Understanding Private Mortgage Insurance (PMI) in Michigan: Your 2026 Homeownership Flight Plan

Paying for insurance that protects your lender rather than your own assets feels like a headwind you didn’t ask for. It’s easy to view these monthly charges as “lost money,” especially when you’re trying to maintain a steady altitude in the 2026 housing market. However, understanding private mortgage insurance (PMI) in Michigan is actually the key to gaining the necessary lift for an early takeoff. Rather than waiting years to save a 20% down payment, PMI acts as the stabilizer that lets you secure a home today while prices continue to shift.

We know the confusion between PMI and FHA MIP can feel like flying through heavy fog, especially with the “One Big Beautiful Bill Act” making these premiums tax-deductible again for the 2026 tax year. This guide will help you master the mechanics of these payments so you can lower your monthly costs and navigate your purchase with total confidence. You’ll discover the exact price points for Michigan homeowners, a clear strategy for early removal through home equity, and the precise flight path to choosing the loan product that fits your family’s budget.

Key Takeaways

- Understanding private mortgage insurance (PMI) in Michigan reveals it isn’t a financial penalty, but rather the mechanical lift that helps you secure a home years earlier than expected.

- Your credit score and loan-to-value ratio act as the flight controls for your monthly costs. A stronger financial profile leads to significantly lower insurance premiums.

- Conventional PMI provides a more flexible exit strategy than FHA MIP because it can be removed once your home equity reaches specific milestones.

- You can request a manual cancellation of your PMI once your mortgage balance hits 80% of the home’s value, saving you money before automatic termination occurs at 78%.

- Partnering with a seasoned navigator ensures your 2026 mortgage plan is engineered for the Michigan market, offering stability and expert guidance throughout your entire journey.

The Mechanics of PMI: A Safety Net for Your Michigan Home Purchase

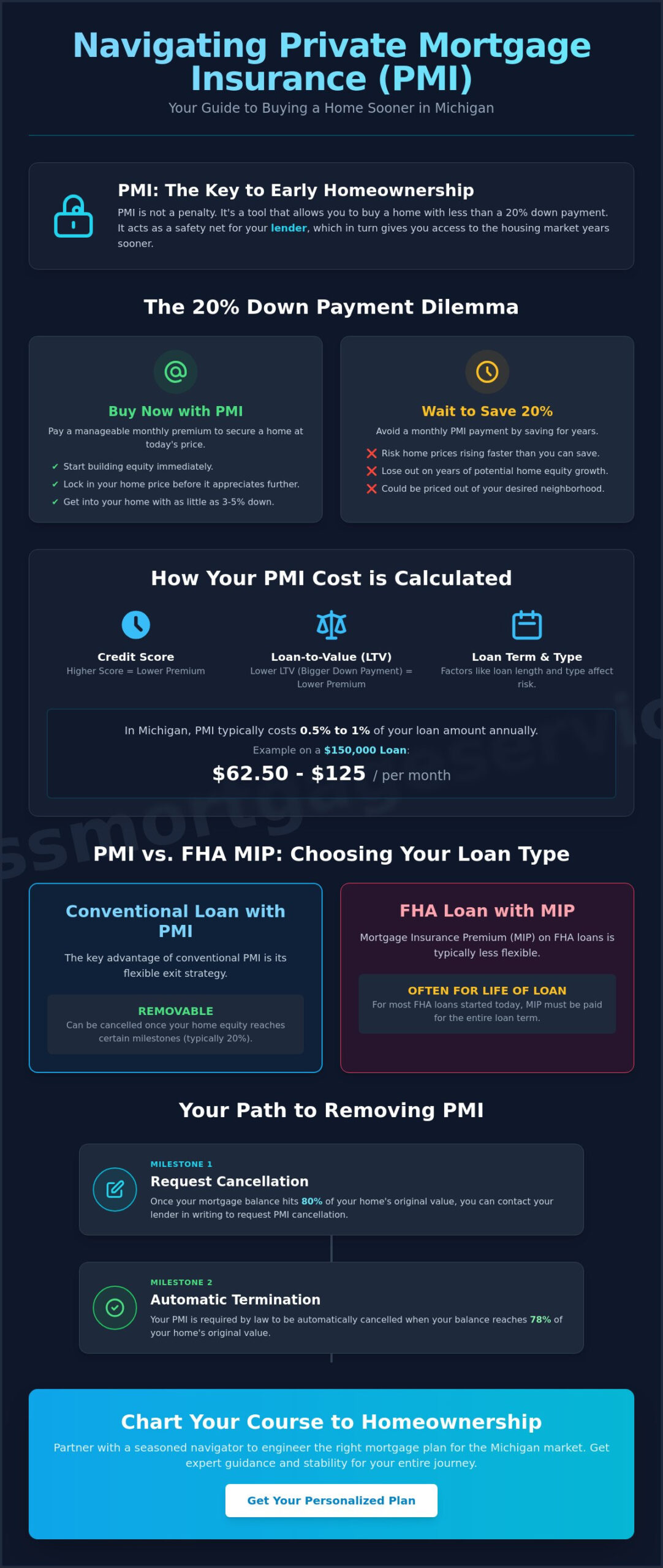

Your mortgage journey is a lot like a flight plan. When your “flight weight,” or down payment, is under 20%, lenders require a specific piece of equipment to ensure a safe journey. Understanding private mortgage insurance (PMI) in Michigan is the first step in realizing that this isn’t a financial penalty. It’s a mechanical necessity that provides the lift needed for your homeownership goals to take flight. By acting as an engine component for a Conventional Mortgage, PMI allows you to bypass the traditional requirement of a massive upfront payment.

Essentially, Mortgage insurance acts as a safety net for the lender. It compensates them if a borrower is unable to maintain the flight path and defaults on the loan. While this protection serves the financial institution, the real benefit for you is immediate market access. Without PMI, most Michigan families would be grounded for years while trying to save 20% of a home’s purchase price. Instead, this temporary stability measure allows you to enter the market with as little as 3% or 5% down, getting you into your new home much sooner.

PMI vs. Homeowners Insurance: Clearing the Air

It’s common to confuse these two protective layers, but they serve very different roles in your aircraft’s maintenance. Think of homeowners insurance as your hull integrity; it protects the physical structure of your home from fire, wind, or storms. In contrast, PMI is your flight stabilizer. It doesn’t protect your furniture or the roof. It protects the integrity of the loan structure itself. Despite their different functions, both are usually managed through your Michigan escrow account, making your monthly payments predictable and streamlined.

Why 20% Down Isn’t Always the Best Flight Path

Waiting to reach a 20% down payment might seem like the safest route, but in the 2026 Michigan real estate market, it can actually lead to a missed connection. Home values in areas like Kalamazoo and Grand Rapids often appreciate faster than a family can save cash. If home prices rise by several percentage points in a single year, waiting to avoid a small PMI premium could cost you tens of thousands of dollars in lost equity. The trade-off is clear: you can pay a manageable monthly premium now to secure today’s home price, or you can risk paying a much higher price for the same house later. Understanding private mortgage insurance (PMI) in Michigan allows you to make this calculation with precision rather than guesswork.

Calculating the Lift: How Much Does PMI Cost in Michigan?

Determining your monthly premium isn’t a guessing game; it’s a calculation based on the specific aerodynamics of your financial profile. To begin, you should ask: What is private mortgage insurance? and how does it apply to my specific loan? Understanding private mortgage insurance (PMI) in Michigan involves looking at three primary dials: your credit score, your loan-to-value (LTV) ratio, and your loan term. These factors determine the lift required to get your loan approved while keeping your monthly costs manageable.

Think of your LTV ratio as the “drag” on your aircraft. If you’re putting down 3%, the insurance company sees a heavier risk profile than if you’re putting down 15%. In Michigan, where median home prices in areas like Kalamazoo or Portage offer a steady entry point for families, this premium typically ranges between 0.5% and 1% of your total loan amount annually according to 2026 industry data. For a $150,000 loan, this might mean an extra $62.50 to $125 added to your monthly statement. While this is an additional cost, it’s often much lower than the price increases you might face if you waited several years to save a full 20% down payment.

Payment Options: Monthly vs. Upfront Premiums

Most Michigan homeowners choose the “Standard Flight” path, which is a monthly premium added to the mortgage payment. It’s the most accessible route because it requires no extra cash at the closing table. However, some travelers prefer the “Pre-Flight Payoff,” also known as single-premium PMI. This involves paying a one-time fee upfront to eliminate the monthly charge entirely. There is also Lender-Paid Mortgage Insurance (LPMI), where the lender pays the premium in exchange for a slightly higher interest rate. Each path has its own turbulence and benefits depending on how long you plan to keep the loan. We take the time to model these scenarios with you so the decision feels engineered for your specific goals.

The Credit Score Connection

Your FICO score is the most significant factor in your PMI altitude. A higher score creates a “streamlined profile” that insurance companies reward with lower rates. Even a modest 20-point increase in your score can significantly reduce your monthly premium, potentially saving you thousands over the life of the loan. We often help our clients review their financial profile before application to ensure they are positioned for the most efficient flight path possible. By optimizing your score early, you ensure that understanding private mortgage insurance (PMI) in Michigan becomes a strategy for savings rather than just another line item on your monthly bill.

PMI vs. FHA MIP: Navigating the Best Path for Your Budget

Choosing between a Conventional Mortgage and an FHA Mortgage is like selecting the right fuel grade for your specific aircraft. While both require insurance when your down payment is low, the mechanics of these premiums are fundamentally different. Understanding private mortgage insurance (PMI) in Michigan is particularly important when you consider local programs like MSHDA Down Payment Assistance. These programs can provide the initial lift you need, but the type of insurance you carry will determine your long-term monthly costs and how much you eventually pay for your home.

Private MI is designed for Conventional loans and is provided by private companies. FHA MIP (Mortgage Insurance Premium) is a government-backed product. The most striking difference is the exit strategy. Conventional PMI is a detachable component; once you have enough equity, you can remove private mortgage insurance (PMI) and lower your monthly overhead. FHA MIP, however, is typically welded to the loan for its entire duration unless you put down 10% or more at the start of your journey.

When Conventional PMI Wins

If your credit score is in a higher bracket, Conventional PMI is usually the most efficient path for your budget. Because the cost of private insurance is heavily tied to your “pilot profile” or credit score, a strong history allows you to secure a much lower monthly premium than the flat rates often found with government products. Over a 10-year horizon, the ability to drop the extra weight of PMI once you reach 20% equity can save you thousands of dollars. It’s the preferred route for those looking to optimize their monthly cash flow as their home value grows in the Michigan market. This flexibility lets you adjust your financial trajectory without needing to refinance your entire loan just to eliminate an insurance cost.

When FHA MIP is the Right Navigator

FHA loans are designed to provide stability when the flight conditions aren’t perfect. If your credit score is lower or your debt-to-income ratio is a bit higher, FHA MIP acts as a reliable stabilizer that Conventional lenders might not offer. This path includes an upfront MIP payment, currently 1.75% of the loan amount as of June 2026, which is usually rolled into the total balance. While Conventional PMI is a detachable stabilizer that falls away once you reach cruising altitude, FHA MIP is often a permanent part of the aircraft’s structure for the life of the loan. For many Michigan families, this is a fair trade-off to achieve the milestone of homeownership sooner, especially when paired with local assistance programs that help cover closing costs.

The Flight Path to Removal: How to Cancel PMI and Save Money

Once your home purchase has reached cruising altitude, your primary objective becomes shedding the extra weight of insurance premiums. Understanding private mortgage insurance (PMI) in Michigan involves knowing exactly when you can detach this stabilizer to improve your monthly cash flow. You don’t have to carry this cost for the entire duration of your 30-year term. Instead, federal law provides clear exit ramps based on your loan-to-value (LTV) ratio, allowing you to reallocate those funds toward your principal or other financial goals.

The Homeowners Protection Act establishes two primary milestones for removal. First, you can request a manual cancellation once your mortgage balance reaches 80% of the home’s original value. This requires a written request and a clean payment history. Second, the lender must provide automatic termination once your balance is scheduled to hit 78% of the original value. However, waiting for the automatic trigger often means paying premiums for months or years longer than necessary. By monitoring your balance, you can take control of the controls and request removal the moment you hit the 80% mark.

Accelerating Your Equity Growth

In the 2026 market, many homeowners in Kalamazoo and Portage are finding that local property appreciation acts as a powerful tailwind. If market values in your neighborhood have climbed significantly since your closing date, you might reach 20% equity much sooner than your payment schedule suggests. You can also create an “instant lift” in equity through strategic home improvements. If you used a Renovation Mortgage to update a kitchen or add a bathroom, those upgrades often increase your home’s market value enough to flip your LTV ratio in your favor. Proving this new value typically requires a fresh appraisal, which serves as an official instrument check to confirm your home’s current worth.

The Refinance Strategy

Sometimes, the most efficient way to eliminate PMI is to transition to a completely new flight plan. If interest rates have shifted or your home value has spiked, a Refinance Mortgage can eliminate the insurance requirement entirely. This is especially effective if your current LTV has dropped from 95% to 80% due to a combination of principal payments and market growth. We help you run a “break-even” calculation to ensure that the savings from removing PMI outweigh the closing costs of the new loan. Understanding private mortgage insurance (PMI) in Michigan means looking at your mortgage as a dynamic tool that can be adjusted as your equity grows.

If you suspect your home’s value has increased enough to shed your monthly insurance costs, contact us today for a personalized equity review.

Charting Your Course: Personalized Mortgage Guidance in Kalamazoo

Every successful flight depends on a navigator who knows the local terrain and the specific mechanics of the aircraft. While understanding private mortgage insurance (PMI) in Michigan provides the technical foundation for your purchase, applying those rules to a home in Kalamazoo or Portage requires a personalized touch. Jeremy Drobeck and the team at Treadstone Mortgage act as your dedicated co-pilots, ensuring that every calculation is precise and every decision is transparent. We view the mortgage process as a significant life milestone, not just a financial transaction, which is why we offer supportive, partnership-based guidance from start to finish.

Our commitment to end-to-end support means we stay in the cockpit with you from the initial pre-approval until the final landing at the closing table. We don’t just provide a generic rate; we perform a deep-level analysis of your specific debt-to-income ratio and credit profile. This allows us to identify the most efficient loan product for your needs, whether that is a Conventional Mortgage with a plan for early PMI removal or a Purchase Mortgage that utilizes local assistance programs. By engineering a plan tailored to your financial goals, we help you avoid unnecessary costs and maximize your long-term savings.

Expert Analysis for Kalamazoo and Portage Buyers

West Michigan has unique neighborhood values and growth patterns that can significantly impact your equity trajectory. Our team possesses deep expertise in the Kalamazoo and Portage markets, allowing us to project how local appreciation might help you shed PMI faster than the national average. We take pride in simplifying complex technical jargon into a clear, actionable flight plan. During a personalized consultation, we can review your PMI projections and show you exactly how different down payment scenarios will affect your monthly “fuel burn” and overall budget stability.

Your Next Steps to Homeownership

Before you begin house hunting, it is vital to complete a thorough pre-flight check. A robust pre-approval gives you the confidence to make competitive offers in a fast-moving market. We are ready to assist you at our offices in Kalamazoo, Portage, or Battle Creek, providing the neighborly reassurance and professional authority you deserve. Our goal is to make the journey toward your new home feel like a controlled, engineered process rather than a gamble. Understanding private mortgage insurance (PMI) in Michigan is much easier when you have a seasoned navigator by your side to handle the heavy lifting.

Schedule your mortgage flight plan consultation today!

Secure Your Financial Flight Path

Mastering the mechanics of your mortgage is the most effective way to ensure a smooth landing in your new home. By understanding private mortgage insurance (PMI) in Michigan, you’ve learned that these premiums are temporary stabilizers rather than permanent fixtures. Whether you choose a Conventional Mortgage for its detachable insurance or an FHA Mortgage for its accessible entry points, your success depends on a strategy built for the 2026 market. Monitoring your home equity and local appreciation in Kalamazoo or Portage will eventually allow you to shed that extra weight and lower your monthly overhead.

With over 20 years of Michigan lending expertise, we specialize in helping families navigate complex tools like MSHDA programs and Renovation loans. As a division of Neighborhood Loans, Inc. (NMLS #222982), we’re committed to providing the transparency and neighborly reassurance you need for this significant life milestone. Ready to chart your course? Get your personalized Michigan mortgage flight plan here! We look forward to being your steady ally throughout the entire journey and seeing you reach your destination with confidence.

Frequently Asked Questions

Is PMI required in Michigan if I put 20% down?

No, you don’t need PMI if you provide a 20% down payment on a conventional loan. This “flight weight” provides enough security for the lender to skip the insurance requirement entirely. If you’re understanding private mortgage insurance (PMI) in Michigan, you’ll see that reaching this 20% mark is the most direct way to keep your monthly costs as lean as possible from day one.

Can I avoid PMI by taking out a second mortgage (Piggyback Loan)?

You can avoid PMI by using a “piggyback loan,” which is a second mortgage taken out at the same time as your first. A common structure is the 80-10-10 plan, where you have an 80% first mortgage, a 10% second mortgage, and a 10% down payment. This multi-engine approach keeps your primary loan at the 80% threshold, effectively bypassing the need for private insurance premiums.

How do I know if my Michigan home has enough equity to cancel PMI?

Start by reviewing your monthly mortgage statement to see your current principal balance. Divide that balance by the original purchase price or a recent professional appraisal to find your current LTV ratio. If the result is 0.80 or lower, you likely have the necessary equity. We recommend an official instrument check through a new appraisal if you believe Kalamazoo market appreciation has pushed you over the 20% equity mark.

Is PMI tax-deductible in 2026?

Yes, PMI premiums are tax-deductible for the 2026 tax year under the Working Families Tax Cuts Act. This deduction is available for homeowners who itemize and fall within specific income thresholds, such as an AGI up to $100,000 for married couples filing jointly. This legislative update provides a helpful tailwind for Michigan families, making the cost of low down payment loans more manageable during the 2026 tax season.

Does PMI increase my interest rate or just my monthly payment?

Standard PMI is a separate line item that increases your monthly payment rather than your interest rate. It functions like an add-on stabilizer for your loan. However, if you choose Lender-Paid Mortgage Insurance (LPMI), the lender pays the premium in exchange for a slightly higher interest rate on the loan. understanding private mortgage insurance (PMI) in Michigan helps you decide if you’d prefer a higher monthly fuel burn or a different interest rate configuration.

What happens if I forget to request PMI cancellation at 80% LTV?

If you miss the 80% milestone, you’ll continue to pay the monthly premium until your loan reaches the 78% automatic termination point. The lender isn’t required to stop the charges at 80% unless you initiate the request in writing. Taking manual control of your flight path at 80% LTV can save you hundreds of dollars in unnecessary premiums that would otherwise be charged while waiting for the “autopilot” 78% termination to kick in.

How does the MSHDA program interact with PMI requirements?

MSHDA programs provide essential down payment assistance, but they don’t automatically eliminate the need for PMI. If your total down payment, including MSHDA funds, is less than 20% of the purchase price, your conventional lender will still require insurance. Think of MSHDA as a secondary booster that helps you get off the ground, while PMI provides the stability needed for the lender to approve a loan with a smaller personal cash investment.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”