Adjustable-Rate vs. Fixed-Rate Mortgage in Michigan: Your 2026 Navigation Guide

Your mortgage isn’t just a financial transaction; it’s a flight plan where your “altitude” is determined by how long you intend to stay in your home. It’s natural to feel a sense of turbulence when looking at the current Michigan market, especially with median home prices sitting near $279,079 and rates remaining a primary concern. You want the reassurance of a steady path, but you might also feel priced out by the standard options. Deciding between an adjustable-rate vs fixed-rate mortgage Michigan requires more than a quick calculation. It demands a clear understanding of how different financial mechanics provide either the lift you need to get started or the stability you need for the long haul.

We believe that expert guidance should replace anxiety with a sense of calm. This guide will help you discover whether a steady fixed-rate cruise or a tactical adjustable-rate path is the right choice for your specific Michigan home purchase. We’ll break down how ARM adjustment caps protect you, why your intended “flight duration” changes your strategy, and how to build a predictable monthly payment you can trust. By the end of this guide, you’ll have a clear decision framework and the confidence to move forward without the fear of overpaying for your journey.

Key Takeaways

- Learn how to evaluate your “flight duration” to determine if the long-term certainty of a fixed rate or the tactical lift of an ARM fits your timeline.

- Discover why a fixed-rate mortgage serves as a reliable anchor, protecting your monthly payment from inflation even as Michigan market conditions shift.

- Uncover the mechanics of interest rate caps and margins to see if a lower entry cost can help you navigate current housing prices more effectively.

- Compare the long-term costs of an adjustable-rate vs fixed-rate mortgage Michigan to see which path offers the most efficient route for your financial horizon.

- Explore how to pair your selected loan type with MSHDA Down Payment Assistance to lower your barrier to entry without compromising your safety.

The Flight Plan: Understanding Fixed-Rate vs. Adjustable-Rate Mortgages in Michigan

Choosing a mortgage in 2026 isn’t just about finding the lowest number on a screen. In West Michigan cities like Kalamazoo, where home values have shown steady growth, your choice is actually a strategic flight plan. You’re deciding how you want to handle the “altitude” of your interest rate over the next several years. The core debate of an adjustable-rate vs fixed-rate mortgage Michigan centers on one thing: do you value the certainty of a level flight or the flexibility of a tactical descent? Viewing your mortgage as a precision tool rather than a generic debt allows you to maintain control, even when local economic winds shift. It’s about matching your loan structure to your actual life goals and your expected time in the cockpit.

What is a Fixed-Rate Mortgage?

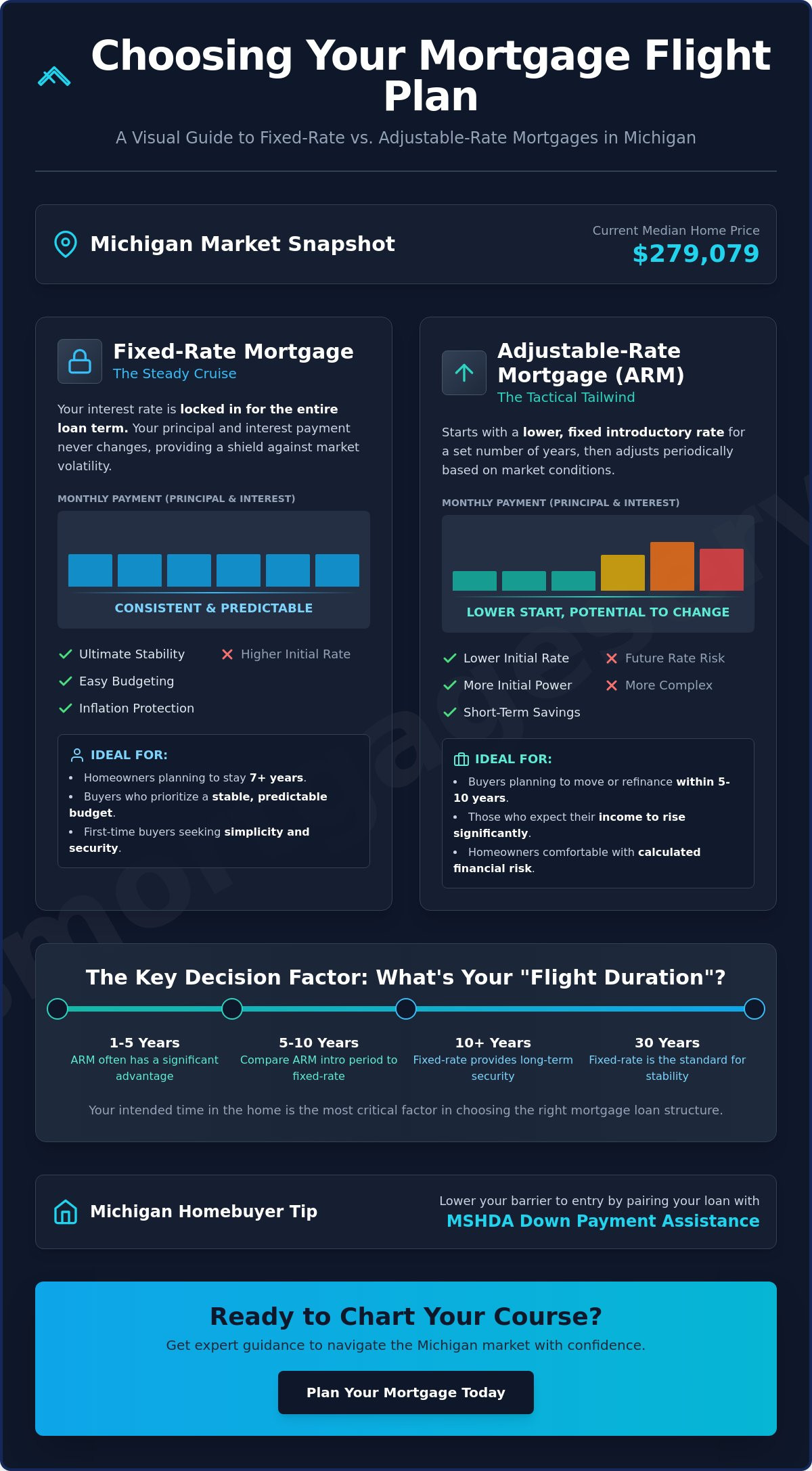

A fixed-rate mortgage is a loan where your interest rate is locked in at the start and never moves for the entire duration of the term. Think of this as your “Steady Cruise.” Whether you are settling into a classic home in Portage or a new build in Battle Creek, your principal and interest payments remain identical from the first month to the last. This predictability acts as a shield against inflation and market volatility. As wages generally rise over time, your housing cost remains a fixed point on your horizon. For many, Understanding Fixed-Rate Mortgages is the first step toward long-term peace of mind. It eliminates the risk of future rate hikes disrupting your family budget; it’s the gold standard for those planning to stay in their Michigan home for a decade or more. You’ll always know exactly what’s required to keep your home on course.

What is an Adjustable-Rate Mortgage (ARM)?

An Adjustable-Rate Mortgage, or ARM, offers a different kind of momentum. These loans begin with an “introductory period” where the interest rate is typically lower than standard fixed options. You might see these labeled as 5/1, 7/1, or 10/1 ARMs. The first number represents how many years your rate stays fixed; the second number indicates how often it adjusts after that. We often call this the “Tailwind” approach. By securing a lower initial rate, you gain early financial lift. This can be especially useful for Michigan buyers who plan to relocate or upgrade their home before the introductory period ends. It’s a tactical choice. It requires a disciplined navigator who understands that the rate will eventually reset based on current market indices. While it offers lower initial payments, you must be prepared for the eventual adjustment phase. Knowing your “flight duration” is key to deciding if this path provides the momentum you need.

Fixed-Rate Mortgages: The Steady Cruise for Long-Term Stability

The 30-year fixed mortgage remains the most trusted flight path for families in Portage and Battle Creek. It’s a choice that prioritizes long-term stability over short-term gains. When you evaluate an adjustable-rate vs fixed-rate mortgage Michigan, the fixed-rate option acts as your heavy-duty anchor. Your principal and interest payments are locked in for the life of the loan. This means your housing costs won’t change, even if the national economy experiences sudden turbulence. It provides a level of certainty that allows you to plan for other life milestones without the fear of a shifting financial foundation.

This predictability is a powerful tool for simplifying your household budget. While other costs of living might climb, your mortgage payment stays the same. Over decades, this creates a natural protection against inflation. As your wages likely rise over time, the percentage of your income dedicated to your mortgage actually shrinks. You can find an official government comparison that highlights how these fixed terms contrast with floating rates, but for many Michigan homeowners, the primary benefit is simply knowing that their “flight altitude” is secure. You are effectively locking in today’s costs for tomorrow’s shelter.

There is a specific trade-off to keep in mind. Fixed-rate loans typically carry a higher initial interest rate compared to the introductory rates found on ARMs. You are essentially paying a small premium for the guarantee that your rate will never increase. It’s a long-term engineering decision; you trade a slightly higher cost today for total protection against the unknown risks of tomorrow. For families who value sleep-at-night security, this is often a price well worth paying.

When a Fixed Rate is Your Best Co-Pilot

Choosing a fixed rate is often the smartest move if your personal flight plan includes the following scenarios:

- Long-Term Residency: You plan to stay in your Michigan home for 10 years or more, allowing the stability of the rate to pay off over the long haul.

- Low Risk Tolerance: You prefer a consistent, unchanging monthly expense and don’t want to monitor market indices for potential resets.

- Your Forever Home: You’ve found the perfect property in a competitive Kalamazoo neighborhood and want to cement your housing costs for the next few decades.

Fixed-Rate Options at Treadstone Mortgage

We provide a variety of fixed-rate paths tailored to the unique needs of West Michigan buyers. Whether you are looking for a Conventional mortgage, a low-down-payment FHA mortgage, or a VA mortgage for our local veterans, we can help you secure a stable foundation. Our team is dedicated to helping you lock in the most favorable Current Mortgage Rates in Kalamazoo so your journey starts on solid ground. If you’re ready to see how these steady options fit your budget, reaching out to a local expert can provide the personalized care you deserve to keep your financial future on course.

Adjustable-Rate Mortgages (ARMs): Leveraging Market Tailwinds

While the fixed-rate path offers a steady cruise, an Adjustable-Rate Mortgage (ARM) can provide the initial “lift” needed to get your Michigan home purchase off the ground. Many homebuyers view an ARM as a gamble, but it’s actually an engineered financial tool that trades long-term certainty for immediate affordability. By securing a lower initial interest rate, you reduce your monthly entry cost. This is particularly valuable in a market where the statewide median home sale price reached $279,079 in April 2026. Lower payments in the first few years provide extra breathing room for home improvements or building your savings.

Understanding the mechanics is essential for any navigator. Every ARM reset is governed by three components: the Index, the Margin, and the Caps. The Index is the market benchmark, while the Margin is the fixed percentage the lender adds. The Caps act as your safety limits. You can find a deeper dive into these structures in the Consumer Financial Protection Bureau’s guide to loan options. This framework ensures that your “flight path” remains within a controlled range, even if market indices rise. An ARM isn’t a blind risk; it’s a calculated decision for those with a clear exit or refinance strategy.

The primary fear for Michigan buyers is the anxiety that their payment might double overnight. This simply doesn’t happen with modern, transparent loan products. The adjustment caps prevent such drastic spikes. When choosing between an adjustable-rate vs fixed-rate mortgage Michigan, remember that an ARM is a tactical choice. It isn’t a “set it and forget it” loan. Instead, it’s a strategic path for those who want to leverage current market tailwinds to their advantage.

The Strategic Advantage of an ARM

An ARM is often the ideal co-pilot for specific life stages. If you are purchasing a “starter home” and plan to move within five to seven years, paying a premium for a 30-year lock you won’t use doesn’t make sense. It allows you to maximize your monthly cash flow during those early years. Real estate investors also utilize these paths for tactical acquisitions. They use the lower initial payments to improve the property’s immediate “lift” before a planned sale or a Refinance Mortgage later on.

Understanding the Safety Gear: Rate Caps

Flight safety is our top priority. To prevent turbulence during the reset period, ARMs include specific rate caps. Initial adjustment caps limit the first jump, while periodic and lifetime caps set a definitive ceiling on your interest rate. Jeremy Drobeck frequently emphasizes this “safety gear” to ensure clients understand that their monthly payments won’t spiral out of control. It’s about precision. By knowing the absolute maximum your rate could ever reach, you can plan your landing with total confidence. When you understand the limits, the fear of the unknown disappears.

The Michigan Comparison: Which Path Fits Your Financial Horizon?

Deciding between an adjustable-rate vs fixed-rate mortgage Michigan requires looking past the first month’s payment to see the entire horizon. While an ARM might offer a lower entry point, a fixed-rate loan provides a level of certainty that many Michigan families find essential. In a market where the statewide median home sale price reached $279,079 in April 2026, every percentage point matters. You must calculate the total interest paid over your expected “flight duration.” If you plan to stay in the cockpit for only seven years, the cumulative savings of an ARM might outweigh the safety of a fixed lock. However, if this is your long-term residence, the fixed-rate path often becomes the more efficient route.

Your total monthly “altitude” isn’t just about the interest rate. In Michigan, property taxes play a significant role. Thanks to Proposal A, your taxable value is capped while you own the home, but it resets to the State Equalized Value upon purchase. This can cause a sudden jump in your monthly escrow. When you pair this with a potentially shifting ARM rate, your budget could face unexpected turbulence. We often recommend that buyers looking for maximum stability consider how MSHDA Down Payment Assistance can be paired with fixed-rate products. This combination provides the “lift” of a lower down payment while keeping your monthly principal and interest locked on a steady course.

It is also vital to perform a refinance reality check. Many buyers choose an ARM with the assumption they can “just refinance” if rates drop later. This is a tactical maneuver, not a guarantee. Refinancing requires sufficient home equity and a stable credit profile. If Michigan home values stall or your personal financial situation changes, you might find yourself unable to change your flight path. You should only choose an ARM if you are comfortable with the maximum possible rate cap or have a definitive plan to exit the loan before the reset occurs. If you want to explore these numbers with a local navigator, you can start your flight plan today with our team.

Local Considerations for Kalamazoo & Portage

Market conditions in West Michigan are unique. While national trends provide a general forecast, local inventory in Kalamazoo and Portage remains competitive. Using a Purchase Mortgage to secure a home in these neighborhoods often requires a quick, decisive offer. If you are eligible for MSHDA programs, you might find that a fixed-rate FHA loan provides the best balance of low entry costs and long-term security. These programs are specifically designed to help Michigan residents compete with cash buyers, providing the momentum needed to win the bid.

The ‘Break-Even’ Analysis

Every financial journey has a break-even point. This is the moment where the total interest paid on a 30-year fixed loan becomes less than the cumulative cost of an ARM after its initial reset period. You must factor in closing costs, which typically range from 2% to 5% of the purchase price, and any future refinance fees. For a $250,000 home, these costs can range from $5,000 to $12,500. The break-even point for a 5/1 ARM versus a 30-year fixed is the specific month where the higher interest of the fixed rate is finally offset by the avoided rate hikes of the adjustable loan.

Navigating Your Choice with a Local Michigan Expert

A generic online calculator is often the first tool a homebuyer reaches for, but it’s essentially a static map. It can’t account for the real-time “wind speeds” of the Kalamazoo housing market or the specific elevation changes in your personal financial life. These tools often miss the nuance of Michigan property tax resets or the specific requirements of local assistance programs. When you’re deciding between an adjustable-rate vs fixed-rate mortgage Michigan, you need a dynamic flight plan tailored to your actual destination. We don’t just look at today’s rate; we analyze your overall “financial lift” to ensure you have the momentum needed for the entire journey.

The Treadstone difference is rooted in neighborly reassurance and technical precision. We view the mortgage process as a partnership, not a cold transaction. Our team takes the time to understand your “flight duration”—how long you truly plan to stay in the home—before recommending a specific loan structure. This personalized care ensures that you aren’t just getting a loan; you’re getting a strategic tool designed to protect your household budget from unnecessary turbulence. Whether you need the steady cruise of a fixed rate or the tactical advantage of an ARM, we provide the transparent guidance required to make that call with total confidence.

Your Pre-Flight Checklist

Before you step into the cockpit, a thorough inspection is required. This begins with a comprehensive review of your financial documents. Your credit score acts as a primary engine component; it determines the “thrust” or pricing available for both fixed and ARM options. Higher scores often unlock more favorable terms that can significantly lower your long-term costs. Consulting with Jeremy Drobeck allows you to map out your long-term goals against these technical requirements. We help you gather everything needed for a smooth pre-approval in the Kalamazoo area, ensuring you’re ready to move when the right property appears on your radar.

Ready for Takeoff?

Initiating your Michigan home loan journey starts with a simple conversation. You don’t have to navigate the complexities of interest rate indices or adjustment caps alone. Having an expert co-pilot from the initial application through to the final closing provides a layer of safety that generic lenders simply can’t match. We are present throughout the entire duration of the process, ensuring every detail is handled with precision. If you are ready to secure your future in West Michigan, it is time to build a strategy that fits your life. You can schedule your mortgage flight plan with Jeremy Drobeck today to begin your journey with a seasoned navigator by your side.

Securing Your Michigan Home Landing

Choosing your path between an adjustable-rate vs fixed-rate mortgage Michigan isn’t just about today’s numbers; it’s about the life you’re building for tomorrow. We’ve explored how a fixed-rate cruise offers absolute certainty against market turbulence, while a tactical ARM provides the early lift needed to enter competitive West Michigan markets. Both paths are engineered for safety when you have a clear understanding of your “flight duration” in Kalamazoo, Portage, or Battle Creek. Your decision should reflect where you want to be decades from now.

You don’t have to make this high-stakes decision alone. Expert guidance from Jeremy Drobeck at Treadstone Mortgage ensures your flight plan is precise and personalized. As a division of Neighborhood Loans, Inc. (NMLS #222982), we’re committed to being your reliable ally from application to landing. It’s time to replace anxiety with a sense of calm, expert navigation that puts you in control of your journey. You deserve a partner who values preparation and precision as much as you do.

Start your personalized Michigan mortgage flight plan today and move forward with total confidence.

Frequently Asked Questions

Are ARM loans worth it in Michigan in 2026?

ARM loans are worth it if your intended flight duration is shorter than the introductory period. If you plan to relocate or upgrade within five to seven years, the lower initial interest rate provides significant monthly savings. With Michigan median home prices reaching $279,079 in April 2026, gaining that extra lift early on can help you manage other costs. You just need a clear exit strategy before the first reset occurs.

How often do ARM rates change after the initial period?

Most ARM rates adjust annually once the initial fixed-rate period concludes. For instance, a 5/1 or 7/1 ARM maintains a steady rate for the first five or seven years, followed by a reset every twelve months. Some modern structures might adjust every six months. You should always review your specific loan documents to understand the exact frequency of these adjustments so you can prepare your household budget for any changes.

Can I switch from an ARM to a fixed-rate mortgage later?

You can switch by using a Refinance Mortgage to move into a fixed-rate path. This isn’t an automatic transition; it requires a new application, a fresh appraisal, and standard closing costs. It is a common strategy for those who used an ARM for initial lift but now want the long-term stability of a locked rate as their residency duration extends. Your local navigator can help you time this move perfectly.

What is the most common ARM index used by Michigan lenders?

The 30-day Average SOFR (Secured Overnight Financing Rate) is currently the most common benchmark used by lenders. This index has replaced older standards to provide a more stable and transparent foundation for rate adjustments. When evaluating an adjustable-rate vs fixed-rate mortgage Michigan, knowing your index is essential. Your final rate is determined by adding a set margin to this SOFR index, creating a controlled framework for your future payments.

Is a fixed-rate mortgage better for a first-time homebuyer in Kalamazoo?

A fixed-rate mortgage is often the preferred choice for first-time buyers who value long-term predictability. Using a fixed-rate Purchase Mortgage ensures that your principal and interest payments never change, providing a stable anchor for your new household budget. While an ARM might offer a lower initial payment, the certainty of a fixed lock eliminates the stress of future market turbulence. It’s about choosing the most comfortable flight path for your experience level.

How do rate caps protect me if interest rates skyrocket?

Rate caps act as your safety gear by setting a definitive ceiling on how much your interest rate can increase. There are typically three types: initial caps, periodic caps, and lifetime caps. These limits ensure that even if market indices spike, your interest rate can only move up by a specific, pre-determined percentage during each adjustment period. This engineered safety feature prevents your monthly payments from spiraling out of control during the reset phase.

Does Treadstone Mortgage offer both fixed and adjustable-rate options?

We offer a comprehensive suite of loan products including Conventional, VA, and FHA fixed-rate paths alongside various ARM structures. Our team provides the expert guidance needed to determine which tool offers the best lift for your specific situation. By comparing an adjustable-rate vs fixed-rate mortgage Michigan with a local navigator, you can select a flight plan that balances initial affordability with long-term security. We are here to support you throughout the entire process.

What happens if Michigan home values decline while I have an ARM?

Declining home values can make it difficult to use a Refinance Mortgage to move into a fixed rate. If you owe more than the home is worth, you might be stuck with the ARM until values recover or you pay down the balance. This is why we emphasize having a solid landing strip, or equity cushion, before choosing an adjustable path. We help you analyze local market trends to ensure your strategy remains sound.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”