Why a Foreclosure Crisis Isn’t on the Horizon

With inflation still lingering and financial strain persisting for many, fears of a looming foreclosure wave are understandable. However, a closer look at the data reveals a different story.

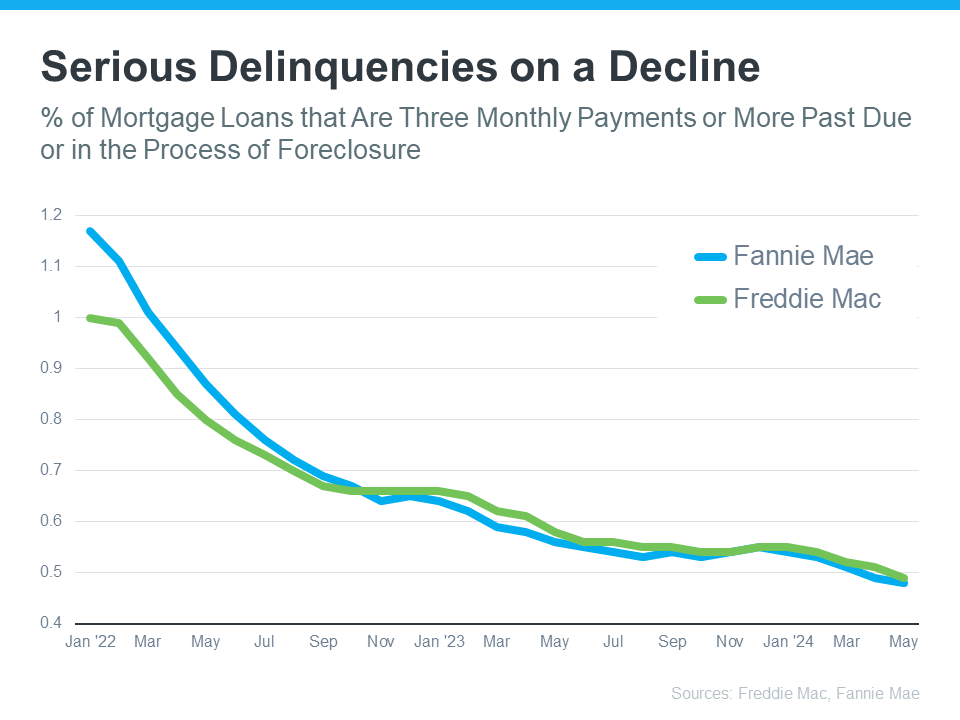

Lenders Are Smarter, Borrowers Are Stronger

The reckless lending practices that fueled the 2008 housing crisis have been significantly tightened. Today’s borrowers are more qualified, with better credit scores and lower debt-to-income ratios. This increased financial stability translates to a lower risk of default.

Data from Freddie Mac and Fannie Mae confirms this trend. The number of homeowners seriously behind on their mortgage payments has been steadily declining. This indicates that borrowers are managing their financial obligations effectively.

Equity: A Safety Net for Homeowners

Another factor working against a foreclosure crisis is the substantial equity homeowners have built up. As Calculated Risk’s Bill McBride points out, this equity provides a cushion for many homeowners, allowing them to sell their homes and avoid foreclosure if needed.

The Bottom Line: No Sign of a Wave

While economic challenges persist, the current housing market landscape is vastly different from the pre-2008 environment. With qualified borrowers and a strong equity cushion, the likelihood of a significant foreclosure surge is minimal.

It’s essential to base our outlook on data and expert analysis rather than fear-driven speculation. The evidence clearly suggests that a foreclosure crisis is not on the horizon.

If you do come across a foreclosure you want to purchase we can absolutely help you finance it. We have a number of different financing options. Just give us a ring (269) 360-7109 or apply online!

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”