How to Avoid Mortgage Pre-Approval Denial: Your 2026 Michigan Homeownership Flight Plan

Imagine finding the perfect bungalow in Kalamazoo only to have your dream grounded because a minor credit shift triggered a rejection at the last minute. It’s a common fear for many Michigan buyers, but a pre-approval letter isn’t just a one-time pass; it’s a flight plan that requires steady hands on the controls until you land at the closing table. Understanding how to avoid mortgage pre-approval denial is about more than just having a good job; it’s about maintaining your financial altitude while the mortgage industry shifts around you.

We know that the complexity of debt-to-income ratios and credit fluctuations can feel like flying through heavy fog. You want to feel confident that your 2026 mortgage is secure, especially with Michigan’s conforming loan limits now reaching $832,750 for single-unit properties. This article will provide the expert guidance you need to keep your homebuying journey on course. We’ll break down a clear checklist of financial dos and don’ts, explain how to manage your debt-to-income ratio effectively, and show you how to protect your standing so you can reach your goal of homeownership with total precision.

Key Takeaways

- Treat your pre-approval as a live flight plan that requires constant monitoring to ensure you stay cleared for the Kalamazoo housing market.

- Learn how to avoid mortgage pre-approval denial by managing your debt-to-income ratio and keeping your credit score at the optimal altitude for the best possible interest rates.

- Determine which loan “vessel”—from Conventional to FHA or MSHDA—is the most stable fit for your specific financial cargo and long-term homeownership goals.

- Avoid the common “no-fly” errors, like job hopping or major purchases, that frequently disrupt the transition from pre-approval to final closing.

- Gain the confidence to navigate the “Clear to Close” milestone with the help of a local navigator who understands the unique terrain of the Michigan real estate landscape.

Understanding the Mortgage Pre-Approval Radar

Before you even tour a craftsman home in the Vine neighborhood or a modern build in Oshtemo, you need to know if you’re cleared for takeoff. Think of a mortgage pre-approval as your financial flight clearance. It’s the signal to sellers that your financing is engineered for success. In a market like Kalamazoo, where median days on market can be as low as 14 to 24 days, having this clearance is your only ticket to a serious seat at the negotiation table. Without it, your offer will likely be ignored by sellers who are already fielding multiple bids from prepared buyers.

Lenders use a sophisticated radar system to scan your financial horizon. They aren’t just looking at a single number; they are evaluating your income stability, asset reserves, and credit reliability. This scan is the primary component of the mortgage underwriting process, where a professional risk assessor determines if your flight plan is viable. Mastering how to avoid mortgage pre-approval denial requires moving beyond simple estimates and into the territory of verified facts. It’s about showing the lender that your financial vessel is structurally sound and ready for the journey ahead.

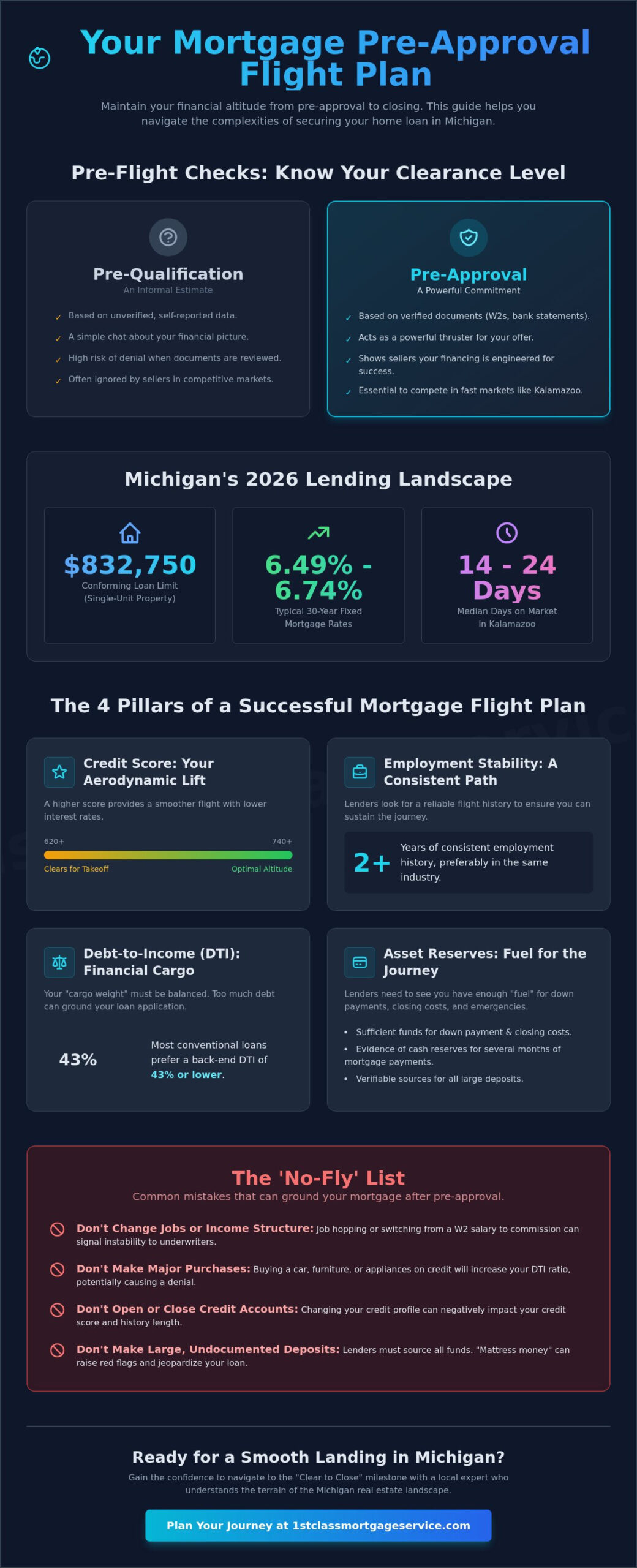

Pre-Qualification vs. Pre-Approval

Don’t confuse a “soft” pre-qualification with a true pre-approval. A pre-qualification is essentially an informal chat based on unverified data. If you rely on this, you risk a mid-flight denial when the actual documentation reveals a different story. To truly secure your position, you must provide the “black box” of your finances early. This includes W2s, bank statements, and tax returns. In competitive areas like Portage, a verified, underwritten pre-approval acts as a powerful thruster for your offer. It proves you’ve already passed the toughest inspections, giving the seller peace of mind that the deal won’t fall apart before closing.

The 2026 Lending Landscape in Michigan

As of June 2026, 30-year fixed mortgage rates in Michigan are hovering between 6.49% and 6.74%. These rates directly impact your maximum loan altitude, which is the total amount you can afford to borrow. While the 2026 conventional conforming loan limit has risen to $832,750 for single-unit properties, higher rates mean your monthly debt obligations are a bigger factor than in previous years. Local expertise is vital here. A Michigan-based navigator understands how local property taxes and the state transfer tax impact your closing costs. They’ll help you prepare for modern underwriting standards that prioritize long-term stability over quick approvals.

The Four Pillars of a Successful Mortgage Flight Plan

A stable flight requires more than just a powerful engine; it needs a balanced airframe and a clear trajectory. To stay clear of the ground, your financial profile must rest on four specific supports that lenders examine with high-resolution detail. These pillars determine not just your eligibility, but the cost of your loan over the next 30 years. Understanding these requirements is the most effective way to learn how to avoid mortgage pre-approval denial before you ever set foot in an open house.

Your credit score provides the aerodynamic lift. While you can often clear the runway with a 620, a score of 740 or higher ensures the smoothest flight with the lowest interest rates. Many buyers face common barriers to homeownership like high credit utilization or thin files, but addressing these early prevents a last-minute rejection. Beyond credit, lenders look for a consistent flight path through employment stability. Typically, they want to see a two-year history in the same industry to ensure your income is reliable enough to sustain the journey.

Credit and DTI: The Engine Room

Your Debt-to-Income (DTI) ratio represents your financial cargo weight. If your monthly obligations are too heavy, your loan might not get off the ground. Lenders calculate two versions: the front-end ratio, which focuses on your housing costs, and the back-end ratio, which includes car loans, student debt, and credit cards. DTI is the percentage of gross monthly income that goes toward debt. Most Conventional loans prefer a back-end DTI of 43% or lower, though some FHA programs offer more flexibility for those carrying a bit more weight. If you aren’t sure where your ratios stand, talking to a professional can help you map out your current financial standing before you apply.

Assets and Down Payment Assistance

Assets are your fuel. You must prove you have the liquid reserves for a down payment, closing costs, and a few months of “emergency fuel” in the bank. Large, undocumented deposits can create sudden turbulence; underwriters need to see exactly where every dollar originated. If your personal reserves are low, MSHDA Down Payment Assistance can provide a significant boost, offering up to $10,000 for eligible Michigan buyers. Whether you use state programs or gift funds from family, a strict paper trail is required. Any “mystery money” that appears in your account without documentation can lead to a denial, as it may be flagged as an undisclosed loan.

Pre-Approval vs. Denied: Analyzing the Gap

A pre-approval letter is a declaration of intent, but it isn’t a guarantee of funding. Many Michigan buyers find themselves in a frustrating gap where they were cleared for takeoff but grounded just before the finish line. One of the most common reasons for this is a mismatch between the borrower’s profile and the specific loan vessel they’ve chosen. Knowing how to avoid mortgage pre-approval denial requires understanding that your financial standing must align perfectly with the guidelines of your chosen program. If your situation changes or if the property itself doesn’t meet the lender’s safety standards, your flight plan can be compromised.

Think of the “Conditional Approval” as your mid-way checkpoint. At this stage, the underwriter has reviewed your basic flight plan but still needs to verify the property’s condition and your final documentation. It is a moment of high-stakes scrutiny. If the home you’ve chosen in Kalamazoo has structural safety issues or fails to meet the appraisal value, your flight could be delayed or cancelled entirely. To stay on course, you must ensure that both your personal finances and the property you’re bidding on remain within the parameters set during that initial scan.

Choosing the Right Loan Product

Selecting the wrong loan type is like trying to fly a bush plane across an ocean. You need the right equipment for the specific terrain of your finances. For example, comparing FHA Loans in Michigan vs. Conventional options is vital for credit-challenged flyers. FHA guidelines are often more lenient regarding past credit turbulence or higher debt ratios. If you are looking at homes outside Battle Creek or in more rural townships, a USDA Rural Development Loan might be the more stable choice, offering zero-down payment options for eligible properties. For those eyeing a “fixer-upper” that might fail a standard safety inspection, Renovation Mortgages allow you to bundle repair costs into the loan, preventing a denial based on the home’s current condition.

Investor-Specific Navigation: DSCR Loans

Real estate investors in Michigan often require a completely different flight plan than standard homeowners. If you’re building a portfolio in Portage or Kalamazoo, personal income caps can sometimes lead to a denial on a traditional mortgage. This is where DSCR loans become an essential tool. These loans avoid personal income denial by focusing entirely on the property’s potential cash flow rather than your personal debt-to-income ratio. By skipping the personal income checks, you can maintain your momentum and continue expanding your investment fleet without the constraints of traditional residential underwriting.

The ‘No-Fly’ List: Common Mistakes to Avoid After Pre-Approval

Once you hold that pre-approval letter, the temptation to celebrate by shopping for your new home is high. However, the flight isn’t over until you land at the closing table. Learning how to avoid mortgage pre-approval denial requires a disciplined “hands off” approach to your finances during the weeks leading up to your move. Underwriters perform a final check of your credit and assets just before the “Clear to Close” is issued. Any deviation from your original flight plan can lead to an immediate grounding of your loan, even if you’ve already packed your boxes.

Think of your financial profile as a finely tuned engine. If you add unexpected weight or change the fuel mixture mid-flight, the entire system can fail. Stability is the most important factor during this phase. Lenders want to see the exact same borrower at the end of the process that they saw at the beginning. By avoiding a few common “no-fly” errors, you ensure that your path to homeownership remains clear and unobstructed.

The Impact of New Debt

Opening a new credit line for a furniture set or kitchen appliances might seem like a logical step, but it adds significant weight to your Debt-to-Income (DTI) ratio. A new $400 monthly car payment can slash your home buying power by $50,000 or more. This occurs because that monthly obligation is subtracted directly from the income available to support your mortgage. Even a small change in monthly obligations can disqualify a borderline DTI. Additionally, you should avoid credit inquiries or “hard pulls” entirely until you have the keys in hand, as these can cause your credit score to dip just enough to trigger a secondary review.

Employment and Income Shifts

Lenders value a consistent flight path. While a lateral move within the same industry for a higher salary is usually acceptable, a career change is a major flight risk. Switching from a steady W2 position to a 1099 or self-employed status is particularly dangerous during the mortgage process. Underwriters typically require a two-year history of self-employment income before they can count it toward your approval. If you are offered a new position, talk to your navigator before accepting. We can help you understand how a change in your pay structure might impact your ability to reach the finish line.

Large, undocumented deposits are another frequent cause of turbulence. If you suddenly deposit $5,000 without a clear paper trail, the lender may flag it as a red flag for an undisclosed loan. Similarly, co-signing for a friend’s vehicle or apartment lease adds that entire debt to your profile. Even if you aren’t the one making the payments, the legal obligation is yours. This “ghost debt” can push your DTI past the limit and result in a denial. To ensure your financial profile remains stable throughout the underwriting process, contact our team of experts for a personalized review of your flight plan.

Navigating Your Path to Closing in Kalamazoo and Beyond

Landing your dream home in West Michigan requires a navigator who knows the local airspace. While national call centers might offer generic checklists, a local Kalamazoo mortgage expert serves as a true co-pilot. Jeremy Drobeck and the Treadstone team are committed to maintaining your flight plan from the moment you receive your initial clearance until you reach the final destination. By staying present throughout the entire duration of the process, we help you understand exactly how to avoid mortgage pre-approval denial during the critical final approach. We monitor the horizon for potential issues, ensuring your trajectory remains stable while you focus on your move.

The “Clear to Close” milestone is the signal that all conditions have been met and your funding is ready for touchdown. Before this happens, you will receive your Closing Disclosure (CD). This document is your final chance to review the mechanics of your loan, including interest rates and closing costs, to ensure there is no last-minute turbulence. Our team reviews this with you, ensuring every detail aligns with the plan we engineered together. It is a moment of precision that marks the end of the technical journey and the beginning of your life in a new home.

The Local Advantage in West Michigan

Navigating local appraisal nuances in Portage and Battle Creek requires a deep understanding of neighborhood-specific values. An algorithm sitting in a different state cannot account for the unique charm of a specific Kalamazoo block or the impact of local school district boundaries. Michigan sellers often show a strong preference for offers backed by local, reputable lenders. They know that a local team provides the accountability and personalized support needed to keep a transaction on schedule. When a listing agent sees a Treadstone pre-approval, they see a flight plan that has been thoroughly vetted and is likely to close without delay.

Your Pre-Flight Consultation

Your journey begins with a pre-flight consultation. When you meet with a Treadstone loan officer, bring your “black box” of documentation. This includes recent pay stubs, your last two years of tax returns, and recent bank statements. This allows us to set a realistic budget based on current mortgage rates in Kalamazoo, which currently hover between 6.49% and 6.74%. Taking this first step ensures your financial standing is solid before you start touring homes. We are here to provide the expert guidance needed to turn your homeownership goals into a reality. It’s time to take the first step toward your new Michigan home with a team that stays by your side until you land safely.

Ready for Touchdown? Landing Your Michigan Homeownership Dream

Securing a home in 2026 requires more than just a pre-approval letter; it demands a steady hand on the controls until the keys are in your pocket. We’ve explored the essential pillars of financial lift and the no-fly mistakes that can ground a loan mid-flight. By choosing the right loan vessel, whether that is a specialized MSHDA program or a renovation mortgage, you ensure your flight plan is engineered for your specific needs. Mastering how to avoid mortgage pre-approval denial is about maintaining your financial altitude through every stage of the underwriting process.

With over 20 years of West Michigan lending expertise, our team at Treadstone, a division of Neighborhood Loans, Inc. (NMLS #222982), is ready to act as your dedicated navigator. We bring specialized knowledge in MSHDA and renovation loans to help you overcome local hurdles and clear the path to closing. Ready to file your flight plan? Get started with a local Kalamazoo mortgage expert today!

Your new Michigan home is on the horizon, and with a seasoned co-pilot by your side, you can land with total confidence.

Frequently Asked Questions

Can I get denied for a mortgage after being pre-approved?

Yes, a pre-approval is a preliminary clearance, not a final guarantee. Learning how to avoid mortgage pre-approval denial involves understanding that changes to your credit score or new debts can trigger a rejection during the final review. Property-related issues like a low appraisal can also ground your loan. Maintaining your financial stability from the moment you receive your letter until you sign the final papers is the only way to stay on course.

How long does a mortgage pre-approval last in Michigan?

A mortgage pre-approval letter is typically valid for 60 to 90 days. This timeframe allows you to shop the local market with confidence, but the clock starts the moment the letter is issued. If your search extends beyond this window, your lender will need to refresh your credit report and bank statements to ensure your financial standing hasn’t changed. Staying in close contact with your navigator ensures your clearance is updated before it expires.

What is the most common reason for a mortgage denial?

The most common reasons for denial after pre-approval include significant changes in your financial situation, such as a drop in credit score or an increase in debt-to-income (DTI) ratio. Lenders generally prefer a DTI of 43% or lower. If you take on a new car payment or max out a credit card, you might lose the “lift” needed for approval. Learning how to avoid mortgage pre-approval denial starts with keeping your spending and debt levels stable.

Can I change jobs after I get my pre-approval letter?

You should avoid changing jobs mid-flight if possible, as it can create significant turbulence for your approval. Lenders look for stability, usually requiring a two-year history in the same industry. While a lateral move for a higher salary might be acceptable, switching from a W2 role to self-employment is a major red flag that could lead to a denial. Always consult your loan officer before making any career shifts to protect your homeownership goal.

How much money should I keep in my bank account after pre-approval?

You should maintain at least the amount of liquid assets documented during your initial pre-approval. This includes funds for your down payment, closing costs, and any required cash reserves. Michigan closing costs typically range from 2% to 5% of the purchase price. On a $350,000 home, you’ll need between $7,000 and $17,500 ready. Avoid moving large sums between accounts or making major withdrawals, as underwriters require a clear paper trail for every dollar.

Does a mortgage pre-approval affect my credit score?

Yes, a pre-approval typically involves a hard credit pull, which may cause a small, temporary dip in your score. This is a necessary part of the process to verify your creditworthiness and determine your interest rate. However, multiple inquiries from different lenders within a short window usually count as a single event for scoring purposes. This minor dip is a small price to pay for the clearance needed to make a competitive offer in the Kalamazoo market.

What happens if my credit score drops during the home buying process?

A drop in your credit score can result in a higher interest rate or a complete denial of your loan application. Lenders perform a final credit refresh just before closing to ensure you still meet their risk standards. For programs like MSHDA, falling below the 640 minimum score requirement will immediately ground your loan. If you notice a dip, alert your lender immediately so they can help you navigate a path toward recovery before the final inspection.

What should I do if my mortgage application is denied?

If your application is denied, the first step is to review the “adverse action” notice to understand exactly why your flight was grounded. This document identifies the specific issues, such as high DTI or credit problems. Once you know the cause, you can work with an expert to build a recovery plan. This might involve paying down debt, correcting credit report errors, or switching to a different loan “vessel” like an FHA mortgage that offers more flexible guidelines.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”