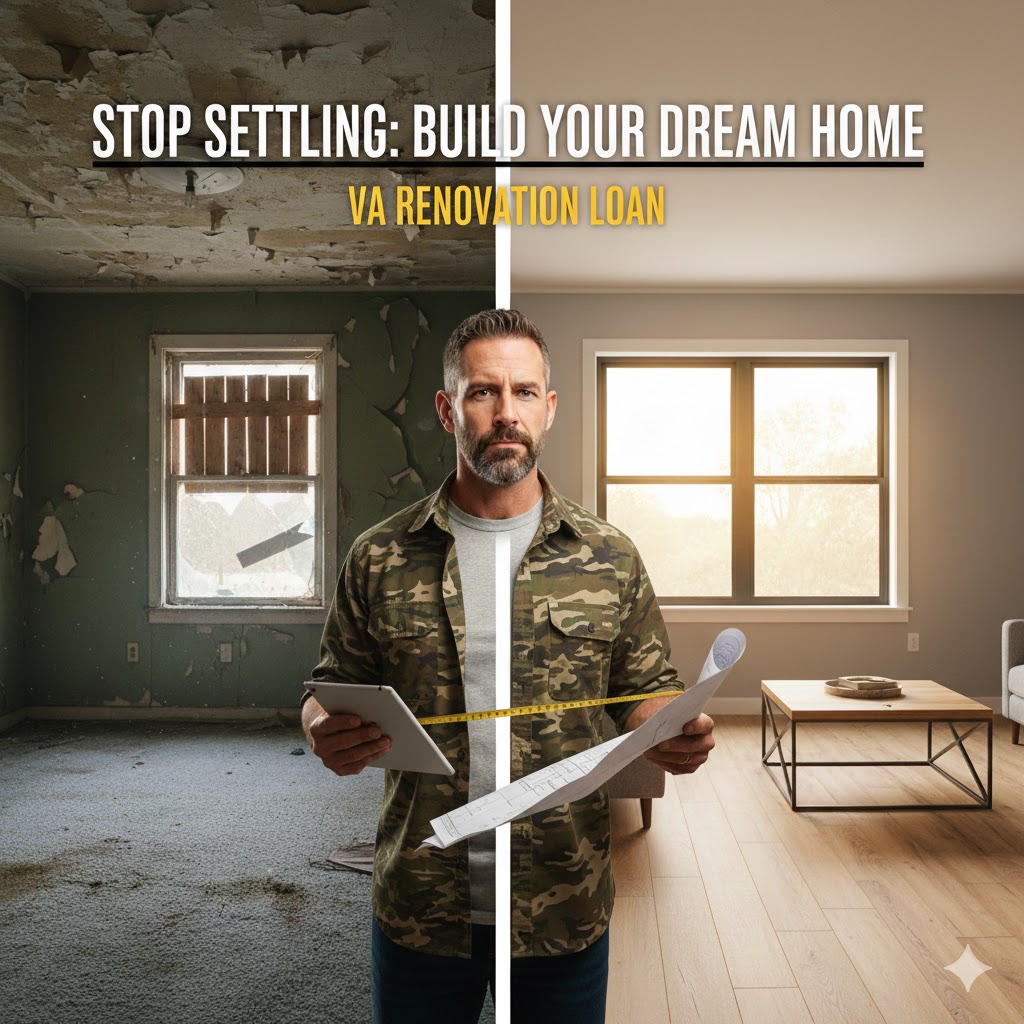

The Veteran’s Hidden Gem: One Loan to Buy and Fix Your Home

Finding the “perfect” home in today’s market is like trying to find a landing strip in a fog bank. It’s tough. You usually have to compromise on the kitchen, the siding, or the floors just to get the keys.

But what if you didn’t have to?

The VA Renovation Loan is the best-kept secret in real estate. It’s not a second mortgage. It’s one loan, one closing, and ZERO DOWN.

1. The “Ugly House” Advantage

Most VA buyers get stuck because of strict appraisal rules. If a house has peeling paint or a broken window, a standard VA loan might get rejected

The Renovation Loan flips the script. Instead of the appraiser looking at the house “as-is,” they look at it “as-completed”.

-

Example: You buy a house for $100k. You have a $30k bid for a new kitchen. The appraiser values the house based on that $130k finished product.

2. What Can You Fix?

The possibilities are almost limitless, as long as it isn’t structural

-

YES: New flooring, windows, HVAC, siding, and kitchens

-

NO: Moving load-bearing walls or jacking up the foundation

-

LIMIT: You can roll up to $75,000 in repairs directly into your loan

3. The Math That Wins

Why use this over an FHA or Conventional loan?

- Zero Down – that’s right the VA renovation loan program allows for no money down

-

NO PMI: You save hundreds every month because veterans don’t pay monthly mortgage insurance

-

LOW RATES: You get the same competitive interest rates as a standard VA loan

-

EQUITY: I’ve seen buyers go “all-in” for $200k on a house that appraises for $250k the day they move in

PRO TIP for Michigan Veterans

If you are a 100% disabled veteran in Michigan, you are EXEMPT from property taxes on your primary residence. Combine that with a $0 down renovation loan, and your monthly “nut” is significantly lower than any neighbor on your block.

Jeremy Drobeck – Mortgage Expert and Marine Corps Veteran is ready to help you finance your dream home. Call today (269) 360-7109 or Get Preapproved Today.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”