Mortgage for Self-Employed in Kalamazoo: Your 2026 Flight Plan to Homeownership

What if the very tax deductions that save your business money are actually grounding your dreams of buying a home in West Michigan? It’s a frustrating paradox many local entrepreneurs face. Your bank account looks healthy, but your net income on paper makes traditional lenders nervous. You’ve likely felt the anxiety of a “big bank” turning you away because they can’t see past a standard tax return. If you’re searching for a mortgage for self-employed Kalamazoo residents, the options often feel limited by rigid systems that don’t value your hard work.

You don’t need a W-2 to secure a competitive rate or a clear path to closing in Portage or Kalamazoo. We understand that your financial story is more complex than a single line on a tax form. This 2026 flight plan reveals how specialized loan programs, such as bank statement loans or USDA options for eligible rural areas, provide the necessary lift. We’ll demystify the paperwork trail and show you how to navigate the current 6.375% to 6.63% rate environment with confidence. From calculating true qualifying income to leveraging MSHDA assistance, you’re about to discover a controlled, expert-led route to your new front door.

Key Takeaways

- Understand the “Tax Return Paradox” and how to accurately calculate your qualifying income without letting business deductions ground your application.

- Compare diverse loan options, including bank statement programs and the standard Conventional Mortgage, to identify the most efficient vehicle for your home purchase.

- Master the documentation process by preparing a precise checklist of tax returns and profit and loss statements required for a successful takeoff.

- Secure a clear path to closing by working with a local navigator who understands the specific requirements of a mortgage for self-employed Kalamazoo business owners.

- Learn how to transform the complex paperwork of entrepreneurship into a streamlined, professional application that local lenders respect.

Navigating the Self-Employed Mortgage Landscape in Kalamazoo

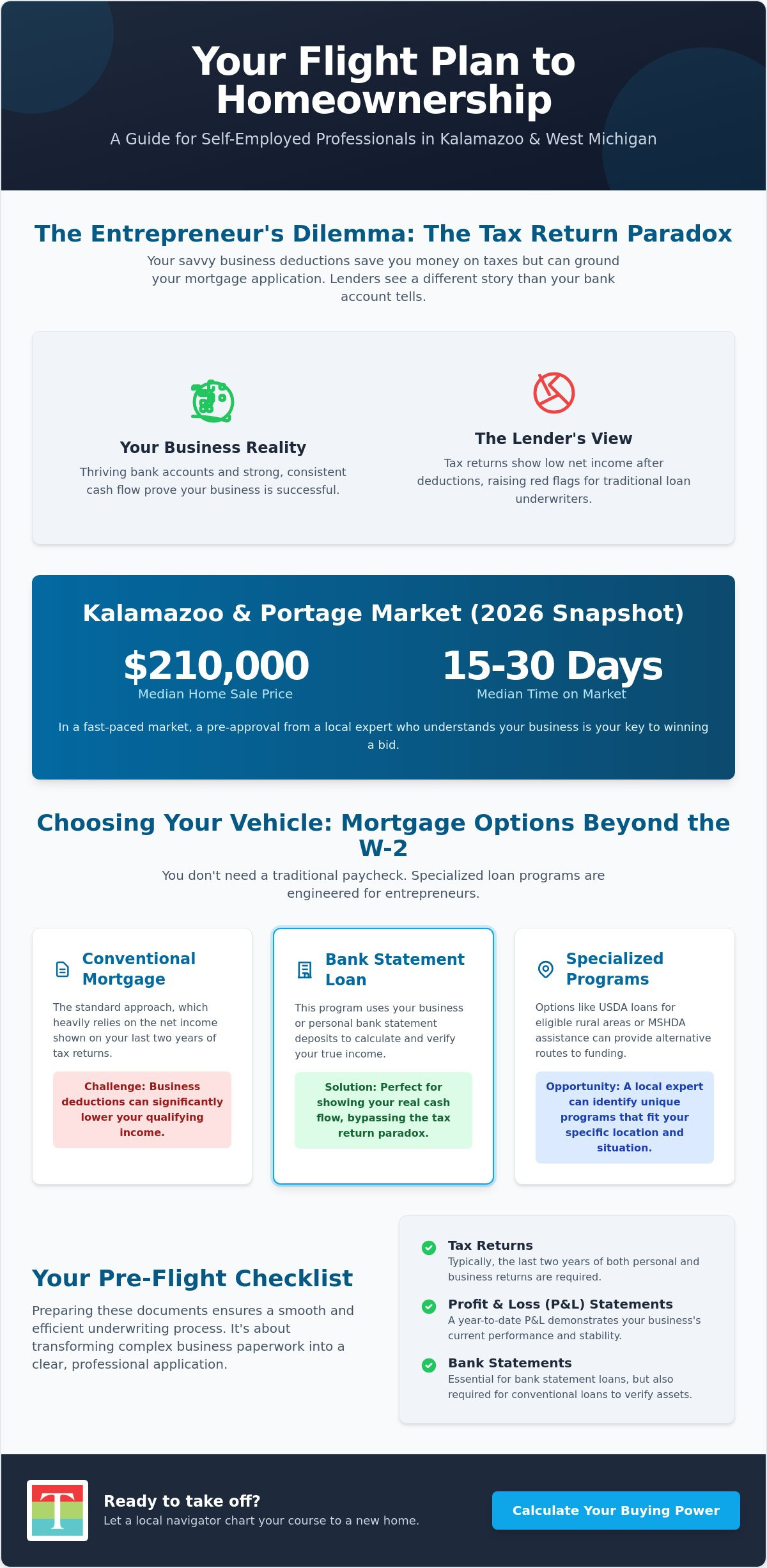

A self-employed mortgage isn’t a different financial species. It’s simply a mortgage engineered for the unique mechanics of business ownership. While a standard employee presents a steady W-2, your income might look like a flight path with significant turbulence on paper. Traditional lenders often give entrepreneurs the “side-eye” because they value predictable, flat-line stability over the dynamic growth of a local business. They often view business deductions as losses rather than savvy management, which can lead to a sudden drop in your perceived borrowing power. In the 2026 Kalamazoo market, where the median home sale price reached $210,000 in May, you can’t afford a lender who doesn’t understand your P&L. You need a navigator who views your business success as the fuel for your home equity, not a liability.

Securing a mortgage for self-employed Kalamazoo residents requires a shift from a transactional mindset to a partnership. Nearly 15% of homeowners across the country are self-employed, yet the industry still treats these borrowers as unconventional. Our approach replaces that cold, automated rejection with expert guidance. We help you translate your entrepreneurial success into a language that underwriters respect, ensuring your “flight plan” to homeownership is cleared for takeoff before you even step foot in a showing.

The Myth of the ‘W-2 Requirement’

You don’t need a traditional paycheck to buy a home in West Michigan. That’s a common misconception that keeps many talented entrepreneurs grounded in the rental market. While big banks typically demand a rigid two-year history of self-employment, there’s more flexibility than you might think. For instance, if you have one year of business ownership but a solid history of W-2 experience in the same field, your path to a loan might still be open. Jeremy Drobeck focuses on the underlying stability of your enterprise. We look at the trajectory of your business, ensuring your Purchase Mortgage is built on a solid foundation of real-world earnings, not just the bottom line of a tax return designed to minimize your tax burden.

Kalamazoo Market Dynamics for Entrepreneurs

The 2026 housing climate in Portage and Kalamazoo is fast-paced and lean on inventory. With homes selling in a median of 15 to 30 days, your pre-approval needs to be more than a piece of paper; it needs to be a flight-ready certification. Self-employed buyers often face extra scrutiny during the offer stage because sellers fear your financing might stall out during underwriting. By securing a mortgage for self-employed Kalamazoo residents through a local expert, you signal to sellers that your income has already been vetted by someone who knows the West Michigan business landscape. This local expertise provides the “lift” needed to win in a competitive seller’s market, giving you the same momentum as a buyer with a standard salary.

Decoding Income: How Lenders View Your Business Earnings

The “Tax Return Paradox” is a common hurdle for entrepreneurs in West Michigan. You’ve spent years working with your CPA to legally minimize your tax liability through deductions, which is excellent for your business’s cash flow. However, when you apply for a mortgage for self-employed Kalamazoo residents, that same strategy can backfire. Lenders typically focus on your net income, the figure left over after all those deductions are taken out. If your paper income looks too low, your loan application might fail to gain the necessary altitude, even if your bank account is thriving.

Stability and continuity serve as the two primary engines that keep your application airborne. Underwriters aren’t just looking at a single snapshot of your success; they’re looking for a consistent flight path over the last two years. For many local business owners in tourism or construction, seasonal income is a reality. We handle this by averaging your earnings over a 24-month period to smooth out the seasonal dips and peaks. This ensures the lender sees a reliable trend rather than a series of erratic maneuvers. If you’re ready to see how your specific earnings translate to buying power, our team can help you review your Purchase Mortgage eligibility today.

The Impact of Business Deductions

Not every deduction on your tax return is treated as a loss by a savvy lender. We look for specific items that can be restored to your total. Add-backs serve as the mechanical lift for your qualifying income by accounting for non-cash expenses that don’t impact your actual liquidity. For example, depreciation on a fleet of vehicles or one-time equipment purchases can often be added back to your bottom line. When we calculate your debt-to-income (DTI) ratio, we typically aim for a target below 45% for conventional loans or 43% for FHA options. This precision ensures you have enough runway to manage both your business expenses and your new home payment comfortably.

Verifying the ‘Flight Path’ of Your Business

In 2026, a year-to-date Profit and Loss (P&L) statement is a critical component of the documentation checklist. It proves to the lender that your business hasn’t stalled since your last tax filing. Whether you operate as an S-Corp, a partnership, or a simple LLC, Jeremy Drobeck specializes in navigating these complex tax structures to find every available dollar of qualifying income. We prioritize the long-term health and stability of your enterprise over a single “peak” month. This disciplined review process ensures that when you find that perfect home in Kalamazoo, your financing is already engineered for a smooth landing and a successful closing.

Choosing Your Vehicle: Mortgage Options for Michigan Entrepreneurs

Selecting the right loan program is like choosing the correct aircraft for a specific mission; the “one-size-fits-all” approach rarely works for business owners. If your tax returns are clean and show strong net income, a Conventional Mortgage is often the most efficient path. These standard loans allow for down payments as low as 3% to 5% for qualifying buyers. However, many business owners find better lift through government-backed options. For 2026, the FHA loan limit in Kalamazoo County is $541,287, requiring only a 3.5% down payment for those with a credit score of 580 or higher. Veterans can access VA Mortgages with 0% down and no loan limits for full entitlement. Securing a mortgage for self-employed Kalamazoo residents often involves looking beyond the standard big-bank offerings to find programs that reward your business’s actual performance.

Bank Statement Loans vs. Traditional Mortgages

For entrepreneurs whose tax returns don’t reflect their true cash flow due to heavy deductions, Bank Statement Loans provide an alternative flight path. These “Non-QM” programs look at your actual deposits over a 12 or 24-month period rather than your net tax figures. While the interest rates are typically higher than conventional options, they offer the flexibility needed when traditional documentation fails to provide enough lift. If your goal is expanding a portfolio rather than a primary residence, a DSCR loan allows you to qualify based on the property’s projected rental income. This is a game-changer for local investors navigating the mortgage for self-employed Kalamazoo market, as it bypasses personal income verification entirely.

Leveraging MSHDA as a Self-Employed Buyer

Many entrepreneurs assume they are ineligible for assistance programs, but Michigan first time home buyer programs like MSHDA are accessible to the self-employed. MSHDA Down Payment Assistance can provide a significant boost, helping you preserve your business capital while still securing a home. In Portage and Battle Creek, eligibility depends on meeting specific income and purchase price limits, but the program is designed to lower the barrier to entry. We help you navigate the nuances of qualifying with non-traditional income, ensuring you have the maximum momentum possible at the closing table. This local support acts as a stabilizer, providing the extra help needed to transition from successful business owner to confident homeowner.

Preparing for Takeoff: Your Self-Employed Documentation Checklist

Before any aircraft leaves the ground, the pilot performs a rigorous pre-flight inspection to ensure every system is functioning perfectly. Your home loan application requires the same level of precision. While a W-2 employee might only need a few paystubs to clear for takeoff, securing a mortgage for self-employed Kalamazoo residents involves assembling a more comprehensive flight log. This documentation serves as the engineering proof that your business is a stable, income-generating machine capable of supporting a long-term financial commitment. Underwriters don’t just want to see that you’re making money; they want to see the consistency of your business’s trajectory over time.

To ensure your application has the necessary lift, you’ll need to gather several key documents. This isn’t just about satisfying a checklist; it’s about providing a transparent view of your financial health. You should be prepared to provide:

- Two years of personal and business tax returns: Include every schedule and attachment to give a full picture of your earnings.

- Year-to-date (YTD) Profit and Loss statement: This proves your business remains on a steady course since your last tax filing.

- Balance Sheet: This document outlines your business assets and liabilities, providing a snapshot of your enterprise’s overall strength.

- Bank statements: Both personal and business statements from the last 12 to 24 months are typically required to verify cash flow.

- Proof of business existence: This can include professional licenses, business insurance, or a formal letter from your CPA.

If you’re ready to begin your pre-flight check and see which programs fit your unique situation, you can start your Purchase Mortgage application today with our local team.

The ‘Business Narrative’ Document

Numbers tell a story, but they don’t always capture the full context of your entrepreneurial journey. A business narrative acts as the flight manual for your underwriter, explaining the “why” behind the data points. If you had a one-off expense, such as a major equipment upgrade or a rebranding effort, this is your opportunity to explain how that investment stabilized your future growth. Highlighting your industry experience in the West Michigan market shows that you aren’t just a business owner; you’re a seasoned professional with deep roots in the community. This narrative provides the emotional and logical “lift” needed to clear hurdles that might otherwise ground a less-prepared application.

Credit and Asset Management

The golden rule for 2026 is simple: keep your personal and business finances in separate cabins. Co-mingling funds creates unnecessary turbulence during the audit process and makes it significantly harder for a lender to verify your true qualifying income. You should also monitor your credit score closely to ensure a smooth flight during underwriting. While a mortgage for self-employed Kalamazoo buyers can be secured with various scores, a higher number typically unlocks more competitive rates. Finally, remember the “seasoning” requirement for your down payment. Lenders generally want to see that large deposits have been in your account for at least 60 days to ensure the funds are stable and sourced correctly.

Jeremy Drobeck: Your Local Mortgage Navigator in Kalamazoo

When you call a national mortgage factory, you’re often treated as a data point in a vast, rigid algorithm. For a business owner, this is where the journey to homeownership often stalls. These distant lenders don’t understand the seasonal flow of a West Michigan landscaping company or the complex reinvestment strategies of a local tech startup. Jeremy Drobeck serves as your local navigator, providing the specialized care required for a mortgage for self-employed Kalamazoo entrepreneurs. Working with Treadstone Mortgage means having a steady, reliable ally who is present throughout the entire duration of the process. We don’t just process files; we engineer solutions that provide the necessary lift for your specific financial situation. Choosing a local expert ensures that your business success is recognized as a strength, not a hurdle.

The Treadstone Mortgage commitment is built on end-to-end support. We view the mortgage process as a significant life milestone that requires careful handling and empathy. Our team takes the time to build a personalized flight plan that reflects your unique business model. Whether you’re looking to close on a home in Portage or find a quiet corner in Kalamazoo County, we provide the expert guidance needed to lower high-stress barriers. We replace the cold, transactional feel of big banks with a partnership based on individualized care and respect.

Personalized Guidance for Complex Scenarios

Business structures aren’t always straightforward. You might be juggling multiple K-1s, managing an S-Corp, or navigating a partnership with complex corporate layers. Jeremy’s experience with Kalamazoo’s diverse industrial base, from medical manufacturing to local retail, allows him to interpret these structures with precision. We replace the anxiety of the unknown with transparent, direct communication. By understanding the mechanical components of your business, we can tailor a Purchase Mortgage that aligns with your long-term goals. This isn’t a standard application; it’s a customized strategy designed to handle unconventional scenarios with technical proficiency.

Ready for Takeoff? Contact Jeremy Drobeck Today

The first step toward your new home is a simple discovery call. Think of this as your pre-flight check. During this initial conversation, we assess your goals and review the flight path ahead. To prepare for your first meeting in Kalamazoo or Portage, gather the documentation checklist we discussed earlier, including your last two years of tax returns and your current YTD Profit and Loss statement. Having these ready ensures a smooth departure from the very start. Your dream home is within reach, even without a traditional W-2 paycheck. With the right preparation and an experienced guide at your side, you can move forward with total confidence in your financial future. Let’s get your homeownership dreams off the ground today.

Clear Your Path to a West Michigan Closing

You’ve built a successful business through discipline and vision. Now, it’s time to apply that same precision to your homeownership journey. By mastering your documentation checklist and choosing a loan vehicle tailored to your actual cash flow, you’ve already cleared the most difficult part of the flight path. Whether you’re leveraging bank statement programs or tapping into MSHDA assistance, your entrepreneurial status is a powerful engine for building long-term equity. Finding a mortgage for self-employed Kalamazoo residents doesn’t have to be a solo mission through heavy turbulence.

Jeremy Drobeck brings over 20 years of local market experience to your side, offering the personalized Treadstone Mortgage service you deserve. As an expert in both MSHDA and Non-QM loans, he’s ready to engineer a solution that fits your specific corporate structure. Your dream home in Portage or Battle Creek is closer than you think. Schedule your Self-Employed Mortgage Flight Plan with Jeremy Drobeck and take the first step toward a successful landing. Your future front door is waiting, and we’re here to guide you every step of the way.

Frequently Asked Questions

Can I get a mortgage if I’ve only been self-employed for one year?

Yes, it’s possible to secure financing with just one year of self-employment if you have a total of two years of experience in the same line of work. While a two-year history is the standard benchmark, lenders can often use your previous W-2 history in the same field to prove your professional stability. We look for a consistent flight path that shows you’ve maintained your expertise and earning potential during the transition to business ownership.

Do lenders use my gross income or my net income after taxes?

Lenders typically focus on your net income, which is the amount remaining after you’ve taken all your business deductions on your tax returns. This can create a challenge when searching for a mortgage for self-employed Kalamazoo residents, as tax-saving strategies often lower your perceived borrowing power. To counter this, we use “add-backs” for non-cash expenses like depreciation, which helps restore your qualifying income and provides the lift needed for your application.

What is a Bank Statement Loan, and is it right for me?

A Bank Statement Loan is an alternative “Non-QM” program that verifies your income using 12 to 24 months of actual bank deposits instead of tax returns. This vehicle is perfect for entrepreneurs with high business write-offs that make their paper income look lower than their actual cash flow. While these loans usually have higher interest rates than a Conventional Mortgage, they offer the flexibility required to get your homeownership goals off the ground when traditional paths are blocked.

Will my business debt count against my personal debt-to-income ratio?

Your business debt won’t necessarily count against your personal DTI if you can prove the business has paid that debt for the last 12 consecutive months. We’ll need to see business bank statements or cancelled checks showing the payments coming directly from your company account. By documenting that the business handles these liabilities, we can keep your personal debt profile clean and maximize your momentum at the closing table.

Are interest rates higher for self-employed borrowers in Michigan?

Interest rates for standard programs like FHA or Conventional loans are generally the same for self-employed borrowers as they are for W-2 employees. You won’t face a higher rate just because you own a business, provided you meet the standard income and credit requirements. However, if you choose a specialized program like a Bank Statement Loan, the rates are typically higher to account for the more flexible documentation and manual underwriting involved.

Can I use MSHDA down payment assistance if I own my own business?

Yes, self-employed individuals are eligible for MSHDA Down Payment Assistance as long as they meet the program’s income and purchase price limits for 2026. This assistance provides a critical boost for business owners who want to keep their liquid capital invested in their company while still buying a home. We help you calculate your qualifying income according to MSHDA’s specific standards to ensure your application remains on a steady course toward approval.

What happens if my business income fluctuated significantly last year?

Lenders usually average your income over a 24-month period to account for the natural peaks and valleys of entrepreneurship. If your income saw a significant decline in the most recent year, it could ground your application, as lenders prioritize a stable or increasing trajectory. We work with you to provide a clear narrative for any fluctuations, ensuring the underwriter understands the mechanics of your business and the stability of your future earnings.

Do I need a CPA-prepared P&L statement to qualify for a loan?

While some programs allow for self-prepared documents, a CPA-prepared Profit and Loss (P&L) statement provides a much higher level of professional authority to your file. It acts as a certified flight log that gives underwriters total confidence in your current year-to-date performance. In a competitive market like Kalamazoo or Portage, having these precisely engineered documents ready can be the difference between a stalled application and a smooth landing at your new home.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”