DSCR Loan vs Traditional Investment Property Loan: A 2026 Michigan Investor’s Guide

What if your personal paycheck wasn’t the engine powering your next Michigan real estate acquisition, but the property itself provided all the necessary lift? Many seasoned investors eventually hit a ceiling where their debt-to-income ratio starts to redline or they reach the frustrating 10-property limit common with conventional financing. It’s a common struggle to watch a prime Grand Rapids or Detroit deal slip away just because a traditional lender is moving at a glacial pace. We understand that as you scale, the paperwork should get lighter, not heavier.

A DSCR loan has zero impact on your personal Debt-to-Income (DTI) ratio because the qualification is based entirely on the property’s performance. This is a primary reason why investors prefer a DSCR loan vs traditional investment property loan Michigan when they want to scale their portfolios. It keeps your personal credit lines clear for other life milestones, such as purchasing a primary residence. For those looking beyond state lines, Padi Goodspeed offers nationwide mortgage expertise to help you navigate these financial decisions with confidence.

This guide explores the critical choice between a DSCR loan vs traditional investment property loan Michigan so you can decide which path offers the smoothest flight for your business. You’ll discover how to leverage property-based income to bypass personal DTI constraints, close deals in record time, and finally move past that 10-property cap. We’ll break down the specific interest rate spreads and Michigan-specific regulations you need to know for 2026, ensuring your portfolio has the clearance it needs to reach new heights.

Key Takeaways

- Learn why traditional financing often hits a “DTI Wall” after 10 properties and how to navigate past these personal income limits to keep your portfolio climbing.

- Understand the mechanics of a DSCR loan vs traditional investment property loan Michigan to determine if your personal credit or the property’s cash flow should take the lead.

- Master the DSCR formula to calculate your property’s “lift ratio,” ensuring your rental income is sufficient to cover debt service without tax return verification.

- Compare interest rates, down payment requirements, and seasoning rules side-by-side to choose the most efficient financing vehicle for your 2026 investment strategy.

- Discover how to engineer long-term growth through LLC borrowing and asset-based qualification, protecting your personal finances while scaling your Michigan reach.

Navigating Michigan’s Investment Landscape: The DTI Wall vs. Scalability

Every investor starts with a clear sky, but as the portfolio grows, the atmospheric pressure increases. Most Michigan investors begin with a personal-income-based approach. It works for the first few properties. Eventually, you hit the “DTI Wall.” This is the point where your personal debt-to-income ratio, weighed down by your own mortgage or personal debts, prevents you from qualifying for another traditional loan. Even if your rentals are cash-flow positive, the bank’s rigid formula says you’ve reached your ceiling. In the 2026 market, where median home prices in Michigan have stabilized around $285,000, hitting this wall can ground your expansion just when opportunities in Kalamazoo or Portage are peaking.

The Pilot vs. The Aircraft: A New Way to Think About Loans

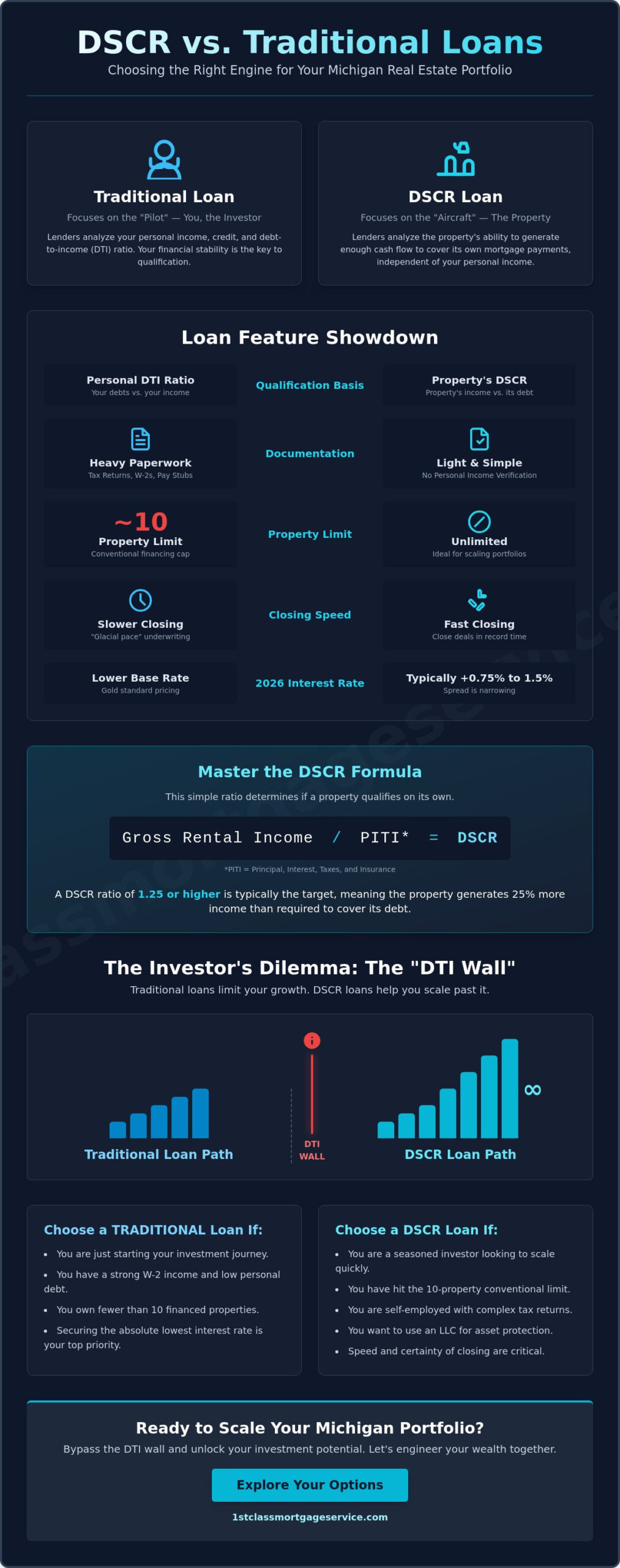

Think of your financing as the engine of your investment vehicle. A traditional loan qualifies the “pilot.” The lender scrutinizes your tax returns and W2s to ensure you can personally handle the financial turbulence. A Debt Service Coverage Ratio (DSCR) loan shifts the focus to the “aircraft.” Instead of looking at your paycheck, the lender looks at the property’s ability to generate enough lift to cover its own debt service. Choosing a DSCR loan vs traditional investment property loan Michigan depends on whether you want the lender to bet on your personal history or the property’s future performance.

When to Pivot from Conventional to DSCR

The pivot to asset-based lending usually happens near the 10-property limit. Conventional guidelines typically cap the number of financed properties you can hold. Beyond this, the documentation requirements become a mountain of tax returns. Many self-employed Michigan investors find these requirements nearly impossible to meet. In West Michigan, where rental demand remains high, waiting for traditional underwriting can mean losing a deal to a faster competitor. DSCR loans offer a faster takeoff. They don’t require personal income verification and prioritize your liquid reserves over your personal debt-to-income ratio.

In 2026, the interest rate spread between these two options has narrowed significantly, often sitting within 0.75% to 1.5%. This makes the move toward property-based qualifying more attractive for those looking to scale quickly. Deciding on a DSCR loan vs traditional investment property loan Michigan requires looking at your long-term flight plan. If you’re just starting, the lower rates of a traditional mortgage might be the right initial boost. But if you’re looking to scale a massive portfolio across the Great Lakes State, you need the flexibility of asset-based qualifying. We’ve seen investors in Kalamazoo and Portage use these tools to bypass the slow traditional process and secure high-demand rentals before the competition can even finish their paperwork. We view this as a strategic engineering of your wealth. We’re here to help you navigate these complex currents and find the path that keeps you in the air.

Traditional Investment Loans: Qualifying the Pilot’s Financial Stability

For many investors, the journey begins with a standard Purchase Mortgage. This path follows the strict flight paths set by Fannie Mae and Freddie Mac, which remain the gold standard for low-rate financing. When you apply for a traditional investment property loan, the lender is primarily concerned with your personal financial stability. Your tax returns serve as the primary flight log, documenting every dollar earned and spent over the last two years. While this scrutiny is intense, it’s designed to ensure the pilot can maintain control even if the investment hits unexpected turbulence.

The impact of personal debt is significant here. Every car payment, student loan, and primary residence mortgage is factored into your debt-to-income (DTI) ratio. In the context of a DSCR loan vs traditional investment property loan Michigan, the traditional route requires you to prove that your personal income can cover all these obligations plus the new rental property’s expenses. If your personal debt load is high, it can ground your acquisition plans before you even reach the appraisal stage.

The Benefits of Conventional Financing

The most compelling reason to choose this path is the cost of fuel. Traditional loans offer the most competitive current mortgage rates. As of June 15, 2026, the average interest rate for a 30-year fixed mortgage in Michigan sits at 6.69%. This long-term stability allows for predictable cash flow over three decades. Additionally, down payment requirements are often more accessible, typically starting around 15% to 25% for single-family rentals, which is often lower than the entry point for commercial-grade products.

The Trade-offs: Documentation and DTI Limits

Underwriting turbulence is the primary trade-off. A traditional loan typically takes 30 to 45 days to close because of the exhaustive documentation required. Lenders will calculate an “all-in” DTI, which can be a major hurdle if you already have a high personal mortgage. Furthermore, conventional guidelines usually require a two-year history of rental income on your tax returns before they will count that income toward your qualification. This “catch-22” often prevents new investors from scaling quickly. If you find the traditional paperwork mountain is slowing your momentum, you might want to explore our specialized investment tools to see if a different engine fits your needs better.

Navigating the DSCR loan vs traditional investment property loan Michigan debate requires an honest look at your financial cockpit. If you have a strong W2 income, low personal debt, and plenty of time, the lower rates of a conventional mortgage provide a solid foundation. However, once you hit the 10-property limit or your DTI begins to redline, it’s time to look at the property’s own lift capacity to keep your portfolio moving forward.

DSCR Loans: Measuring the Property’s Lift and Cash Flow

If the traditional mortgage is a thorough background check on the pilot, the DSCR loan is an inspection of the aircraft’s engines. This financing vehicle ignores your W2s and personal tax returns entirely. Instead, it measures the property’s ability to generate its own lift. By focusing on the income the asset produces rather than your personal debt-to-income ratio, this loan type allows you to bypass the common roadblocks that ground growing portfolios. It’s a shift from personal qualification to asset performance.

One of the most significant advantages when comparing a DSCR loan vs traditional investment property loan Michigan is the ability to close in the name of an LLC. This provides a layer of asset protection that traditional Fannie Mae products often restrict. Because the property is the primary qualifier, there is theoretically no limit to the number of loans you can hold. You aren’t tethered to the 10-property cap that often stalls investors using conventional routes. This scalability is why seasoned investors view property-based financing as the primary engine for long-term growth.

Calculating the Debt Service Coverage Ratio (DSCR)

To determine your lift ratio, lenders use a simple formula: Monthly Rental Income divided by PITI (Principal, Interest, Taxes, and Insurance). To verify the income, an appraiser completes a 1007 Rent Schedule to confirm the market rent for your specific Michigan neighborhood. We generally look for a ratio of 1.0 or higher, meaning the property covers its own weight. The DSCR ratio is the primary metric used to verify that a property is self-sustaining and solvent without relying on the borrower’s personal funds.

The Speed of Execution in Competitive Markets

In fast-moving markets like Battle Creek or Grand Rapids, speed is your greatest asset. Traditional underwriting can feel like a slow taxi on a crowded runway, but DSCR loans can reach takeoff in as little as 21 days. By removing the pilot’s personal financial history from the equation, we eliminate the need for endless paperwork like W2s and tax returns. This streamlined process allows Michigan investors to win deals in low-inventory areas where sellers prioritize a certain and swift closing. When you’re comparing a DSCR loan vs traditional investment property loan Michigan, you’re essentially choosing between qualifying based on your past earnings or the property’s future potential.

We’ve helped countless investors in West Michigan navigate this transition. It’s about more than just a loan; it’s about engineering a portfolio that can withstand market shifts while maintaining steady momentum. By letting the property do the heavy lifting, you’re free to focus on finding the next opportunity rather than managing a mountain of personal documentation.

The Michigan Investor’s Scorecard: Conventional vs. DSCR

Choosing the right financing engine requires a clear view of the scorecard. While we’ve discussed the mechanics of how these loans qualify, the decision often comes down to the numbers on the page. In the 2026 market, the spread between a DSCR loan vs traditional investment property loan Michigan has tightened significantly. Conventional rates for a 30-year fixed mortgage in Michigan are averaging 6.69 percent. Meanwhile, well-qualified DSCR borrowers are seeing rates between 6.12 percent and 7.50 percent. This narrowing gap means the “premium” for property-based qualifying is lower than it’s been in years, making the speed and flexibility of asset-based lending much more attractive.

The most common objection we hear is about those slightly higher interest rates. It’s a fair concern. However, you have to weigh that cost against the “lift” it provides. If a traditional loan takes 45 days to close and requires a mountain of personal paperwork, you might lose a high-yield deal in a competitive area like Grand Rapids. A DSCR loan can close in half that time. For many West Michigan investors, the ability to secure a property quickly and scale beyond the 10-property limit far outweighs a small difference in the monthly payment. It’s about engineering a portfolio for growth, not just finding the absolute lowest rate at the expense of your momentum.

Michigan Market Appraisal Nuances

Appraisals in 2026 require a local touch. In markets like Kalamazoo and Grand Rapids, there’s often a gap between “Actual Rent” (what the current tenant pays) and “Market Rent” (what the property could command today). Traditional lenders often lean on the lower of the two. We focus on the Market Rent verified by the 1007 Rent Schedule. This distinction is vital because it can be the difference between your loan reaching the required 1.0 coverage ratio or falling short. Expect a down payment requirement of 20 to 25 percent for both loan types, though conventional options can sometimes dip to 15 percent for specific single-family scenarios.

LLC vs. Personal Name: The Liability Navigation

Traditional loans almost always require you to close in your personal name. This ties the property directly to your personal credit and liability. For long-term portfolio protection, many Michigan investors prefer closing in an LLC. This provides mechanical stability and separates your personal assets from your business ventures. Jeremy Drobeck specializes in assisting investors as they navigate the legal requirements for Michigan business entities, ensuring your flight plan includes the necessary asset protection. If you’re ready to see how these numbers look for your next deal, you can start your custom loan comparison here to find the most efficient path forward.

The “Local Advantage” cannot be overstated. A national call center doesn’t understand why a duplex in the Vine neighborhood of Kalamazoo commands a different rent than one in Portage. We live and work in these communities. We know the rent comps, the local property managers, and the specific Michigan transfer taxes (0.75 percent state and 0.11 percent county) that impact your closing costs. That local expertise ensures your appraisal is accurate and your loan stays on course from application to closing.

Charting Your Course: Why West Michigan Investors Choose Jeremy Drobeck

Engineering a successful rental portfolio isn’t just about picking a product; it’s about choosing the right navigator. In the complex world of the DSCR loan vs traditional investment property loan Michigan, the technical details can feel overwhelming. That’s where the Treadstone Advantage comes into play. We don’t just process applications; we engineer personalized flight plans designed to help you scale with precision. Whether you’re eyeing a multi-unit in Kalamazoo or a single-family home in Portage, our local expertise provides the mechanical stability your investments require. We tackle the tough questions about rates and ROI head-on, ensuring you have the data to overcome any hesitation before you commit to a new deal.

Our core signature is a commitment to being present throughout the entire duration of your journey. Many national lenders hand you off to a call center once the initial paperwork is signed, leaving you to navigate the turbulence alone. We stay in the cockpit with you. From the first pre-flight check to the final signatures at the closing table, you’ll have a steady, reliable ally who views your success as a significant life milestone. This end-to-end support is what separates a transactional experience from a true partnership, transforming a high-stress financial hurdle into a controlled, professional process.

Expert Guidance for Complex Scenarios

West Michigan’s real estate landscape is diverse, often requiring unconventional solutions that national big-box lenders don’t understand. Short-term rentals, like Airbnbs along the lakeshore or near downtown hubs, have unique income profiles that standard lenders often struggle to underwrite correctly. We understand these nuances and how to present them to underwriters to ensure your loan stays on track. If you find a property with great bones but in need of a mechanical overhaul, we can integrate a Purchase Mortgage with specialized financing. For those looking to add immediate value through renovations, our Renovation Mortgage guide outlines how to finance your dream investment. We believe in transparent communication with no fine print, just clear navigation toward your goals.

Schedule Your Pre-Flight Investment Review

Ready to clear for takeoff? Your first step is a comprehensive pre-flight investment review. During this consultation, we’ll look at your current property details and your long-term scaling goals to ensure your strategy is built on a solid foundation. We won’t just push one product; we analyze both the Conventional and DSCR paths side-by-side to find the highest ROI for your specific situation. This process is designed to lower the high-stress barriers of lending, replacing anxiety with a sense of calm, expert guidance. Bring your property addresses, current rent rolls, and your vision for the future. Contact Jeremy Drobeck to start your investment flight plan today. We’re ready to help you navigate the 2026 Michigan market with confidence and care.

Engineering Your Michigan Portfolio for the Long Haul

Your flight path as a real estate investor is unique, and your financing should reflect your specific goals. We’ve explored how traditional loans scrutinize the pilot’s personal finances while DSCR options focus on the aircraft’s own lift capacity. Deciding between a DSCR loan vs traditional investment property loan Michigan is a strategic choice that determines how quickly you can scale beyond the typical 10-property limit or bypass personal debt hurdles. Whether you need the low rates of a conventional mortgage or the rapid execution of asset-based lending, the right engine makes all the difference in your 2026 strategy.

With over 20 years of local Michigan lending experience, Jeremy Drobeck offers specialized expertise in both conventional and unconventional investment products. As a representative of the Division of Neighborhood Loans, Inc. (NMLS #222982), he provides the transparent, expert guidance you need to navigate even the most complex market conditions. You don’t have to fly solo through the paperwork and underwriting turbulence. We’re committed to being your steady ally from takeoff to landing.

Navigate your next investment with Jeremy Drobeck’s expert mortgage services. The Michigan rental market holds incredible potential for those with the right tools and a clear plan. We’re ready to help you engineer your success and get your next deal off the ground with confidence.

Frequently Asked Questions

Can I get a DSCR loan for my first investment property in Michigan?

Yes, you can secure a DSCR loan for your first Michigan investment property even without prior landlord experience. While some lenders prefer experienced “pilots,” many programs are specifically engineered to help new investors take flight. You will simply need to ensure the property’s projected rental income provides enough lift to meet the required coverage ratio, which is verified through a professional appraisal.

How much higher are DSCR loan interest rates compared to traditional loans in 2026?

In 2026, the interest rate spread between a DSCR loan vs traditional investment property loan Michigan has narrowed to approximately 0.75% to 1.5%. With conventional Michigan rates averaging 6.69%, well-qualified DSCR borrowers can find fixed rates starting around 6.12% for adjustable products or up to 7.50% for 30-year fixed terms. This smaller gap makes property-based qualifying more accessible than in previous years.

Do DSCR loans require a minimum credit score for Michigan borrowers?

Most DSCR programs require a minimum credit score of 620, though a score of 680 or higher typically unlocks the most competitive rates and higher leverage options. Your credit score acts as a certification of your financial reliability. A stronger score allows for a smoother underwriting process and provides more flexibility when navigating complex investment scenarios in competitive markets like Grand Rapids.

Can I use a DSCR loan to buy a multi-family property in Kalamazoo?

Yes, multi-family properties in Kalamazoo or Battle Creek are ideal candidates for DSCR financing. These assets often generate substantial lift because they have multiple rental streams, which makes it easier to satisfy the 1.0 debt service coverage requirement. We frequently use these loans to help investors acquire 2 to 4 unit properties that might otherwise be difficult to qualify for using traditional personal income limits.

What is the maximum Loan-to-Value (LTV) for a Michigan DSCR loan?

The maximum Loan-to-Value for most Michigan DSCR products is 80%, which translates to a 20% down payment. If the property’s cash flow is tighter or if you are looking for a “no-ratio” loan, the LTV may be adjusted to 70% or 75%. This ensures the financing is properly engineered to remain stable even if the local rental market experiences minor turbulence.

How does a DSCR loan impact my personal Debt-to-Income ratio?

A DSCR loan has zero impact on your personal Debt-to-Income (DTI) ratio because the qualification is based entirely on the property’s performance. This is a primary reason why investors prefer a DSCR loan vs traditional investment property loan Michigan when they want to scale their portfolios. It keeps your personal credit lines clear for other life milestones, such as purchasing a primary residence.

Do I need to have a registered LLC to qualify for a DSCR loan in Michigan?

You aren’t always required to have a registered LLC, but many DSCR lenders prefer or even require you to close in a business entity name. Closing as an LLC provides mechanical stability and keeps your personal assets separate from your investment risks. We can help you navigate the specific documentation needed to ensure your Michigan business entity meets all lending requirements for a successful closing.

What happens if the property’s rental income is less than the mortgage payment?

If the rental income doesn’t cover the mortgage payment, you can still qualify through a “low-ratio” or “no-ratio” DSCR program. These specialized tools typically require a larger down payment, often 25% to 30%, to provide additional equity as a safety buffer. It allows you to secure properties in high-appreciation areas where current rents might temporarily lag behind the debt service.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”