,” which includes the earnings of everyone 18 and older living in the home, not just the “borrower income” listed on the loan application. As of May 1, 2024, these limits ranged from $91,200 to $174,720 depending on your county and household size. There are also asset limits to consider. This program is designed for those who truly need the lift, so having excessive cash on hand can sometimes disqualify you from receiving the full $10,000 in assistance.

Essential Documentation for Your Co-Pilot

Gathering your paperwork is like filing your flight plan with the tower. You’ll need the “Big Three”: two years of tax returns, 30 days of paystubs, and two months of bank statements. If you are applying for a “targeted area” in Kalamazoo or Portage, you may need additional proof of residency or first-time homebuyer status. Straight talk about your finances now prevents a crash during the final stages of underwriting. We prefer to identify potential issues while we’re still on the tarmac rather than at 30,000 feet.

Home Requirements: The Landing Strip

Even with a perfect credit score, the home itself must meet certain specs to serve as your landing strip. For 2026, the statewide home purchase price limit is $224,500. The property must be your primary residence; investment properties and second homes are grounded immediately. Eligible property types include single-family homes, approved condos, and multi-section manufactured homes. The property must not exceed two acres, though some exceptions allow for up to five acres in specific Michigan rural zones.

Navigating Local Airspace: MSHDA in Kalamazoo and Portage

Every flight region has its own unique weather patterns and air traffic control protocols. Flying into the West Michigan housing market is no different. While the MSHDA Down Payment Assistance program is available statewide, the way it applies to a home in Kalamazoo County versus a property in neighboring St. Joseph or Calhoun County can vary. For 2026, the statewide home purchase price limit is $224,500. Staying within this flight ceiling is essential for eligibility. We also monitor the local income limits closely. As of May 1, 2024, these limits ranged from $91,200 to $174,720 based on your household size. Knowing these numbers before you start shopping prevents you from heading toward a destination you can’t legally land in.

The Kalamazoo real estate market moves fast. Using DPA isn’t just about saving money; it’s a competitive maneuver. By securing $10,000 in assistance, you can keep your personal savings as “emergency fuel” for home repairs or unexpected costs after closing. In a market where multiple offers are common, having your financing locked in with a local co-pilot who understands these specific Michigan regulations gives you a significant advantage. We’re here every step of the way to ensure your offer is viewed as a “1st Class” ticket by sellers in Portage and beyond.

Targeted Areas in West Michigan

One of the most powerful “shortcuts” in the MSHDA flight plan is the Targeted Area designation. In certain census tracts within Kalamazoo and Battle Creek, the state waives the requirement that you must be a first-time homebuyer. This means repeat buyers can access MSHDA Down Payment Assistance to get back into a home if they choose a property in these specific zip codes. It’s an excellent way to bypass standard eligibility rules and accelerate your return to homeownership. You can explore more about these opportunities in our Michigan First Time Home Buyer Programs pillar.

The 1% Contribution in Local Dollars

Even with $10,000 in assistance, you still need a small amount of “skin in the game.” MSHDA requires a 1% contribution from the buyer. If you are purchasing a $200,000 home in Portage, your required contribution would be $2,000. When you compare this to the standard down payment requirements in Kalamazoo, which can often reach 3.5% or 5%, the savings are massive. For buyers who want to eliminate their upfront costs entirely, pairing MSHDA with a zero down payment home loan through USDA or VA financing may be worth exploring as a complementary strategy. This allows you to achieve lift-off with much less cash out of pocket, preserving your liquidity for the journey ahead. If you’re ready to see if your favorite neighborhood qualifies, contact our team for a custom flight plan.

Ready for Takeoff: How to Apply for MSHDA with Jeremy Drobeck

Your flight plan is finalized, the pre-flight inspection is complete, and the runway is clear for your ascent. Now comes the most rewarding part of the journey: the actual application process. Applying for MSHDA Down Payment Assistance doesn’t have to be a high-stress maneuver that leaves you circling the airport. While the state paperwork can be dense, having an experienced team ensures you don’t get lost in the clouds. We’ve engineered a step-by-step process that takes you from the initial dream of homeownership to the final landing at the closing table in Kalamazoo or Portage.

- Step 1: The Initial Consultation. We start by charting your course. During this meeting, we review your specific goals and verify that your financial profile aligns with the 2026 state requirements. This is where we determine if the MI 10K DPA or another program is the most efficient fuel for your journey.

- Step 2: Pre-Approval. Think of this as getting your clearance from the tower. We provide a formal pre-approval letter, which signals to sellers and realtors that your financing is solid and backed by a reliable lender. In a fast-moving market like Battle Creek, this letter is your ticket to being taken seriously.

- Step 3: The Home Search. With your clearance in hand, you can shop for a property that fits the MSHDA landing strip. Your agent will help you find a home that meets the primary residence requirements while we stay in constant communication to ensure the property specs remain within the program’s guidelines.

- Step 4: Underwriting and Closing. This is where your team handles the heavy lifting. We manage the back-end coordination with state officials and process the specific documents required for the $10,000 assistance. We keep you informed at every waypoint until you reach the final destination.

Why Choose a “1st Class” MSHDA Lender?

The State of Michigan provides a long list of approved lenders, but not all flight crews offer the same level of precision. Many large, national banks treat MSHDA Down Payment Assistance as a secondary task, which often leads to delays or missed deadlines. We take a different approach. Choosing Jeremy Drobeck – Treadstone Mortgage means you’re getting a partner who prioritizes personal attention and respect. We understand that your home purchase is a major life milestone, not just another loan file in a stack. We specialize in handling outside of the box scenarios, helping buyers who might have been grounded by other lenders due to complex income structures. We’re here every step of the way to ensure your GPS stays on track.

Your Next Steps to Homeownership

The horizon is waiting, and the first step is simpler than you might think. You don’t need to have every detail of the mortgage industry mastered today; that’s what your co-pilot is for. You can start the application process online in under 10 minutes, or simply call our office to discuss your goals. We’ll help you determine if MSHDA is the right lift for your specific situation and help you secure the funds you need to move forward. Call today for a mortgage consultation to see if we can clear you for takeoff. Contact Jeremy Drobeck – Treadstone Mortgage to begin your journey toward homeownership.

Clear the Runway for Your New Michigan Home

Your path to owning a home in West Michigan is now mapped out and ready for execution. We’ve reviewed how the right configuration of financial tools can overcome the headwind of high upfront costs. By utilizing MSHDA Down Payment Assistance, you can effectively bridge the gap between your current savings and the requirements of the 2026 housing market. The goal is to move from the tarmac of renting to the clear skies of homeownership without draining your emergency reserves or delaying your dreams any longer.

With over 20 years of local mortgage expertise, Jeremy Drobeck – Treadstone Mortgage provides the specialized guidance needed for MSHDA, FHA, and renovation lending. Our seasoned co-pilot service model ensures that you receive the personal attention and respect required for such a significant life milestone. We’re here every step of the way to navigate the complexities of state funding on your behalf. Schedule Your 2026 MSHDA Flight Plan Consultation with Jeremy Drobeck – Treadstone Mortgage today. Your new front door is within reach, and we’re ready to help you achieve a smooth landing.

Frequently Asked Questions

Do I ever have to pay back the MSHDA down payment assistance?

Yes, you must repay the funds when you sell your home, pay off your primary mortgage, or choose to refinance. This assistance is a 0% interest, non-amortizing second mortgage with no monthly payments required. It sits quietly on your flight recorder until one of those specific events triggers the repayment of the balance.

Can I use MSHDA assistance with a VA loan if I am a veteran?

Yes, MSHDA Down Payment Assistance can be used in conjunction with VA, FHA, USDA, or Conventional loans. This flexibility allows veterans to leverage their earned benefits while gaining the extra lift of state-backed funds. We’ll help you coordinate both programs to ensure your entry into homeownership is as smooth as possible.

What is the minimum credit score for MSHDA in 2026?

The minimum credit score required is 640 for stick-built homes and 660 for manufactured homes as of May 2026. These scores act as your flight ceiling; meeting them ensures your financial engines are strong enough for takeoff. If your score is slightly lower, we can discuss a plan to help you get airborne in the future.

Is MSHDA only for first-time homebuyers in Michigan?

No, the program is open to repeat buyers if they purchase a home in a designated “Targeted Area.” While standard rules focus on first-time buyers, these specific zip codes in Kalamazoo and Battle Creek offer a shortcut. We can check the local radar to see if your preferred neighborhood allows you to bypass the first-time buyer requirement.

How long does the MSHDA approval process take compared to a standard loan?

The approval process typically adds about 3 to 5 business days to a standard mortgage timeline. Because it involves state-level paperwork, it requires a co-pilot who knows the specific protocols to avoid delays. We manage the extra documentation behind the scenes so your closing stays on schedule and doesn’t get stuck on the tarmac.

Can I use MSHDA to buy a fixer-upper or renovation property?

Yes, you can combine MSHDA Down Payment Assistance with a renovation mortgage to purchase and repair a home. This is an excellent strategy for buyers looking to build equity in older neighborhoods in Portage or St. Joseph. It provides the cash lift needed for the down payment while the primary loan covers the cost of improvements.

Are there income limits for MSHDA in Kalamazoo County?

Yes, income limits are based on your total household size and the specific county where you are buying. As of May 1, 2024, these limits ranged from $91,200 to $174,720 for Michigan residents. We must include the income of all adults living in the home to ensure your flight plan stays within the state’s legal limits.

What happens to the DPA if I refinance my home later?

You must pay back the full amount of the assistance if you refinance your primary mortgage. Since the loan has no interest, you simply settle the original amount, such as the $10,000 provided by the MI 10K DPA program. This is usually handled using the equity you’ve built in the home before you start your next financial flight path.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”