How to Qualify for a DSCR Loan in Michigan: Your 2026 Investor Flight Plan

Your personal tax returns shouldn’t be the anchor that keeps your real estate portfolio grounded, especially when Michigan’s rental market is showing such steady lift in 2026. It’s a common frustration for seasoned investors; you’ve found a high-performing property in Grand Rapids or Detroit, but traditional lenders are more interested in your debt-to-income ratio than the building’s actual income. Learning how to qualify for a DSCR loan in Michigan allows you to shift the focus back to where it belongs: the property’s performance.

We understand that navigating 2026 interest rate volatility and Michigan-specific property tax uncapping can feel like flying through a storm. This guide provides a clear flight plan to master the technical mechanics of Debt Service Coverage Ratio loans, allowing you to scale your portfolio without the burden of personal income verification. We’ll examine the current 6.12% to 7.50% rate environment, the 640 minimum credit score requirement, and the specific steps needed to use property cash flow to secure your next closing in record time. By the end of this article, you’ll have the technical precision required to engineer a portfolio that grows as fast as your ambition.

Key Takeaways

- Learn how to bypass traditional debt-to-income limits by using the property’s rental income as the primary engine for loan approval.

- Master the specific metrics of how to qualify for a DSCR loan in Michigan, including the necessary credit clearance and the Debt Service Coverage Ratio required for 2026.

- Understand why property performance in local hubs like Kalamazoo and Portage is more critical to your success than your personal W-2 history or tax returns.

- Follow a streamlined pre-flight checklist to secure fast pre-approvals and signal your intent to sellers in Michigan’s competitive investment market.

- Discover the value of a local navigator like Jeremy Drobeck at Treadstone Mortgage to handle the technical complexities of your investment journey from takeoff to landing.

Navigating the DSCR Loan Terrain: A Michigan Investor’s Starting Point

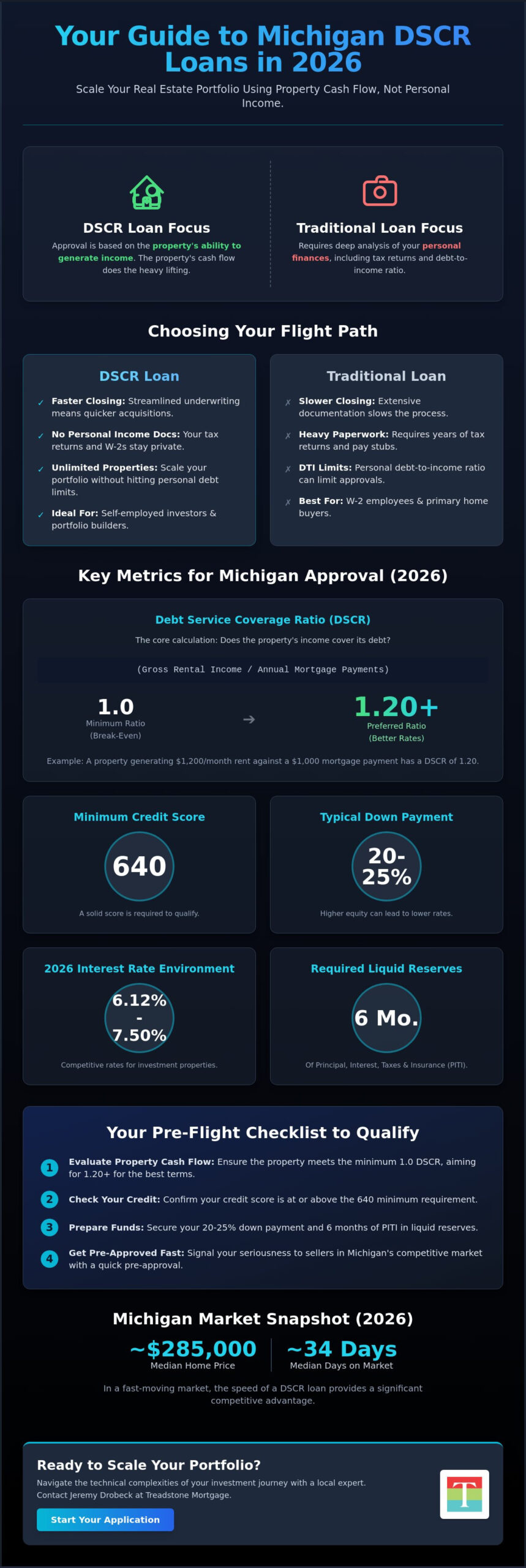

Think of a Debt Service Coverage Ratio loan as the auto-pilot system for your real estate portfolio. While a traditional Purchase Mortgage relies heavily on your personal flight history, including tax returns and debt-to-income ratios, a DSCR loan focuses almost entirely on the aircraft’s performance. In this scenario, the “aircraft” is your investment property. By shifting the focus to property cash flow, investors can bypass the heavy documentation that often keeps ambitious portfolios grounded. Understanding how to qualify for a DSCR loan in Michigan is the first step toward scaling your investments with technical precision and speed.

The 2026 Michigan market presents a unique landscape for this approach. With median home prices stabilizing around $285,000 and West Michigan seeing steady appreciation, the demand for quality rentals remains high. Whether you’re looking at Grand Rapids or the surrounding communities, the ability to close quickly without waiting for personal income verification is a significant competitive advantage. In a market where the median days on market is roughly 34 days, being able to signal your intent to fly with a streamlined loan process can be the difference between securing a high-performing asset or watching it slip away.

The Mechanics of Debt Service Coverage Ratio

At its core, the Debt Service Coverage Ratio (DSCR) is a calculation of “lift.” Lenders look at the Net Operating Income (NOI) generated by the property and compare it to the annual debt service. A ratio of 1.0 means the property generates exactly enough income to cover the mortgage payments, representing a break-even point. For most Michigan lenders, this is the minimum threshold for entry. However, achieving a higher ratio, such as 1.20 or above, often allows you to reach a more favorable interest rate altitude. A property that produces $1,200 in monthly rent against a $1,000 mortgage payment provides the stability lenders look for, proving the investment can sustain itself without outside fuel.

DSCR vs. Traditional Financing: Choosing Your Flight Path

When comparing DSCR loans to traditional options like FHA Loans in Michigan, the primary trade-off is speed versus cost. Traditional loans often offer lower interest rates but come with significant documentation “turbulence,” requiring years of tax returns and strict debt-to-income checks. DSCR loans typically carry rates between 6.12% and 7.50% in the current 2026 environment, which is slightly higher than conventional averages. However, the closing times are significantly faster because the underwriting is simplified. This makes DSCR the most reliable vehicle for self-employed investors or those who already have multiple properties and don’t want their personal credit capacity stretched to the limit. Knowing how to qualify for a DSCR loan in Michigan allows you to keep your personal finances private while your property does the heavy lifting.

The Qualification Flight Plan: Key Metrics for Michigan Approval

Every successful takeoff requires a rigorous pre-flight inspection. When you’re looking at how to qualify for a DSCR loan in Michigan, that inspection focuses on the financial mechanics of your investment property rather than your personal paychecks. While your tax returns stay grounded, the property’s ability to generate “lift” through rental income becomes the primary metric for approval. In the 2026 market, lenders are looking for a specific balance of cash flow, credit readiness, and liquid reserves to ensure the journey is stable from closing day to long term management.

Securing your clearance for a DSCR loan typically starts with a down payment of 20% to 25%. While some products allow for an 80% loan-to-value ratio, bringing more equity to the table can often lower your interest rate altitude. Beyond the down payment, you’ll need to demonstrate “fuel reserves.” These are liquid assets, usually equivalent to six months of principal, interest, taxes, insurance, and association fees (PITIA), held in a bank account to prove you can handle unexpected turbulence like a temporary vacancy or emergency repair.

Calculating Your Ratio: The DSCR Formula

The fundamental equation for this loan is simple: divide your gross monthly rent by the property’s total monthly PITIA. To determine the rent side of the equation, lenders don’t just take your word for it; they use a Form 1007 rent schedule completed by an appraiser to estimate current market rates. It’s vital to account for Michigan-specific variables in your PITIA calculation, such as property tax uncapping after a sale and the rising costs of landlord insurance in the Great Lakes region. If your property is part of a condo development in Grand Rapids, don’t forget to include those monthly HOA fees, as they directly impact your final ratio.

Credit and Liquidity: Your Financial Flight Readiness

While the property does the heavy lifting, your credit score still acts as the navigator. Treadstone Mortgage allows credit scores starting at 640, but reaching a 700 or higher provides the smoothest path to the most competitive 2026 rates. Maintaining high credit standards aligns with the Michigan prudent investor rule, which emphasizes the importance of making disciplined, well-researched financial decisions. If you’re looking to scale quickly, you can actually use a DSCR Loan to finance multiple properties at once, provided your liquidity reserves can cover the collective debt service. If you aren’t sure where your current metrics land, it’s a good idea to review your scenario with a specialist who understands the local Michigan terrain.

Evaluating the Property: West Michigan’s Rental Performance

In the world of DSCR lending, your personal financial history takes a backseat while the property itself becomes the star of the application. The primary question lenders ask isn’t about your salary; it’s whether the property has the mechanical strength to support its own debt. Understanding how to qualify for a DSCR loan in Michigan requires a deep dive into local market data to ensure your chosen asset can maintain a steady altitude. Whether you’re targeting a single-family home, a 2-4 unit multi-family property, or a warrantable condo, the property’s “flight worthiness” is determined by its ability to generate consistent Net Operating Income (NOI).

West Michigan offers a diverse range of terrains for investors. While some national guides focus solely on high-yield but volatile urban centers, stable markets like Kalamazoo and Portage provide a more predictable journey. These areas benefit from a mix of healthcare professionals and a robust student population, creating a consistent demand for quality housing. By focusing on the asset’s performance rather than your personal W-2, you can leverage the strength of the Michigan rental market to expand your holdings more rapidly than traditional financing allows. The goal is to identify a property where the rental engine is powerful enough to carry the weight of the mortgage, insurance, and taxes without needing outside fuel.

Kalamazoo and Battle Creek: Stable Rental Altitudes

Kalamazoo’s rental market is powered by a reliable student housing engine that provides consistent NOI for savvy investors. With Western Michigan University and local colleges driving demand, multi-family properties often see lower vacancy rates than the national average. In Battle Creek, we’re seeing multi-family assets gain significant traction in 2026 as investors seek value and higher yields outside the immediate Grand Rapids area. When calculating your ROI, consider whether a traditional long-term lease or a short-term rental strategy provides the most lift for your specific debt service ratio. Both paths are viable, but each requires a different approach to documenting projected income during the qualification process.

The Property Tax Trap: Avoiding Mid-Flight Turbulence

One of the most common causes of mid-flight turbulence for Michigan investors is the “uncapping” of property taxes. Under Michigan’s Proposal A, when a property transfers ownership, its taxable value resets to the State Equalized Value (SEV), which can lead to a tax increase of 50% or more. You must calculate your DSCR ratio using the projected post-sale tax amount rather than the current owner’s capped rate to ensure your cash flow remains positive. Failing to account for this reset is a frequent mistake that can sink an application during underwriting. Working with a local navigator who understands these regional tax nuances is essential to prevent unexpected denials and ensure your investment remains profitable long after the closing papers are signed.

The Pre-Flight Checklist: Steps to Qualify and Close Fast

Achieving a smooth landing at the closing table requires more than just a good property; it requires a disciplined pre-flight checklist. Mastering how to qualify for a DSCR loan in Michigan is about following these steps with precision to ensure your application moves through the system without delays. Because we aren’t waiting on tax returns or complex income audits, the timeline is significantly shorter, but the preparation must be just as rigorous. Your checklist should follow this trajectory:

- Step 1: Identify the Asset. Focus on properties with strong cash-flow potential in established rental markets like Grand Rapids or Kalamazoo.

- Step 2: Secure Pre-Approval. This document signals your ‘intent to fly’ to sellers, proving you have the credit clearance and liquidity to close.

- Step 3: The Appraisal. This is the most critical component, as it verifies the property’s income engine through a professional rent schedule.

- Step 4: Underwriting and Closing. A final technical review ensures the property meets the required ratio before you reach touchdown.

By focusing on these specific milestones, you can move from an initial offer to a completed transaction quickly. This speed is a major advantage in the 2026 market, where high-performing properties don’t stay available for long. Knowing how to qualify for a DSCR loan in Michigan allows you to act while other investors are still gathering their tax returns.

The DSCR Appraisal: Measuring Your Performance

The appraiser determines ‘Fair Market Rent’ by looking at comparable rentals in the immediate Michigan area. If the appraisal ‘under-shoots’ the expected rent, it can lower your ratio and potentially increase your required down payment. This is why property condition is so important. To maximize your valuation, ensure the property is clean, functional, and ready for occupancy. Appraisers look for properties that can command premium rates immediately. If the market rent doesn’t quite hit the target, we can often look at alternative data or adjust the loan-to-value ratio to keep the deal on track.

Documenting Your Flight Plan

While you don’t need tax returns, you’ll still need to provide identification and any relevant LLC documents if you plan to hold the title in a business name. Many investors prefer LLC vesting for the liability protection it offers. It’s also vital to maintain ‘radio silence’ on new personal debt during this time. Even though your personal debt-to-income ratio isn’t the primary factor, large new purchases can impact your credit score or liquid reserves. These metrics are still part of the final verification. For a better sense of the current environment, you can check Current Mortgage Rates in Kalamazoo to see how they might influence your property’s cash flow. If you’re ready to start your journey, connect with our team for a custom flight plan and secure your pre-approval today.

Partnering with a Navigator: Jeremy Drobeck – Treadstone Mortgage

Even with a perfect flight plan, the most successful investors know they shouldn’t fly solo. Real estate investment is a high-stakes journey, and having a local co-pilot who understands the specific crosswinds of the Michigan market is essential. Jeremy Drobeck – Treadstone Mortgage provides the expert navigation you need to move from a single property to a flourishing portfolio. While national lenders might offer a generic approach, Jeremy focuses on the technical nuances of the West Michigan landscape, from the intricacies of Grand Rapids appreciation to the specific challenges of Kalamazoo property tax uncapping. By understanding the local terrain, he ensures that your strategy for how to qualify for a DSCR loan in Michigan is built on a foundation of precision rather than guesswork. This partnership shifts the experience from a cold transaction to a supportive relationship where your long-term goals are the priority.

Beyond DSCR: Building a Comprehensive Portfolio

Building a comprehensive portfolio often requires switching between different financial vehicles as your needs evolve. You might start by utilizing Renovation Mortgages to add value to a distressed property in an up-and-coming neighborhood before transitioning into a DSCR loan to stabilize the asset. This move allows you to free up capital and prepare for your next acquisition without the constraints of personal debt-to-income limits. The synergy between Jeremy’s local expertise and premium-tier lending products allows you to maintain momentum without hitting documentation bottlenecks. His “no-hidden-fees” promise ensures that you have a clear-skies view of your closing costs, preventing any last-minute turbulence that could derail your investment goals. It is this level of transparency that builds the trust necessary for a multi-property journey.

Ready for Takeoff? Schedule Your Flight Planning Session

If you’re ready to see how your specific property performs under the DSCR lens, you can secure a property-specific quote in under 24 hours. This rapid response time is critical in Michigan’s 2026 market, where the window of opportunity for high-yield properties can close in a matter of days. For your first flight planning session with Jeremy Drobeck – Treadstone Mortgage, simply bring your property details, projected rental income data, and an overview of your investment goals. The Treadstone difference lies in meticulous care for every milestone, providing end-to-end support from the initial inquiry to the final touchdown at the closing table. Learning how to qualify for a DSCR loan in Michigan doesn’t have to be a stressful ordeal when you have a seasoned navigator by your side. Reach out today to schedule your consultation and take the first step toward a more scalable, cash-flowing future that isn’t tied to your tax returns.

Launch Your Michigan Investment Portfolio Today

Scaling a rental portfolio in 2026 requires a shift in perspective. You’ve seen that the key to unlocking growth isn’t found in your personal tax returns, but in the mechanical strength of your property’s cash flow. By mastering the technical details of how to qualify for a DSCR loan in Michigan, you can bypass traditional debt-to-income limits and move toward your financial goals with precision. This specialized approach turns property performance into your primary engine for expansion, allowing for faster closing times and a more streamlined path to success.

Success in markets like Kalamazoo, Portage, and Battle Creek depends on more than just finding a building; it requires a navigator who understands regional nuances like property tax uncapping and NOI optimization. Jeremy Drobeck – Treadstone Mortgage provides the steady, expert guidance needed to handle complex DSCR, Renovation, and FHA investment paths. With deep local roots and a commitment to meticulous care, he’s ready to help you manage every milestone of your journey. Don’t let traditional lending hurdles keep your ambitions grounded any longer.

Schedule Your 2026 Investment Flight Plan with Jeremy Drobeck – Treadstone Mortgage and take the first step toward a more profitable horizon. We’re here to ensure your next investment reaches its full potential with a smooth, controlled landing at the closing table.

Frequently Asked Questions

What is the minimum DSCR ratio required in Michigan for 2026?

A ratio of 1.0 is the standard break-even point for most Michigan lenders in 2026. This means the property’s gross income exactly covers the debt service. Aiming for a 1.20 ratio or higher often provides more lift, helping you secure a more favorable interest rate altitude during the underwriting process.

Can I qualify for a DSCR loan with a 620 credit score?

Treadstone Mortgage typically requires a minimum credit score of 640 for DSCR products. While a 620 might ground your application for this specific program, we can often look at other flight paths or help you prepare for a future takeoff once your score reaches the necessary clearance. Higher scores generally lead to smoother approvals and lower rates.

Does a DSCR loan require a personal guarantee?

Yes, most DSCR loans require a personal guarantee from the members of the LLC or the individual borrower. Although the loan is qualified based on property cash flow and doesn’t impact your personal debt-to-income ratio, the guarantee provides a safety net for the lender. This ensures all parties are committed to a successful journey from takeoff to landing.

How much is the typical down payment for a Michigan DSCR loan?

You should plan for a down payment between 20% and 25% of the property’s purchase price. While some programs allow for an 80% loan-to-value ratio, bringing more equity to the runway can lower your monthly debt service. This extra equity often helps you achieve a stronger debt service coverage ratio.

Can I use a DSCR loan for a short-term Airbnb rental in Kalamazoo?

You can absolutely use a DSCR loan for short-term rentals in Kalamazoo or other West Michigan hubs. We specialize in products that account for the unique income streams of Airbnb and VRBO properties. We’ll use market data to confirm the property has the necessary power to support its own debt service.

Are DSCR interest rates higher than conventional investment rates?

DSCR interest rates in 2026 typically range from 6.12% to 7.50%, which is generally 0.75% to 1.5% higher than conventional investment rates. This slight premium is the trade-off for the convenience of bypassing personal income verification. It allows you to close with significantly less documentation turbulence than a traditional mortgage.

What happens if my property is currently vacant?

Vacant properties can still qualify if the appraiser’s Form 1007 rent schedule confirms strong market demand. We use these professional estimates to determine how to qualify for a DSCR loan in Michigan when a tenant isn’t currently in place. This ensures your investment journey doesn’t stall simply because the property is between leases.

How long does it take to close a DSCR loan with Jeremy Drobeck – Treadstone Mortgage?

Closing a DSCR loan with Jeremy Drobeck – Treadstone Mortgage is significantly faster than a traditional mortgage, often taking just three to four weeks. Because we don’t have to navigate the complex clouds of personal tax audits, the underwriting process is much more efficient. This speed allows you to secure high-performing assets before competitors can even get their paperwork in order.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”