Conventional vs. FHA Loan in Michigan: Your 2026 Navigation Guide

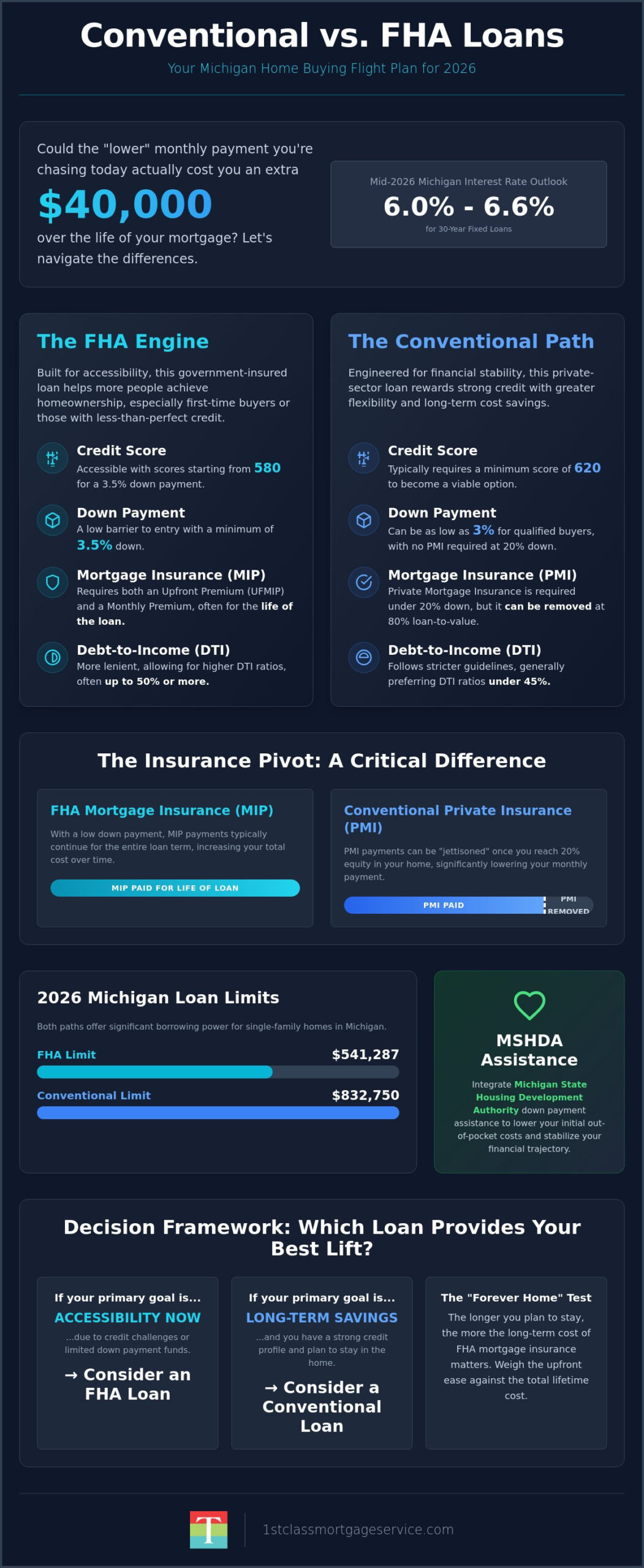

What if the lower monthly payment you’re chasing today actually costs you $40,000 more over the life of your mortgage? When you’re weighing a Conventional vs FHA loan Michigan homeowners often feel like they’re choosing between two different flight paths without a clear radar. It’s a high-stakes decision, especially with interest rates for 30-year fixed loans hovering between 6% and 6.6% in mid-2026. You want the security of a stable home without the turbulence of hidden costs or rigid insurance rules.

I understand that the technical jargon of UFMIP and PMI can make the process feel like a gamble rather than a controlled, engineered plan. This guide is your navigation manual to master the mechanical differences and local advantages of both paths. We’ll compare upfront costs against long-term savings, explain how MSHDA down payment assistance fits into your strategy, and give you the confidence to choose the financial engine that delivers the most lift for your specific credit score and Michigan zip code.

Key Takeaways

- Learn the technical mechanics of a Conventional vs FHA loan Michigan to determine which mortgage engine provides the most efficient lift for your credit score and down payment goals.

- Compare the minimum fuel required for takeoff, including the 3.5% down payment barrier for FHA and the specific credit benchmarks that trigger a more streamlined Conventional path.

- Master the insurance pivot by understanding how to eventually jettison Conventional PMI at 80% equity, compared to the life-of-loan commitment often required by FHA engines.

- Discover how to integrate MSHDA Down Payment Assistance into your flight plan to lower your initial out-of-pocket costs and stabilize your long-term financial trajectory.

- Apply the “Forever Home” test to decide if the upfront accessibility of an FHA loan or the long-term cost-efficiency of a Conventional mortgage is the right vehicle for your Michigan home.

FHA vs. Conventional Mortgages: Mapping Your Michigan Flight Path

The 2026 Michigan housing market requires more than just a pre-approval letter; it demands a tactical strategy. Whether you’re eyeing a bungalow in Kalamazoo or a family home in Portage, the decision between a Conventional vs FHA loan Michigan acts as the primary engine for your purchase. I don’t see these as generic products. Instead, I view them as customized flight paths designed to match your specific financial altitude. Choosing the wrong one can lead to unnecessary turbulence in the form of higher fees or rejected offers in a competitive bidding war. Your loan choice determines your monthly overhead, your upfront cash requirements, and how quickly you build equity in your Michigan home.

The FHA Engine: Built for Accessibility

The Federal Housing Administration doesn’t actually lend you the money. Instead, an FHA insured loan provides a safety net for the lender. This government backing acts like a stabilizer, allowing us to offer mortgages to borrowers who might have a few bumps in their credit history or less cash for a down payment. In our local communities like Kalamazoo and Portage, this accessibility has helped thousands of families achieve lift-off when traditional private-sector routes were closed. It’s an engine built for inclusivity. Because the government reduces the lender’s risk, we can accept lower credit scores and higher debt ratios. This makes the FHA path a reliable vehicle for first-time buyers or those recovering from past financial setbacks.

The Conventional Path: Conforming to Stability

Conventional loans follow a different mechanical logic. These are private-sector paths that “conform” to rules set by Fannie Mae and Freddie Mac. While they often require higher credit scores to clear the runway, they reward that stability with more flexibility. If you’ve saved a 20% down payment, a Conventional loan allows you to fly without any mortgage insurance at all. Even with a smaller down payment, the private mortgage insurance (PMI) on a Conventional loan can eventually be jettisoned once you reach 80% equity. This is a sharp contrast to the permanent insurance premiums often found in the FHA hangar. For borrowers with strong credit, the Conventional vs FHA loan Michigan comparison often favors the Conventional path due to its long-term cost efficiency and streamlined closing process.

I believe in a “Navigator” approach to lending. My goal isn’t just to sell you a mortgage; it’s to help you engineer a plan that fits your life. We look at your five-year and ten-year goals to see which loan provides the best lift. Sometimes the accessible FHA engine is perfect for getting you into the market today. Other times, waiting to polish your credit for a Conventional path is the smarter play for your long-term wealth.

Mechanical Comparison: Credit, Down Payments, and Debt-to-Income

Every successful flight requires a specific fuel load and a carefully calculated weight limit. When you’re comparing a Conventional vs FHA loan Michigan borrowers often assume FHA is the only option for low down payments. That’s a common misconception in 2026. While FHA loans allow for a higher “payload” in your Debt-to-Income (DTI) ratio, often pushing toward 50% or more, Conventional paths have become remarkably agile. The 2026 economic climate in West Michigan has created a unique environment where the technical specs of your credit and cash reserves matter more than ever. Understanding these mechanics helps you avoid being grounded before you even reach the closing table.

The 2026 loan limits also play a role in your planning. With FHA limits at $541,287 and Conventional conforming limits reaching $832,750 for single-family homes in Michigan, both paths offer plenty of room for most local properties. However, the higher your DTI, the more you might need the FHA engine to stabilize your application. We look at your total monthly obligations to ensure your mortgage doesn’t become a heavy anchor on your financial freedom.

Credit Score Nuances in 2026

Your credit score acts as your visibility on the financial radar. A score of 620 remains the traditional pivot point where the Conventional path becomes a viable option. If your score is currently sitting at 580, the FHA engine is usually your primary vehicle for a 3.5% down payment. You can find a detailed breakdown from the Consumer Financial Protection Bureau on FHA Loans regarding how these credit benchmarks affect your eligibility. I specialize in helping families navigate this “turbulence” months before they apply. Sometimes, a few strategic moves to polish your credit can shift you from an FHA entry to a more cost-effective Conventional altitude, which significantly lowers your interest rate over the life of the loan.

Down Payment Realities for Michigan Buyers

It’s time to debunk the 20% down payment myth once and for all. In 2026, many Conventional programs allow for just 3% down, which is actually less initial “fuel” than the 3.5% required by FHA. However, the choice involves more than just the percentage. FHA is typically more lenient when it comes to using gift funds from family members to cover your costs. If your parents are contributing to your purchase in Kalamazoo or Portage, the FHA documentation process is often less restrictive than the Conventional route. The amount you put down directly impacts your monthly burn rate and long-term equity. If you’re trying to decide which path fits your budget, you can explore your purchase mortgage options to see which engine delivers the best performance for your specific scenario.

- FHA: Requires a 3.5% minimum down payment with a 580+ credit score.

- Conventional: Offers a 3% minimum down payment for qualified first-time buyers with a 620+ score.

- DTI Limits: FHA permits a higher debt-to-income ratio, allowing you to carry more monthly “weight” than most Conventional loans.

The Insurance Pivot: MIP vs. PMI and the Kalamazoo Factor

Every pilot knows that drag can slow your momentum and increase your fuel consumption. In the world of home finance, mortgage insurance is that drag. It’s a necessary component for many takeoffs, but how you manage it determines the efficiency of your long-term flight. When comparing a Conventional vs FHA loan Michigan families often focus solely on the interest rate. However, the insurance pivot, the point where you either keep or jettison your mortgage insurance, is where the real savings are engineered. Choosing between FHA’s Mortgage Insurance Premium (MIP) and Conventional’s Private Mortgage Insurance (PMI) requires a clear look at your five-year radar.

The 2026 market in West Michigan has shown steady appreciation, which makes the insurance conversation even more critical. You can find excellent resources for managing these costs in the CFPB Mortgage Guide, which outlines how to shop for the best overall loan structure. My role is to help you decide which insurance model provides the most lift for your specific budget without weighing down your future equity.

FHA MIP: The Cost of the Safety Net

FHA loans require a two-layered insurance approach. First, there’s an upfront premium, usually 1.75% of the loan amount, which most Michigan buyers choose to finance into their total balance. Second, you’ll pay an annual monthly fee. If you start your journey with a down payment of less than 10%, that monthly MIP is a life-of-loan commitment. It doesn’t drop off automatically as you pay down the balance. While this might sound like a heavy load, FHA MIP is often the more affordable monthly option for borrowers with credit scores below 700. It provides a stable, predictable cost that doesn’t fluctuate wildly based on small credit score changes.

Conventional PMI: The Path to Lower Monthly Costs

Conventional PMI operates on a different mechanical logic. The cost is highly sensitive to your credit score and down payment amount. If you have a high credit score, your monthly PMI might be significantly lower than an FHA premium. The biggest advantage of the Conventional path is the ability to eventually jettison the insurance altogether. Once your loan-to-value ratio reaches 80%, you can request to have the PMI removed. This instantly lowers your monthly burn rate and increases your cash flow.

This is where we apply the “Kalamazoo Factor.” In vibrant markets like Kalamazoo and Portage, home values have historically trended upward. You don’t just reach that 80% equity mark through monthly payments; you can reach it through local market appreciation. If your home’s value increases, you can often order a new appraisal to prove you’ve hit the equity target and cancel your PMI years ahead of schedule. When weighing a Conventional vs FHA loan Michigan, this ability to cancel insurance based on local growth is a powerful argument for the Conventional path. It rewards homeowners who plan to stay in their property long enough to benefit from our region’s steady economic climb.

- Upfront Costs: FHA requires a 1.75% upfront premium; Conventional typically does not.

- Monthly Impact: FHA MIP is often cheaper for lower credit; Conventional PMI is cheaper for higher credit.

- Cancellation: Conventional PMI can be cancelled at 80% equity; FHA MIP usually stays for the life of the loan.

Strategic Navigation: Integrating MSHDA and Local Assistance

Choosing between a Conventional vs FHA loan Michigan is rarely a solo flight. For many Michigan families, the journey requires a secondary power source to clear the financial runway. This is where state-specific programs like MSHDA Down Payment Assistance act as a booster, providing up to $10,000 in support. These programs don’t interact with every loan engine in the same way. Coordinating these tools requires precise navigation to ensure your local grants and seller concessions, especially in markets like Battle Creek, align with your primary mortgage structure. My role is to help you synchronize these mechanical components so they work in harmony rather than causing drag on your application.

The MSHDA Bridge

The MSHDA MI Home Loan program is a versatile tool that can be paired with both loan types, but the eligibility mechanics vary. For a Conventional 97% loan, MSHDA provides the necessary lift for borrowers who have strong credit but limited cash reserves. Conversely, MSHDA can also cover the entire 3.5% down payment required for an FHA loan in Michigan. This combination is particularly effective for first-time buyers in 2026 because it lowers the initial barrier to entry to nearly zero. You’ll need a minimum credit score of 640 to access this bridge, and I’ll be there to help you verify that your household income fits within the county-specific limits.

Appraisal Standards: FHA vs. Conventional

The condition of your target property often dictates which flight path is even possible. FHA appraisals are designed with a “safety first” mentality. They include stricter inspections for habitability issues like peeling lead-based paint, missing handrails, or outdated electrical systems. If you’re falling in love with a historic Kalamazoo home that needs some mechanical updates, the FHA path might require repairs before you can close. Conventional appraisals focus more on the market value and general stability of the structure. If a property doesn’t meet FHA’s rigorous safety check, we might pivot to a Conventional path or look at renovation options to ensure your home is a safe long-term investment. If you want to see which assistance programs match your target neighborhood, you can check your MSHDA eligibility and start building your custom flight plan today.

- MSHDA Compatibility: Works with both paths but requires a 640 minimum credit score.

- Seller Concessions: FHA allows sellers to contribute up to 6% of the price; Conventional typically limits this to 3% for low down payment loans.

- Property Condition: FHA is more restrictive regarding minor safety repairs than Conventional.

Matching your loan type to local incentives in Battle Creek or Kalamazoo requires a deep understanding of the regional landscape. We don’t just look at the numbers on a spreadsheet. We look at the specific house, the specific city grants, and your specific financial goals to engineer the most stable path forward.

Decision Framework: Which Loan Provides Your Best Lift?

Choosing between a Conventional vs FHA loan Michigan comes down to your intended flight duration. If you’re looking for a “Forever Home” where you’ll stay for a decade or more, the Conventional path often provides the best long-term lift. The ability to eventually remove mortgage insurance creates a more efficient financial engine over time. However, if you’re executing a “Starter Home” strategy, the FHA engine allows you to enter the market sooner with less initial capital. This gets you into a home today so you can begin building equity, even if you plan to refinance into a different vehicle later. You can find more detailed tactical advice in this Purchase Mortgage guide.

I recommend a rigorous “Stress Test” for every 2026 flight plan. We look at how interest rate fluctuations or changes in your monthly payload might affect your stability. It’s about ensuring your mortgage remains a source of security, not a point of failure. By comparing the total cost of each path over five, ten, and fifteen years, we can identify which loan type offers the most stable trajectory for your household. This isn’t just about the lowest rate; it’s about the highest level of financial safety.

Expert Guidance with Jeremy Drobeck

Most big banks treat lending as a cold, transactional experience. I view it as a partnership. At Treadstone Mortgage, we move beyond the standard application process to provide personalized navigation. We analyze your income, assets, and your specific 2026 goals to find the right fit. Every Michigan homebuyer has a unique financial signature. I take the time to understand yours so we can engineer a plan that fits your life. My commitment is to be your ally from the first pre-approval conversation until the moment you receive your keys at the closing table. You deserve a navigator who values preparation and precision as much as you do.

Your Pre-Flight Checklist

Before you clear for takeoff, you’ll need to organize your flight logs. This includes your recent pay stubs, tax returns, and bank statements. Having these documents ready ensures a smooth transition from application to approval without unnecessary delays. You should also benchmark your options against current mortgage rates in Kalamazoo to see how today’s environment impacts your monthly budget. The 2026 market moves fast. Being prepared allows you to act with confidence when you find the perfect property. Ready to start your journey? Contact Jeremy Drobeck today and let’s map out your path to homeownership.

- The Long-Term View: Use Conventional if you plan to build equity and cancel insurance.

- The Entry View: Use FHA if you need lower credit requirements and flexible down payment options.

- The Strategy: Always run a budget stress test against 2026 rate fluctuations.

Ready for Takeoff: Finalizing Your Michigan Home Strategy

Your journey toward homeownership doesn’t have to be a solo flight through heavy fog. Whether you choose the accessible engine of an FHA loan or the long-term streamlined path of a Conventional mortgage, your success depends on a precisely engineered plan. We’ve explored how credit benchmarks and insurance rules dictate your trajectory, but the most important variable is having a seasoned navigator by your side. Deciding between a Conventional vs FHA loan Michigan is just the first step in a larger mission to build lasting stability for your family.

Since 2002, I’ve provided local Kalamazoo expertise to help families navigate the complexities of MSHDA programs and first-time buyer incentives. My team at Treadstone Mortgage offers direct access to FHA, Conventional, and Renovation loan engines, ensuring you have the right mechanical components for your specific goals. Don’t leave your financial future to chance or a generic online calculator. You can Schedule Your Mortgage Flight Plan Consultation with Jeremy Drobeck today to secure your path. I’m here to provide the expert guidance and neighborly support you need until you’re safely cleared for closing.

Frequently Asked Questions

Is it harder to get an FHA loan than a conventional loan in Michigan?

It is actually often easier to qualify for an FHA loan because the government-backed engine is designed for higher accessibility. While Conventional loans require a more pristine credit history and lower debt ratios, FHA guidelines provide a safety net for borrowers with a 580 score or higher. This makes FHA a reliable vehicle for those who might find the Conventional path too restrictive for their current financial altitude.

Can I use MSHDA assistance with a conventional mortgage?

You can absolutely integrate MSHDA assistance with a Conventional mortgage. This combination is often used with 97% Conventional programs to cover the initial 3% down payment requirement. It provides a powerful boost for borrowers with strong credit who want to avoid the life-of-loan insurance premiums associated with FHA while still preserving their upfront cash reserves for home improvements or emergencies.

Why do sellers in Kalamazoo sometimes prefer conventional offers over FHA?

Sellers sometimes prefer Conventional offers because the appraisal process is generally less rigorous regarding minor property repairs. FHA appraisals include stricter safety checks, such as inspections for peeling paint or handrail stability, which can lead to repair requests before closing. In a competitive market like Kalamazoo, a Conventional offer often signals a smoother flight path with fewer mechanical hurdles during the inspection phase.

How much higher are FHA interest rates compared to conventional in 2026?

In July 2026, FHA interest rates are frequently lower than Conventional rates, often ranging between 6.000% and 6.500%. While the base rate for an FHA loan might look more attractive on your radar, the mandatory mortgage insurance premiums can increase your total monthly burn rate. When comparing a Conventional vs FHA loan Michigan, we must look at the all-in cost rather than just the initial interest rate altitude.

Does FHA mortgage insurance ever go away automatically?

FHA mortgage insurance typically remains for the entire life of the loan if you start with a down payment of less than 10%. Unlike Conventional PMI, which you can jettison once you reach 20% equity, FHA premiums are a permanent part of the engine’s operation. To remove this cost, most Michigan homeowners eventually choose to navigate a refinance into a Conventional loan once their home’s value has increased sufficiently.

What is the minimum credit score for a conventional loan in Michigan?

The standard minimum credit score for a Conventional loan in Michigan is 620. While some specialized programs might offer slight flexibility, clearing this 620 benchmark is essential for a stable takeoff on the Conventional path. Borrowers with scores above 720 typically receive the most favorable interest rates and lower monthly insurance costs, making credit polishing a vital part of your pre-flight preparation.

Can I switch from an FHA loan to a conventional loan later through refinancing?

Switching from an FHA loan to a Conventional loan through a refinance is a very common strategy for building long-term wealth. Many homeowners use the FHA path to enter the market with 3.5% down and then pivot to a Conventional loan once they’ve reached 20% equity through payments or local appreciation. This maneuver allows you to cancel monthly insurance premiums and streamline your financial engine for the long haul.

Are there specific income limits for FHA or conventional loans in Portage?

Standard FHA and Conventional loans don’t have strict income limits, but specialized programs and assistance tools do. If you’re using MSHDA or a Conventional path in Portage, your household income must fall below specific county benchmarks. These limits ensure that assistance is directed toward borrowers who need the most lift, and I can help you verify your eligibility based on the latest 2026 data.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”