MSHDA Mortgage Lender in Battle Creek: Your 2026 Homeownership Flight Plan

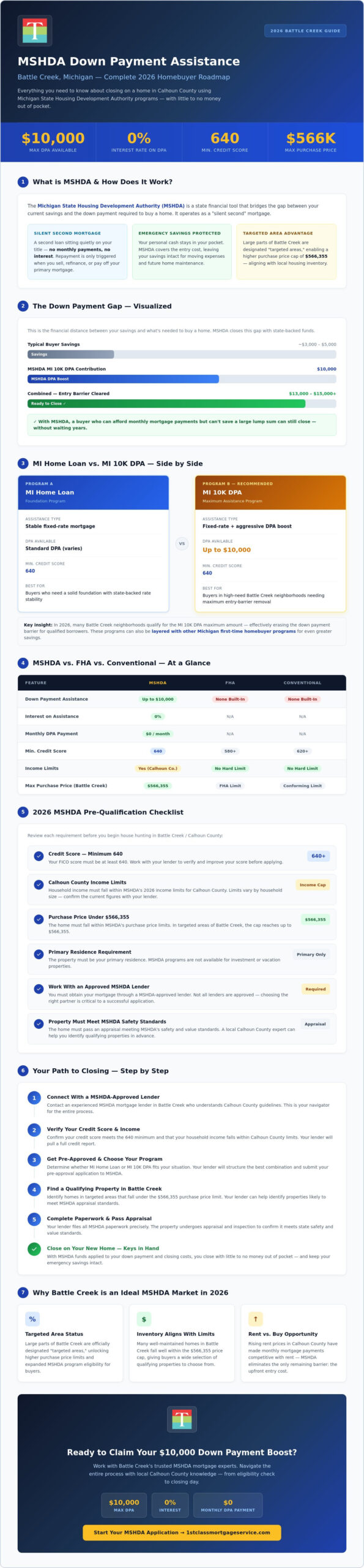

In the 2026 Battle Creek real estate market, the dream of homeownership isn’t grounded by a lack of ambition, but often by the weight of a traditional down payment. You might think you need tens of thousands of dollars in the bank to clear the runway, but that’s a misconception holding too many qualified buyers back. Finding a specialized MSHDA mortgage lender Battle Creek families trust is the first step in fueling your flight toward a new front door. With the MI 10K DPA program now offering up to $10,000 in assistance at 0% interest, the financial lift you need is more accessible than ever.

It’s exhausting to feel like you’re stuck in a holding pattern because of confusing jargon or income limits that seem to change by the day. We understand that the mortgage process can feel like navigating through a storm without a radar. This guide will show you exactly how to secure MSHDA down payment assistance in Battle Creek with the precision of a top-ranked Michigan lender. We’ll break down the latest 2026 eligibility requirements and the specific steps required to close on your home with little to no money out of pocket.

Key Takeaways

- Understand how the MI 10K DPA program provides a $10,000 financial booster to overcome high down payment requirements in Battle Creek.

- Discover why choosing an experienced MSHDA mortgage lender Battle Creek residents trust is essential for navigating complex government guidelines and paperwork.

- Compare MSHDA programs against standard FHA and Conventional loans to determine which flight path offers the most stability for your specific budget.

- Review the 2026 credit score and Calhoun County income limits to ensure your financial profile is cleared for takeoff before you begin house hunting.

- Learn how local guidance from a top-ranked navigator like Jeremy Drobeck provides the end-to-end support needed to reach a successful closing with confidence.

Navigating the Down Payment Barrier in Battle Creek (2026)

The hardest part of any flight isn’t the cruise at thirty thousand feet; it’s the initial lift required to get off the ground. For many families in Calhoun County, that lift is often stalled by the massive upfront cost of a down payment. This is where the Michigan State Housing Development Authority (MSHDA) functions as your primary assistance engine. MSHDA isn’t just a government agency; it’s a specialized financial tool designed to provide the necessary thrust to move you from a rental agreement to a home deed. By offering down payment assistance (DPA), they help bridge the distance between your current savings and the keys to your new home.

A MSHDA loan typically operates as a “silent second” mortgage. Think of this as a stabilizer for your financial flight path. This second loan often has 0% interest and requires no monthly payments, staying quietly in the background until you sell or refinance. It provides the stability you need to secure a primary mortgage without draining every cent of your emergency fund. However, launching this program successfully requires precision. Partnering with an expert MSHDA mortgage lender Battle Creek homebuyers rely on ensures your paperwork is filed correctly and your application meets every state guideline. Your lender acts as your navigator, keeping you on course when the technical jargon feels overwhelming.

Why Battle Creek is an Ideal MSHDA Market

Battle Creek is a high-opportunity zone for buyers in 2026. Because large parts of the city are designated as “targeted areas,” the purchase price limits are generous, reaching up to $566,355. This aligns perfectly with local housing inventory, where many well-maintained homes fall well within these boundaries. Local expertise is vital here. A navigator who understands Calhoun County appraisals can help you identify properties that meet MSHDA’s safety and value standards, ensuring your flight plan doesn’t hit unexpected turbulence during the inspection phase.

The ‘Down Payment Gap’ and How to Close It

The ‘Down Payment Gap’ is the financial distance between the liquid cash you have in your savings account and the total amount required for your down payment and closing costs. In Battle Creek, where rent prices have continued to climb, many residents find themselves caught in a cycle where they can afford a monthly mortgage payment but can’t save enough to clear the initial entry hurdle. The MSHDA path allows you to close this gap using state-backed funds instead of years of aggressive saving. This provides immense emotional relief, as it keeps your emergency savings intact for the actual move and future home maintenance.

The MSHDA MI Home Loan: Your Financial Booster Rocket

If the primary mortgage is your aircraft, the MI Home Loan is the high-performance engine that powers your ascent. This program serves as the foundational structure for most state-backed purchases, providing a stable, fixed-rate mortgage that works in tandem with down payment assistance. To get this engine started, you’ll need a minimum credit score of 640. This isn’t a hurdle meant to ground you; it’s a safety threshold that ensures your financial flight plan is viable for the long haul. Partnering with a seasoned MSHDA mortgage lender Battle Creek families trust is the most effective way to verify your score and prepare your application for a smooth takeoff.

The real acceleration for your home purchase comes from the MI 10K DPA. This program provides up to $10,000 in assistance to cover your down payment and closing costs. Unlike traditional loans that add to your monthly overhead, this is a zero-interest, no-payment second mortgage. It sits quietly on your home’s title, requiring repayment only when you eventually sell the property, refinance, or pay off the primary mortgage. It acts as a strategic reserve, allowing you to keep your personal cash in your pocket while you begin building equity in the Calhoun County market.

MI Home Loan vs. MI 10K DPA: Which Path is Yours?

Choosing the right assistance level depends on your specific destination. While the standard MI Home Loan provides a solid foundation, the MI 10K DPA offers a more aggressive boost for those buying in high-need areas. In 2026, many neighborhoods within Battle Creek qualify for this maximum assistance, effectively erasing the entry barrier for qualified borrowers. These programs can often be layered with other michigan first time home buyer programs to maximize your savings. If you’re unsure which route offers the best lift, a quick consultation with a local mortgage navigator can help clarify your options.

MSHDA for Repeat Buyers in Calhoun County

Many people mistakenly believe that MSHDA assistance is reserved exclusively for those who have never owned a home. This is a common misconception that often prevents experienced homeowners from exploring valuable tools. Because the City of Battle Creek is designated as a “Targeted Area,” the first-time homebuyer requirement is waived. This means even if you’ve owned a home before, you can still utilize MSHDA’s booster rocket to purchase a new residence in Battle Creek. You’ll simply need to ensure your previous home is sold before closing on the new one. This makes MSHDA an excellent option for those looking to upgrade or relocate within the city while maintaining their financial stability. It’s often a more flexible alternative to standard FHA loans when you need significant help with the initial cash requirements.

Comparing MSHDA with FHA and Conventional Navigation Routes

Selecting the right financing is like plotting a course through varying weather conditions; you need the right tools for your specific environment. While some buyers might look at a standard loan, working with a specialized MSHDA mortgage lender Battle Creek navigator allows you to layer assistance programs for maximum efficiency. One of the most effective strategies involves combining the Michigan State Housing Development Authority (MSHDA) assistance with other loan types to lower your initial cash outlay. This layering effect provides the necessary thrust to get your homeownership goals off the ground without waiting years to save a massive down payment.

The primary difference between these flight paths lies in how they handle risk and monthly costs. Every low down payment loan requires some form of insurance to protect the lender, often referred to as Private Mortgage Insurance (PMI) or Mortgage Insurance Premium (MIP). This insurance acts as a safety net, but it also impacts your monthly “fuel” consumption, or your budget. By comparing these routes side-by-side, you can decide which provides the most stable altitude for your long-term financial health. We also look at “Seller Concessions,” where the home seller pays a portion of your closing costs, as a way to further reduce the cash you need at the closing table.

MSHDA + FHA: The Most Popular Flight Plan

This combination is the go-to for buyers with credit scores in the 640 to 660 range who need maximum flexibility. A standard FHA Mortgage requires a 3.5% down payment, which the MSHDA DPA covers entirely. This specific pairing maximizes financial leverage for Battle Creek buyers by virtually eliminating the need for a large personal down payment. It’s an approachable route that allows families to enter the market sooner rather than later.

The Conventional MSHDA Route: When to Choose It

The Conventional MSHDA path typically requires a higher credit score but offers distinct advantages for those who qualify. It often features lower monthly insurance costs and can be more attractive to sellers in a competitive Battle Creek multi-offer scenario. Because Conventional appraisals can sometimes be less stringent than government-backed inspections, this path may provide a smoother landing if you’re looking at a home that needs minor cosmetic updates. It’s a precision-engineered option for buyers with established credit who still want to keep their liquid savings for future home improvements.

Your Pre-Flight Checklist: Qualifying for MSHDA in 2026

Before any pilot taxis onto the runway, they complete a meticulous pre-flight checklist. Your homeownership journey requires the same level of preparation. Qualifying for state-backed assistance isn’t a matter of luck; it’s a matter of meeting specific engineering standards. Missing a single requirement can delay your closing or ground your application entirely. By partnering with an experienced MSHDA mortgage lender Battle Creek specialist, you ensure every box is checked before you ever make an offer on a home.

This checklist serves as your roadmap to a successful closing. We recommend reviewing these five critical steps at the very start of your process:

- Verify your credit score: You’ll need a minimum score of 640 for standard single-family homes. If you’re looking at a multiple-section manufactured home, the floor rises slightly to 660.

- Audit your household income: MSHDA looks at the total income of everyone living in the home. These limits vary by family size and location.

- Confirm the purchase price: For Calhoun County in 2026, the sales price limit is a generous $566,355, which covers the vast majority of local inventory.

- Enroll in flight school: Every MSHDA borrower must complete a state-approved homebuyer education course.

- Choose your navigator: Work with a local, certified lender who understands the specific nuances of the Battle Creek market.

Income and Purchase Price Limits for Battle Creek

Because the City of Battle Creek is designated as a “Targeted Area,” the income ceilings are more flexible than in other parts of Michigan. For 2026, a household of 1 to 2 persons can earn up to $118,080, while families of 3 or more have a limit of $137,760. These higher thresholds are designed to encourage investment in the community. This targeted status also allows repeat homebuyers to access the program, a benefit not usually available in non-targeted regions of Calhoun County where income limits for a 1 to 2 person household sit lower at $98,400.

The Role of Homebuyer Education Classes

The required homebuyer education course isn’t just a hurdle of red tape; it’s flight school for your personal finances. These classes cover essential topics like long-term budgeting, home maintenance, and the mechanics of escrow accounts. You can complete these courses online or through local Battle Creek providers. Once finished, you’ll receive a certificate that becomes a mandatory part of your flight log for final loan approval. Taking this step early shows sellers that you’re a prepared and serious buyer.

Ready to see if you meet the criteria for takeoff? Contact our Battle Creek team to start your official pre-approval checklist today.

Why Jeremy Drobeck is Your Trusted MSHDA Navigator in Battle Creek

In the high-stakes world of mortgage lending, you don’t just need a service provider; you need a navigator who has flown this route hundreds of times. Jeremy Drobeck and the team at Treadstone Mortgage have established themselves as the premier MSHDA mortgage lender Battle Creek families rely on for precision and care. As a top-ranked MSHDA lending partner in Michigan, our expertise isn’t just a claim; it’s a documented record of helping families achieve lift-off when other lenders might have grounded the application. We understand that a mortgage is more than a transaction; it’s the propulsion system for your future.

Based in the Kalamazoo and Battle Creek corridor, Jeremy brings a deep sense of local community expertise to every file. This local presence means your loan isn’t being processed by a distant algorithm in a different time zone. Instead, you’re working with a neighbor who understands the specific housing inventory in Calhoun County and the nuances of the local market. We’ve stripped away the confusing government jargon and replaced it with clear, supportive directions. From the initial pre-approval to the final signature at the closing table, our promise is end-to-end support that keeps you informed at every altitude of the process.

Expertise That Lowers Your Financial Altitude (Stress)

MSHDA loans come with specific underwriting quirks that can ground a less experienced team. Our deep familiarity with state-backed programs allows us to anticipate potential turbulence and clear the path before it becomes an issue. We prioritize speed and precision, ensuring your MSHDA loan closes with the same efficiency as a conventional mortgage. This level of personalized care treats your home purchase as a significant life milestone. By handling the complex mechanical details of the loan in the background, we lower your stress levels and allow you to focus on the excitement of your new front door. You’ll never feel like you’re in a holding pattern when you have a seasoned navigator at the controls.

Start Your Battle Creek Homeownership Journey Today

Your path to homeownership begins with a simple, no-obligation “flight check” of your finances. We’ve engineered a streamlined digital application process through Treadstone that fits into your busy life, allowing you to submit documentation and track your progress from anywhere. It’s time to stop wondering if you’re eligible for assistance and start moving toward the runway. Our team is ready to review your goals and help you select the financial tools that provide the best lift for your budget. Don’t let the fear of a down payment keep you grounded any longer. Schedule your MSHDA consultation with Jeremy Drobeck today and let’s clear your financial flight plan for takeoff.

Clear the Runway for Your New Battle Creek Home

Your flight plan for homeownership in 2026 is now fully mapped. We’ve explored how the MI 10K DPA functions as a high-performance booster rocket, allowing you to bypass the traditional down payment barrier with up to $10,000 in assistance. You’ve also seen why Battle Creek’s status as a targeted area provides a unique advantage, offering more flexible income limits and opportunities for repeat buyers to re-enter the market. The final step is ensuring you have a steady hand at the controls to manage the technical paperwork and state guidelines.

Choosing a specialized MSHDA mortgage lender Battle Creek families trust makes all the difference in a smooth landing. With over 20 years of local Michigan lending expertise and a ranking as a Top 10 MSHDA Lender, Jeremy Drobeck and the Treadstone team are deeply familiar with Calhoun County market dynamics. We provide the end-to-end support you need to move from pre-approval to the closing table with total confidence. It’s time to stop dreaming about homeownership and start the engine on your future.

Secure Your Battle Creek MSHDA Pre-Approval with Jeremy Drobeck

Your new front door is closer than you think, and we’re ready to help you reach it.

Frequently Asked Questions

Is MSHDA only for first-time homebuyers in Battle Creek?

No, Battle Creek is a designated targeted area, which means the first-time homebuyer requirement is waived. This status clears the way for repeat buyers to use the program to purchase a primary residence. As long as you don’t own another home at the time of closing, you can utilize this financial lift to secure your next property in the city limits.

What is the minimum credit score for a MSHDA loan in 2026?

You’ll need a minimum credit score of 640 to qualify for a standard single-family home purchase. If your flight plan includes a multiple-section manufactured home, the requirement increases slightly to 660. Consulting with a MSHDA mortgage lender Battle Creek expert is the best way to verify your score and ensure your credit profile is ready for takeoff.

Do I have to pay back the MSHDA down payment assistance?

Yes, but the repayment doesn’t happen through monthly installments. The assistance acts as a silent second mortgage with 0% interest and no monthly payments. You only repay the balance when you sell the home, refinance your primary loan, or finish paying off your mortgage. It stays quietly in the background until your housing journey reaches its next major destination.

How long does it take to get approved for a MSHDA mortgage?

A typical MSHDA loan closes in 30 to 45 days from the time you have a signed purchase agreement. While government-backed programs involve extra layers of paperwork, an experienced navigator keeps the process moving at a steady, predictable pace. Starting your pre-approval early ensures all your documentation is cleared for a smooth, timely landing at the closing table.

Can I use MSHDA to buy a fixer-upper or a manufactured home?

Yes, MSHDA supports multi-section manufactured homes that are permanently attached to a foundation and taxed as real estate. For fixer-uppers, the property must generally be in move-in condition to meet state safety standards. However, you can often layer assistance with a renovation mortgage if the property requires specific repairs to reach flight readiness before you move in.

What are the income limits for MSHDA in Calhoun County?

Income limits in Calhoun County vary based on family size and the specific neighborhood’s targeted status. In Battle Creek’s targeted zones, the 2026 limit is $118,080 for 1 to 2 persons and $137,760 for 3 or more. In non-targeted parts of the county, these ceilings are lower, starting at $98,400 for smaller households and $113,160 for larger families.

Are there any hidden fees with MSHDA down payment assistance?

There are no hidden fees or surprise costs associated with the state’s down payment assistance programs. You’ll still be responsible for standard closing costs like title insurance and appraisals, but the MI 10K DPA is specifically designed to help cover those expenses. Your lender will provide a transparent flight log of all anticipated costs well before you sign the final papers.

How do I find an MSHDA approved homebuyer education class near Battle Creek?

You can find approved classes through the official state website or by asking your loan officer for a list of certified local providers. These courses are available both online and in-person near Battle Creek. Completing this education is a mandatory part of your flight preparation and provides the essential tools needed for long-term homeownership success in Michigan.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”