What Not to Do While Your Mortgage is in Underwriting: A 2026 Guide to a Smooth Landing

Last week, a hopeful buyer discovered that a simple credit limit increase for new appliances was enough to ground their entire home purchase just days before the 50-day closing mark. It’s a heartbreaking scenario that turns a smooth flight into a sudden emergency landing right when you should be preparing to celebrate. You’ve worked hard to reach this milestone, yet the “black box” of the underwriting process often feels like a high-stakes mystery where one wrong move triggers a red flag. Knowing exactly what not to do while your mortgage is in underwriting is essential to protecting your investment and ensuring your loan clears the flight deck without delay.

We understand the anxiety of the closing window and the fear that a technicality might cost you your dream home. You deserve a steady ally who provides clear navigation through the final descent of your financial journey. This guide will teach you how to avoid the critical mistakes that derail approvals, answering the vital question of which specific actions cause underwriters to reject loans at the last minute. We’ll preview the red flags that modern AI-driven systems look for in 2026, giving you the peace of mind and the expert flight plan required to secure your “Clear to Close” notification with total confidence.

Key Takeaways

- Maintain total financial stability during the “final descent” to ensure your credit and asset profile matches your pre-approval exactly.

- Master the essential rules of what not to do while your mortgage is in underwriting to avoid common traps like new credit lines or undocumented cash deposits.

- Understand the unique asset limits and contractor contingency checks required for specialized programs like MSHDA assistance and renovation mortgages.

- Learn the “Mayday Protocol” for handling financial mistakes, including how to craft a Letter of Explanation that satisfies an underwriter’s inquiry.

- Leverage local expertise in the Kalamazoo and Portage markets to navigate regional lending requirements and reach a successful touchdown at the closing table.

The Underwriting “Flight Deck”: Why Stability is Your Only Objective

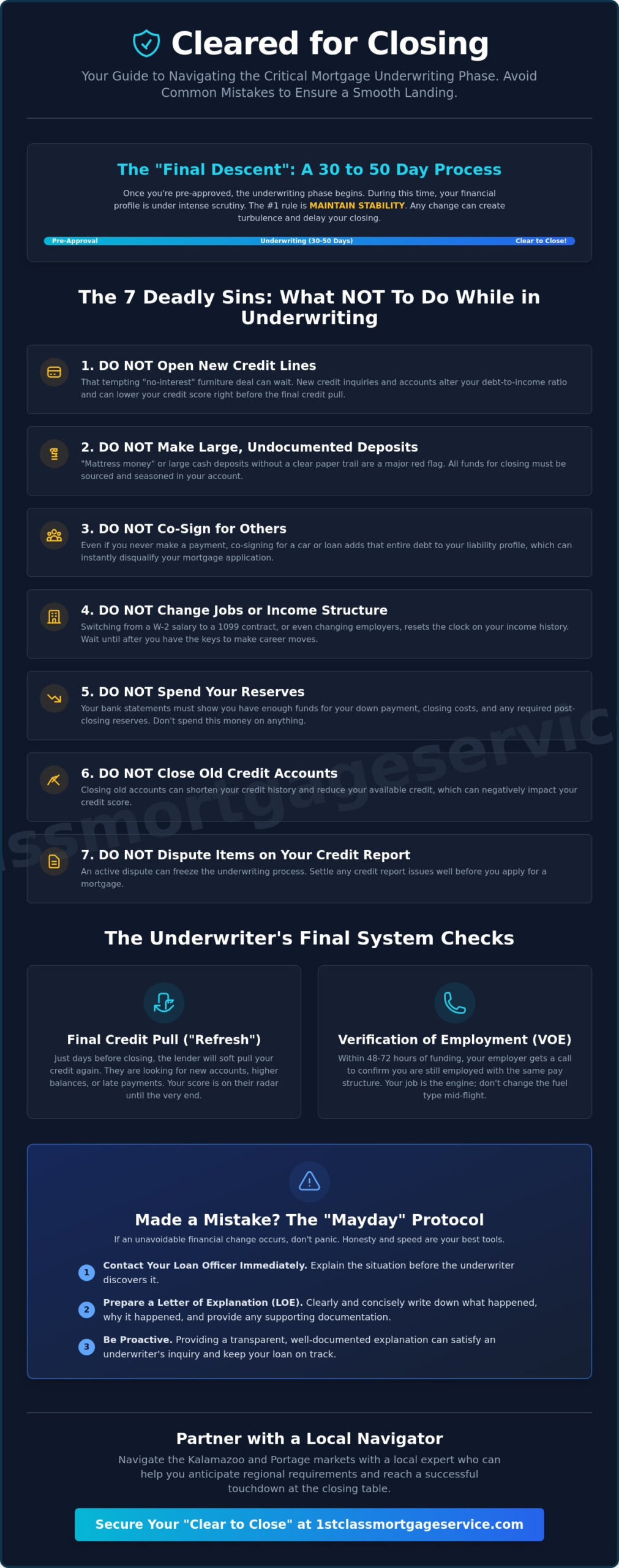

Think of the underwriter as the flight engineer performing a final systems check before the wheels touch the tarmac. While your pre-approval was the initial flight plan, mortgage underwriting in the United States is the rigorous, technical verification of your entire financial story. Many buyers mistakenly believe that once they have a pre-approval letter, the hard work is over. In reality, the 30 to 50 days spent in the underwriting phase are the most critical. This is your “final descent,” and for a smooth landing, your financial profile must remain exactly as it was when the journey began.

Any deviation in your debt-to-income ratio, asset levels, or credit history acts like unexpected turbulence. Underwriters aren’t just looking for reasons to say “no”; they are ensuring the safety of the loan for both you and the lender. This is why understanding what not to do while your mortgage is in underwriting is so vital. If you change the variables mid-flight, the engineer has to recalculate the entire trajectory. This often leads to frustrating delays or even a total grounding of your home loan. Stability is your only objective during this window.

The Final Credit Pull: Your Score is Still on the Radar

Don’t be fooled into thinking your credit score is locked in once you sign the initial application. Lenders almost always perform a “refresh” or a soft pull of your credit report just days before the scheduled closing. While this isn’t usually a hard inquiry that lowers your score, it reveals any new debts or increased balances. Even a 10-point drop caused by a high credit card balance can push you into a higher interest rate tier. In some cases, it can disqualify you from specific programs like a Conventional Mortgage or an FHA loan. Keep those cards tucked away and avoid any new financial commitments until you have the keys in hand.

The Verification of Employment (VOE) Check

Your job stability is the primary engine providing lift for your mortgage. Underwriters typically conduct a final Verification of Employment (VOE) within 48 to 72 hours of funding. They will call your employer to confirm you are still active and that your pay structure hasn’t changed. Switching from a steady salary to a commission-based role might seem like a career win, but it resets the clock on income stability requirements. Similarly, resigning or “quiet quitting” before the papers are signed is a catastrophic move. Staying the course is the only way to ensure a successful touchdown, and knowing what not to do while your mortgage is in underwriting includes keeping your professional life as stable as your bank account.

The 7 Deadly Sins: What Not to Do While Your Mortgage is in Underwriting

The period between your initial application and the final signature is a time for financial hibernation. While it’s tempting to start nesting, the underwriting phase is a delicate balance where even small movements can knock your loan off course. Underwriters are looking for absolute consistency. If you’ve been Preparing to shop for your mortgage by cleaning up your credit, don’t undo that hard work now. Here are the primary financial maneuvers that can ground your flight:

- Opening new credit lines: That “no interest for 24 months” furniture deal will show up on your final credit refresh.

- Making undocumented deposits: Cash from a side hustle or “mattress money” can’t be used without a clear history.

- Co-signing for others: Even if you aren’t making the payments, the full liability is added to your debt profile.

- Changing income structures: Moving from a W-2 salary to a 1099 contract role can disqualify your income history.

- Spending your reserves: Your bank balance must remain high enough to cover the closing costs and any required “cushion.”

- Closing old accounts: Reducing your available credit or shortening your credit history can cause your score to dip.

- Disputing credit items: Active disputes often require the underwriter to stop the process until the dispute is resolved.

Staying disciplined during this 30 to 50 day window is the best way to ensure your purchase mortgage clears the final hurdles. Any change in your financial profile requires the underwriter to re-verify your entire file, which often leads to delays or denied applications.

Large Deposits and the Paper Trail

In the eyes of an underwriter, any deposit that isn’t your regular paycheck is a potential red flag. Generally, any single deposit exceeding 25% of your total monthly gross income will require a meticulous paper trail. If you sell a vehicle to boost your down payment, you must provide the bill of sale and a copy of the check. Cash gifts from family are common, but they require a signed gift letter stating the funds don’t need to be repaid. Without this documentation, those funds might be excluded from your available assets, potentially stalling your approval. Knowing what not to do while your mortgage is in underwriting means keeping your bank statements as clean and predictable as possible.

The Danger of New Debt-to-Income (DTI) Ratios

Your Debt-to-Income ratio is the most sensitive instrument on your financial flight deck. A new $400 car payment might not seem like a deal-breaker, but at current 2026 interest rates, that monthly obligation can slash your borrowing power by over $60,000. Underwriters also keep a close eye on deferred student loans. If a grace period ends during underwriting, the new payment must be factored into your DTI. This is why it is so critical to understand what not to do while your mortgage is in underwriting; keep your debt profile frozen until you have the keys. If you have questions about a specific purchase, checking in with your loan officer first is the best way to avoid a mid-flight emergency.

Specialized Loans: How Underwriting Varies for MI Programs

While the standard flight rules apply to most borrowers, specialized lending programs often have additional sensors on the underwriting flight deck. If you are utilizing state-specific assistance or a niche product, the list of what not to do while your mortgage is in underwriting becomes even more specific. These programs are designed to provide lift for particular scenarios, but they come with tighter tolerances. A small change in your liquid assets might be manageable for a conventional loan, but it could disqualify you from a down payment assistance program entirely.

VA and USDA mortgages, for example, have strict occupancy and geographic requirements that underwriters verify late in the closing window. For a USDA loan, the property must remain in a designated rural area; the underwriter will double-check that your household income hasn’t climbed above the program’s limits right before funding. Similarly, VA underwriters ensure the home meets “Minimum Property Requirements” to guarantee it’s safe and sound for a veteran. Any major repairs you negotiate after the initial appraisal must be documented carefully, as unauthorized changes to the property condition can stall the final sign-off.

Navigating MSHDA and FHA Requirements

For those utilizing FHA loans in Michigan, property condition is paramount. Underwriters look for specific safety standards, such as peeling paint or missing handrails, which must be resolved before the loan clears the deck. If you are a MSHDA buyer, you must be exceptionally cautious with your liquid asset caps. MSHDA programs often have strict limits on how much cash you can have in the bank after closing. If you suddenly deposit a large sum, you might inadvertently exceed these caps and lose your assistance. Don’t forget the Michigan First Time Home Buyer educational requirement; failing to complete this course on time is a common reason for a delayed landing.

Renovation and DSCR Nuances

A renovation mortgage adds another layer of complexity because the underwriter is evaluating the “as-completed” value of the home. This involves checking contractor bids and ensuring there is a 10% to 20% contingency fund for unexpected repairs. Changing your contractor or significantly altering your renovation plans mid-underwriting is a major red flag that requires a total re-evaluation of the project. On the other hand, a DSCR loan focuses almost entirely on the property’s cash flow rather than your personal tax returns. In this scenario, the underwriter’s primary concern is the lease agreement and the debt service coverage ratio. Understanding what not to do while your mortgage is in underwriting for these specialized paths requires a navigator who knows the local terrain in Kalamazoo and Portage.

The Mayday Protocol: Damage Control for Underwriting Mistakes

Even the most disciplined pilot can hit a sudden pocket of turbulence. If you’ve already made a financial move that contradicts our list of what not to do while your mortgage is in underwriting, the most important thing you can do is speak up. Silence is the only mistake that can’t be corrected. Your Loan Officer is your navigator. They need to know about the anomaly before the underwriter discovers it during the final systems check. Silence is the real danger to your closing.

The first step in the Mayday Protocol is immediate disclosure. Whether you opened a new credit card for an emergency or received an unexpected cash gift, tell your LO today. They can help you gather the necessary evidence to explain the situation. In some cases, you might be able to reverse the transaction. This could involve returning a large purchase or paying down a balance to restore your Debt-to-Income ratio. If the transaction stands, your navigator will re-calculate your DTI to ensure the loan still meets the flight requirements for a Purchase Mortgage.

Writing an Effective Letter of Explanation

An underwriter isn’t looking for a long story. They want facts and documentation. A Letter of Explanation (LOE) should be brief and directly address the why behind any financial anomaly. If you had an emergency car repair that required a credit card swipe, explain it clearly and provide the receipt. A sample sentence for an LOE might look like this: “The deposit on June 1st was a tax refund, as evidenced by the attached IRS document.” This provides the underwriter with the paper trail they need to clear the red flag and keep your application moving forward.

When a “Go-Around” is Necessary

Sometimes a mistake requires more than a simple letter. If a new debt significantly impacts your profile, you might need a go-around, which is a temporary delay to stabilize your finances. This might mean requesting a 30-day extension from the seller in Kalamazoo or Portage. While a delay is stressful, it is far better than a flat denial. Your local navigator plays a crucial role here. They negotiate with the underwriter and provide the human element that automated systems often miss. By being proactive and transparent, you can often save a flight that seemed destined for a crash landing.

Partnering with a Local Navigator in Kalamazoo and Portage

Navigating the final stretch of purchase mortgages in Kalamazoo requires more than just following a generic checklist of what not to do while your mortgage is in underwriting. It requires a guide who understands the specific currents of the Southwest Michigan real estate market. When you work with a local expert, you aren’t just a file number in a distant server; you’re a neighbor whose success matters to our community. Local expertise is the mechanical advantage that provides stability when the winds of the market shift unexpectedly.

The “Jeremy Drobeck Difference” is built on the promise of being present from pre-flight to touchdown. While national lenders might leave you in a holding pattern, we provide direct communication and expert guidance during the high-stakes final 72 hours. Treadstone Mortgage monitors current mortgage rates in Kalamazoo to protect your interest rate lock, ensuring your financial profile remains optimized for the best possible outcome. This end-to-end support is what separates a stressful transaction from a celebratory milestone.

Kalamazoo-Specific Market Dynamics

Local market knowledge is essential for a timely landing. The appraisal market in Portage and Kalamazoo has its own rhythm, and a lender who understands these local timelines can prevent delays before they even start. We maintain deep, long-standing relationships with Southwest Michigan title companies, which streamlines the exchange of legal documents and speeds up the final verification process. Having a navigator who can effectively “walk into the underwriter’s office” to clarify a complex detail ensures that minor questions don’t turn into major grounding events. This level of personalized care provides a steady hand when the automated systems of national lenders might otherwise trigger a generic rejection. Understanding what not to do while your mortgage is in underwriting is the first step, but local advocacy is the final piece of the puzzle.

Final Checklist for Your Closing Day

As you prepare for the final walk-through of your Michigan home, pay close attention to seasonal issues like winter-related pipe damage or roof ice dams that may have occurred since the initial inspection. This is your last chance to ensure the property condition matches the underwriter’s expectations before the title is transferred. Additionally, we’ll have a critical “Wire Transfer” safety talk to protect you from the rising threat of mortgage fraud. Never send funds based on an email without verbal confirmation from a trusted source. Our team is here to ensure every detail is engineered for your safety. Ready for a smooth landing? Contact Jeremy Drobeck today to start your homebuying journey.

Clear Skies Ahead: Finalizing Your Flight Plan for Success

The journey from application to closing is a precision maneuver that requires a steady hand and a disciplined financial approach. By maintaining total stability and mastering what not to do while your mortgage is in underwriting, you protect your investment from the sudden turbulence of credit shifts or undocumented deposits. Whether you’re utilizing MSHDA assistance or a complex renovation loan, your primary objective is to keep your financial profile frozen until the keys are in your hand. Stability isn’t just a goal; it’s the mechanical requirement for a successful touchdown.

With over 20 years of local Kalamazoo lending expertise, our team provides the specialized navigation you need to reach the closing table with confidence. We offer direct access to your Loan Officer throughout the entire process, ensuring you’re never left in a holding pattern. We specialize in the nuances of MSHDA and renovation mortgages, providing the individualized care your milestone deserves. Secure Your Michigan Home Loan with Expert Guidance. Your dream home is just over the horizon, and we’re ready to help you make a perfect landing.

Frequently Asked Questions

Can I buy a new car while my mortgage is in underwriting?

No, you should avoid all major purchases until the keys are in your hand. Buying a new car introduces a significant monthly payment that alters your debt-to-income ratio. This can disqualify you from your purchase mortgage even if you’ve already received a conditional approval. Wait until after the touchdown at the closing table to visit the dealership.

What happens if I lose my job while my loan is in underwriting?

Losing your job is a significant event that requires immediate disclosure to your Loan Officer. Since underwriters perform a Verification of Employment within 72 hours of funding, they will discover the change in status. While it’s a difficult situation, we can help you evaluate if a co-signer or a different loan program can keep your home purchase on track.

Is it okay to move money between my savings and checking accounts?

Moving funds between your own accounts is acceptable, but you must maintain a clear paper trail for every transfer. Underwriters look for stability, and frequent large transfers can appear like you’re trying to hide debt or season “mattress money.” Always keep your bank statements ready to show the origin and destination of every dollar.

How much can I spend on my credit cards during the mortgage process?

You should keep your credit card spending to a minimum and avoid any large, unusual purchases. Increasing your credit utilization can lower your credit score during the final refresh, potentially moving you into a higher interest rate tier. As a rule of thumb, don’t let your balances exceed what they were at the time of your initial application.

Does the underwriter check my credit score again before closing?

Yes, the underwriter will perform a refresh credit pull shortly before your closing date. This is a standard part of the flight plan to ensure no new debts have been opened. This is a primary reason why knowing what not to do while your mortgage is in underwriting is so critical for a smooth landing.

Can I use gift money for my down payment if it arrives late?

You can use gift money for your down payment, but it requires a certified gift letter and proof of the transfer. If the funds arrive late in the process, the underwriter will need to verify the source and ensure the money is truly a gift and not a loan. It’s best to have these funds seasoned in your account well before the final descent.

What is a Letter of Explanation and why does the underwriter want one?

A Letter of Explanation is a factual document that provides context for specific items in your financial file. Underwriters use these letters to understand anomalies like a one-time large deposit or a recent address change. Keep your letter brief and attach supporting documents, such as a tax refund receipt or a bill of sale, to provide the necessary lift for your approval.

How long does the final underwriting stage typically take in Michigan?

In the current 2026 market, the average time to close a purchase mortgage is approximately 50 days. The final underwriting stage, where the “Clear to Close” is issued, typically occurs in the last week of the process. Working with a local navigator in Kalamazoo can help streamline these timelines by ensuring all documents are engineered for a quick review. Knowing what not to do while your mortgage is in underwriting helps prevent unnecessary delays during this home stretch.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”