Bad Credit Home Loans in Portage, MI: Your 2026 Mortgage Flight Plan

What if your credit score wasn’t a “No-Fly Zone,” but simply a flight path that requires a more experienced navigator? It’s exhausting to watch Portage home prices climb toward a $310,000 median while you’re stuck paying high rent because you’re afraid a big bank will laugh at your financial history. You don’t have to stay grounded. It’s entirely possible to secure bad credit home loans Portage MI even if your financial record has seen some recent turbulence.

We understand that a low score doesn’t define your future as a homeowner. You deserve a clear roadmap that replaces anxiety with expert guidance and neighborly respect. This 2026 mortgage flight plan will show you exactly how to qualify for flexible programs like FHA or VA loans. We’ll also explore how to secure up to $10,000 in MSHDA down payment assistance to help you achieve lift-off in the competitive Michigan market. By the time you finish reading, you’ll have the technical knowledge and the confidence to move from the terminal to the cockpit of your new home.

Key Takeaways

- Learn the specific 2026 credit score benchmarks for FHA, VA, and USDA loans to understand where your standing fits on the eligibility spectrum.

- Discover why FHA and VA programs serve as the primary engines for bad credit home loans Portage MI, offering flexible terms that traditional big-box banks often overlook.

- Implement a 90-day “Pre-Flight” strategy to optimize your credit profile and clear the runway for a smoother mortgage approval.

- Unlock up to $10,000 in down payment assistance through MSHDA programs, providing the essential lift needed to bridge the gap between renting and owning.

- Understand the power of manual underwriting and why a local Portage navigator is the key to bypassing automated rejections from national lenders.

Defining “Bad Credit” for a Portage Home Loan in 2026

Many Portage residents assume a single three-digit number locks the cockpit door forever. In reality, “bad credit” isn’t a fixed destination; it’s a spectrum of data points that change over time. Whether you have a “thin” file with very little history or a score bruised by past financial turbulence, your path to homeownership remains open. Finding bad credit home loans Portage MI doesn’t have to feel like flying blind. We view your current financial status not as a rejection, but as the starting point for your personalized mortgage flight plan.

The Credit Score Tiers: Where Do You Stand?

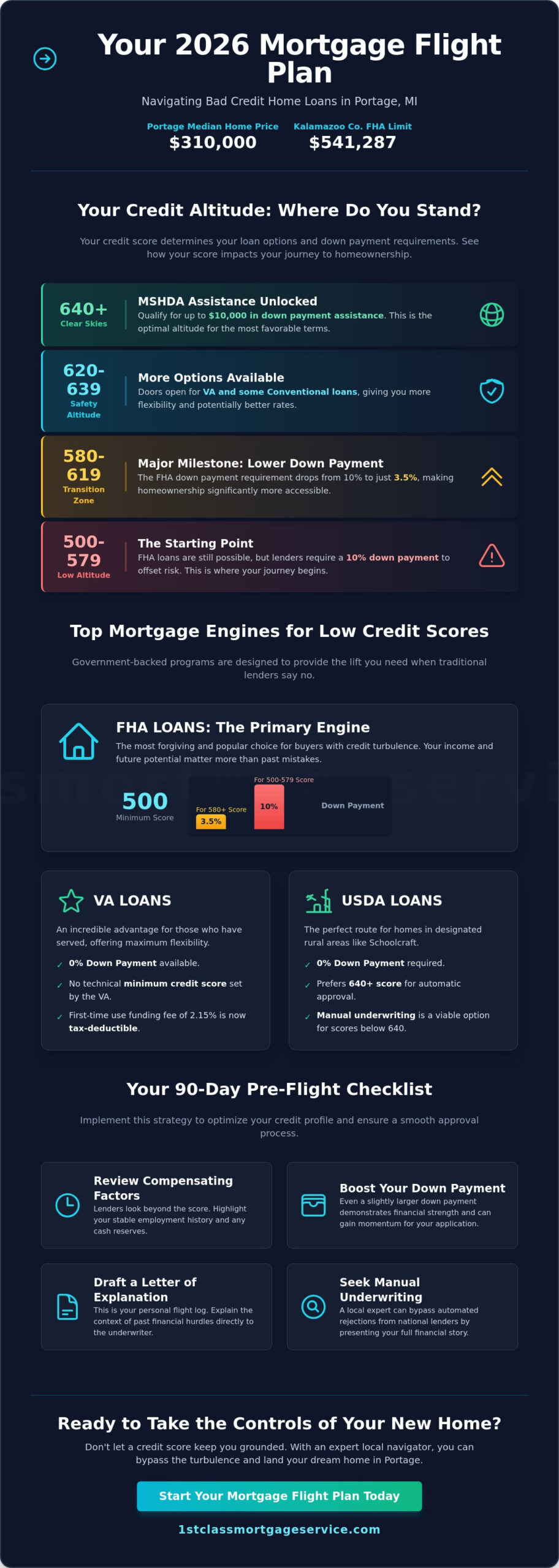

Your eligibility for bad credit home loans Portage MI depends heavily on which tier your score occupies. While different programs have unique requirements, the 2026 benchmarks provide a clear map for your journey. Understanding standard credit score ranges is the first step in determining your current altitude and selecting the right loan engine.

- 500 to 579: This is the “Low Altitude” zone. You may still qualify for an FHA mortgage, but lenders typically require a 10% down payment to offset the risk.

- 580 to 619: This is the “Transition” zone. At 580, you unlock the ability to put just 3.5% down on an FHA loan, which is a major milestone for many buyers.

- 620 to 639: This is often considered the “Safety Altitude” for many West Michigan lenders, opening doors to conventional options and VA mortgages for eligible veterans.

- 640 and Above: This is the “Clear Skies” zone required for MSHDA Down Payment Assistance, providing up to $10,000 in support for those who qualify.

Why Portage Lenders Look Beyond the Number

Local experts in Portage look at the story behind the data. They understand that a low score caused by a one-time medical emergency is different from a chronic history of missed payments. Lenders often look for “compensating factors” that provide extra stability to your application. This might include a long history of stable employment with a major Kalamazoo employer or significant cash reserves in the bank. These factors act like stabilizers on an aircraft, keeping the loan steady even when the credit score isn’t perfect.

If your score is on the lower end, a larger down payment can act as a powerful way to gain momentum. Additionally, a well-written Letter of Explanation serves as your personal flight log. It allows you to explain the context of past financial hurdles directly to the underwriter. When you combine these factors with the 2026 FHA loan limit of $541,287 for Kalamazoo County, the dream of owning a home in Portage becomes a tangible reality. We’re here to help you navigate these nuances and keep your journey on track from taxi to touchdown.

Top Mortgage Programs for Low Credit Scores in West Michigan

Finding the right mechanical components for your financial journey makes all the difference when you’re starting with a lower credit score. You aren’t limited to a single path; instead, several government-backed engines are designed to provide the lift you need. Whether you’re looking for bad credit home loans Portage MI or exploring specialized programs for veterans, understanding these options helps you choose the most stable flight path for your family’s future.

FHA Loans: The 500-580 Score Opportunity

The FHA mortgage is often the first choice for buyers whose credit has faced some turbulence. If your score sits between 500 and 579, you can still secure a loan, provided you can bring a 10% down payment to the table. Once you cross the 580 threshold, the requirement drops significantly to just 3.5% down. This flexibility is why FHA is the most forgiving government-backed engine. It allows you to focus on your steady income and future potential rather than just your past mistakes.

VA and USDA: Specialized Lift for Qualified Buyers

For those who have served, a VA mortgage offers an incredible advantage because the Department of Veterans Affairs doesn’t actually set a technical minimum credit score. This allows for much more flexible navigation during the approval process. Keep in mind that as of 2026, the VA funding fee for first-time use with 0% down is 2.15%, and it’s now tax-deductible. If you’re looking toward the outskirts of the city, such as Schoolcraft or more rural parts of Kalamazoo County, a USDA mortgage might be your best bet. While they often prefer a 640 score for automatic approval, manual underwriting is still a viable route for those with slightly lower scores who want a zero-down payment option.

Renovation Loans: Buying the “Diamond in the Rough”

Sometimes the best way to enter the Portage market with a lower credit score is to look for a property that others might overlook. An FHA 203(k) renovation mortgage allows you to bundle the purchase price and the cost of repairs into one single loan. This is a strategic move for low-credit buyers because it often reduces competition from other purchasers who only want move-in-ready homes. You can find more details on how to manage this process in our Renovation Mortgage Guide. A local navigator can help you determine which of these real estate loans best suits your specific scenario, ensuring you don’t stay grounded just because of a few credit hurdles.

Navigating the Turbulence: Your Flight Path to Credit Approval

Securing a mortgage isn’t just about having a high enough score; it’s about the technical preparation of your financial profile. Think of this phase as your 90-day pre-flight inspection. Even if you’re seeking bad credit home loans Portage MI, a few strategic adjustments to your credit “mechanics” can significantly improve your chances of approval. You don’t need a perfect record to fly, but you do need an aircraft that’s airworthy and a navigator who knows how to bypass the storm clouds of automated rejection.

Step 1: The Credit Audit

Most Portage buyers start by checking free apps, but those often use VantageScore models that differ from what lenders actually see. You need to pull your mortgage-specific FICO scores to see your true altitude. During this audit, we look for the “big three” errors: incorrect addresses, unauthorized inquiries, and outdated balances that haven’t been updated by creditors. A recent late payment within the last 12 months creates much more turbulence than an old collection from five years ago. Identifying these discrepancies early allows us to file disputes before they ground your application.

Step 2: Strategic Debt Reduction

Your credit utilization acts like the weight of your cargo. If your credit cards are maxed out, your score will struggle to gain lift. We recommend the “30% Rule,” where you keep balances below 30% of your total limit. For example, if you have a $1,000 limit on a card, try to keep the balance under $300. It’s also vital that you don’t close old accounts right now. Closing an account might seem like “cleaning up,” but it actually shortens your credit history and can cause your score to drop unexpectedly. When handling collections, we focus on “pay for delete” strategies that resolve the debt without resetting the clock on old negative marks.

Step 3: The Rapid Rescore

If we identify a specific error or a balance that needs updating, we don’t have to wait 30 to 45 days for the bureaus to catch up. A Rapid Rescore is a high-speed navigational correction that your mortgage broker initiates directly with the credit bureaus. By providing proof of a balance paid down or an error corrected, we can often see a score jump of 20 or more points in just three to five business days. This tool is often the difference between a “denied” and a “cleared for takeoff” status. It allows you to move quickly in a competitive market where Portage homes stay on the market for an average of just 15 days.

Managing your Debt-to-Income (DTI) ratio is equally important. With 30-year fixed rates sitting around 6.45% as of May 2026, every dollar of monthly debt affects how much home you can afford. By lowering your monthly obligations while optimizing your score, you create a more stable profile that manual underwriters respect. We stay by your side throughout this entire maintenance process, ensuring your file is flight-ready before we submit it for a final decision.

MSHDA: The “Lift” Needed for Low-Credit Buyers in Portage

While fixing your credit mechanics provides the stability you need, sometimes you require additional thrust to get your homeownership goals off the ground. This is where the Michigan State Housing Development Authority (MSHDA) acts as your ultimate co-pilot. For many seeking bad credit home loans Portage MI, the biggest barrier isn’t just the monthly payment; it’s the upfront payload of a down payment. MSHDA programs are engineered to bridge this gap, providing the financial lift necessary to move from a rental agreement to a deed in a competitive seller’s market.

MSHDA Down Payment Assistance Basics

In 2026, the MSHDA MI Home Loan program offers a significant boost of up to $10,000. This assistance functions as a 0% interest, no-monthly-payment second mortgage that you only repay when you sell the home or finish paying off your primary loan. To qualify for this specialized lift in Portage or the wider Kalamazoo County area, you must meet specific household income limits and complete a homebuyer education course. While we discussed FHA’s 580-score requirement earlier, MSHDA requires a slightly higher altitude; you generally need a minimum credit score of 640 to access these funds. You can find a full eligibility checklist and income requirements in our comprehensive MSHDA Guide.

Combining MSHDA with Low-Credit Loans

The most effective strategy for Portage buyers involves pairing MSHDA assistance with an FHA mortgage. Since an FHA loan requires a 3.5% down payment once you hit a 580 score, the $10,000 from MSHDA often covers the entire down payment and a portion of your closing costs. This creates a “Zero Down” path that is much more accessible than traditional conventional financing. It’s a strategic maneuver that allows you to keep your personal savings as a safety reserve for future home maintenance.

Navigating these state-level programs requires a navigator who is specifically certified to handle MSHDA files. National online lenders often lack the local credentials to process these grants, which can lead to a mid-flight rejection. Working with a local expert like Jeremy Drobeck ensures that your application meets both federal lending standards and MSHDA’s specific Michigan requirements. If you’re ready to see if you qualify for this financial boost, we can help you evaluate your eligibility for MSHDA Down Payment Assistance and guide you through every step of the paperwork. We view this not just as a loan application, but as a partnership designed to land you safely in your new Portage home.

Landing Your Dream Home: Why a Local Portage Expert is Essential

National “Big Box” lenders often operate like automated pilots in a storm; the moment conditions become complex, they simply disengage. These large institutions rely on rigid algorithms that trigger an immediate “auto-decline” for anyone with a less-than-perfect credit history. They don’t see the hard work you’ve put into your 90-day pre-flight plan or the stability of your local employment. When you’re searching for bad credit home loans Portage MI, you need a navigator who understands that a computer program can’t measure your character or your true capacity for homeownership. A local expert doesn’t just process a file; they advocate for your future.

The Advantage of Manual Underwriting

Manual underwriting is the human element of the mortgage process. While automated systems might ground your application based on a single data point, a human underwriter reviews your entire flight log. They look at your stable income, your consistent rent history in Portage, and those “compensating factors” we discussed earlier. This human review allows us to justify your ability to pay, even if your score is currently in a lower tier. It’s the difference between being rejected by a machine and being understood by a professional who knows the West Michigan market inside and out. Local knowledge helps us explain why your specific financial situation is a safe bet for a Purchase Mortgage, regardless of past turbulence.

Your Next Steps to Homeownership

We invite you to a “No-Pressure Flight Review” to evaluate your current standing. Jeremy Drobeck and the Treadstone Mortgage team are committed to staying on the flight deck with you until you successfully close on your home. There’s no judgment here, only a disciplined focus on preparation and precision. We’ve helped many families who were told “no” by big banks find a path to success through individualized care and respect. We view the mortgage process as a significant life milestone that requires careful handling and constant availability.

Whether you’re ready to apply now or need a few more months of credit maintenance, we provide the end-to-end support required for a safe landing. You can explore the full journey in our Purchase Mortgage guide. When you’re ready to take the controls, we’re here to ensure your transition to homeownership is smooth, transparent, and successful. Don’t let the fear of a credit score keep you grounded. Your flight path to a new home in Portage starts with a single conversation with a neighbor who truly cares about your success.

Clear the Runway for Your New Portage Home

Your journey toward homeownership in West Michigan doesn’t have to be grounded by past financial turbulence. You now have a 2026 flight plan that utilizes flexible government-backed engines and the powerful lift of MSHDA assistance. Remember that your credit score is a starting point, not a final destination. By focusing on strategic preparation and human-led manual underwriting, you can bypass the automated rejections of national banks. We are here to ensure you have a steady, reliable ally throughout the entire process.

Finding bad credit home loans Portage MI requires a navigator who understands the local landscape. As a MSHDA Certified Lender with deep Portage and Kalamazoo community expertise, Jeremy Drobeck specializes in manual underwriting for complex credit scenarios. We don’t just look at numbers; we look at your ability to succeed. It’s time to stop paying high rent and start building your future in a community you love.

Schedule Your Free Credit Flight Plan with Jeremy Drobeck to begin your pre-flight audit. We’ll stay on the flight deck with you until you’re cleared for touchdown in your new home. Your future as a homeowner is ready for takeoff.

Frequently Asked Questions

What is the minimum credit score for a home loan in Portage, MI in 2026?

In 2026, the minimum score typically required for an FHA loan is 500, though this usually necessitates a 10% down payment. For a lower down payment of 3.5%, most lenders look for a score of at least 580. Conventional loans generally require a 620, while MSHDA programs in West Michigan set their safety altitude at 640 to qualify for down payment assistance.

Can I get a mortgage in Michigan with a 500 credit score?

You can secure a mortgage in Michigan with a 500 credit score by utilizing the FHA program. While many big box banks might decline this flight path, specialized local navigators can process these applications with a 10% down payment. It’s a viable path for those seeking bad credit home loans Portage MI who have stable income but a turbulent credit history.

Does Portage have special programs for first-time buyers with bad credit?

Yes, the Michigan State Housing Development Authority (MSHDA) offers up to $10,000 in down payment assistance for qualified buyers. While this program requires a 640 credit score, it acts as a powerful co-pilot for first-time owners who need extra lift. This assistance can be paired with FHA loans to minimize your out of pocket costs at the closing table.

How long does it take to fix my credit for a mortgage?

Most Portage buyers can see significant improvements in their flight readiness within 30 to 90 days. Using tools like a Rapid Rescore can even update your profile in as little as five business days once errors are corrected or balances are paid down. The duration depends on whether you’re disputing errors or building a thin credit file from scratch.

Will a mortgage application hurt my credit score even more?

A formal mortgage application involves a hard inquiry, which typically results in a minor, temporary dip of about five points. Credit bureaus recognize rate shopping and usually group multiple mortgage inquiries within a 14 day window as a single event. This small adjustment is a necessary part of your pre-flight check and won’t ground your long-term goals.

Can I use a co-signer for a bad credit home loan in Portage?

You can absolutely use a co-signer, often referred to as a non-occupant co-borrower, to help qualify for an FHA loan. This person’s income and credit profile can provide the additional stability needed to secure approval. It’s a common strategy for Portage residents who have the income to manage payments but need a boost to meet technical lending requirements.

What is the difference between a hard pull and a soft pull for mortgages?

A soft pull is a preliminary review that doesn’t affect your score; we often use this for initial pre-qualification. A hard pull is a comprehensive audit required for a formal mortgage commitment and does appear on your credit report. Think of a soft pull as a weather report and a hard pull as the final mechanical inspection before takeoff.

Are interest rates significantly higher for bad credit home loans?

Interest rates are generally higher for lower credit scores because lenders view the increased risk as requiring more financial ballast. While a buyer with a 740 score might see the 6.45% average reported in May 2026, a lower score may result in a higher premium. Securing a home now allows you to refinance later once your credit altitude has improved and market conditions shift.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”