Am I Too Old to Get a 30-Year Mortgage in Michigan? Your 2026 Guide

What if the “year of your model” mattered far less than the “altitude” of your financial stability? Many Michiganders approaching their golden years worry that a bank will see their birth date as a reason to ground their homeownership dreams. You might be asking yourself, am I too old to get a 30-year mortgage in Michigan, especially as you look toward a fixed income. It’s a common concern; however, the reality of modern lending in 2026 is much more encouraging than you might think.

We understand that the thought of carrying debt into your seventies or eighties can feel like a heavy cargo. You want to ensure your retirement is secure and not weighed down by complex financial hurdles. This guide will show you why age is never a legal barrier to securing a loan in our state and how a 30-year term can actually protect your monthly cash flow. We’ll preview how lenders calculate Social Security income and outline a clear flight plan for choosing between a Purchase Mortgage, an FHA loan, or even a Refinance Mortgage to keep your retirement plans on course.

Key Takeaways

- Learn why federal and Michigan laws protect your right to borrow, ensuring no lender can ground your application based on your age or life expectancy.

- Discover how Social Security and pension distributions provide the necessary lift to clear income requirements when asking, “am I too old to get a 30-year mortgage in Michigan?”

- Understand the strategic advantage of a 30-year term as a stabilizer for your retirement cash flow, keeping monthly obligations manageable while you enjoy your golden years.

- Explore alternative flight paths such as the 15-year fixed mortgage or specialized programs designed to help families secure a primary residence together.

- See why a local Michigan expert acts as a seasoned navigator, helping you avoid turbulence and guiding you through the specific regional requirements of the 2026 market.

The Short Answer: Is There a Maximum Age for a 30-Year Mortgage in Michigan?

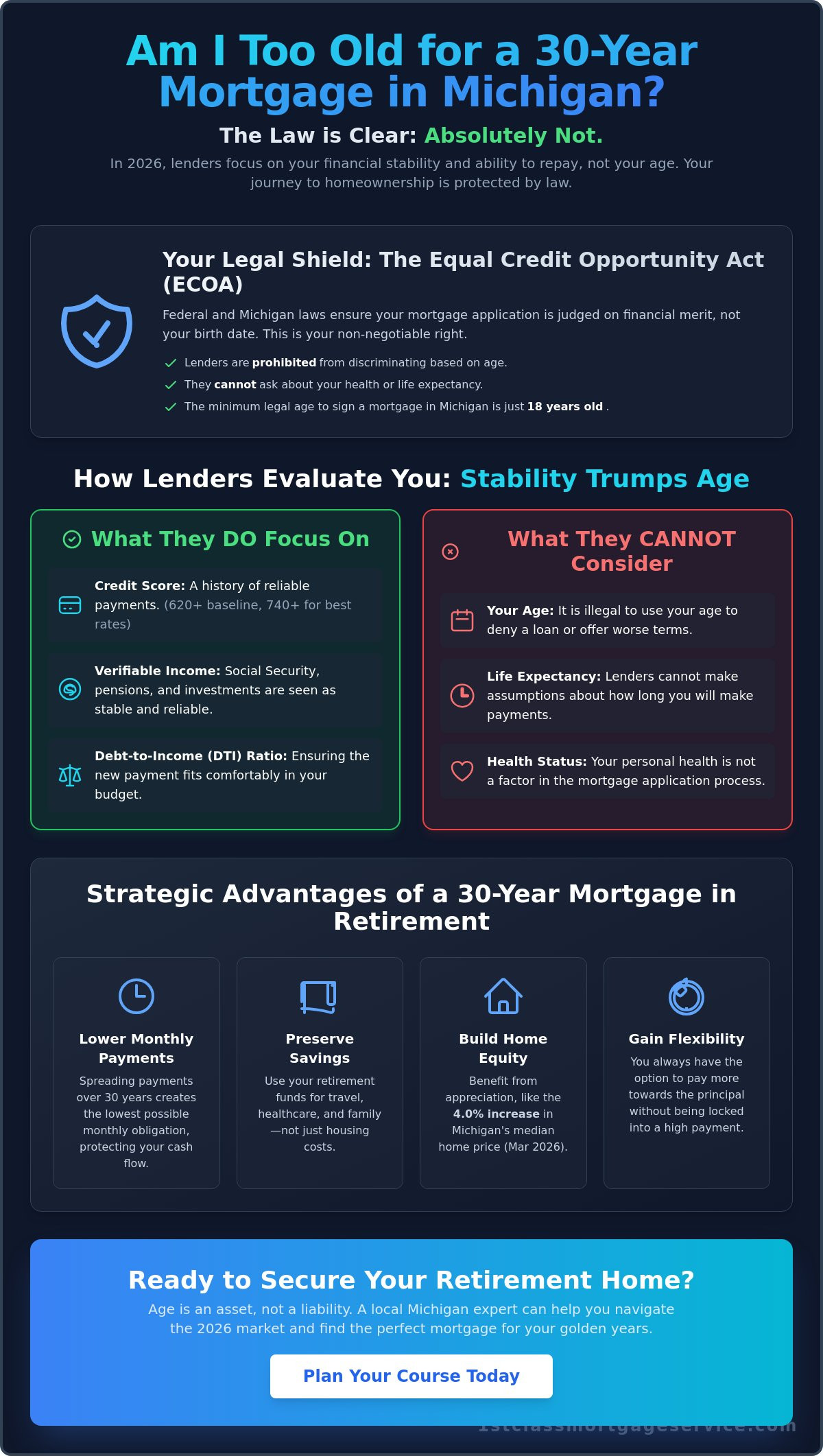

The simple truth is that you cannot be aged out of a home loan. If you are wondering, am I too old to get a 30-year mortgage in Michigan, the law is firmly on your side. In the Great Lakes State, the only age requirement for a mortgage is that you must be at least 18 years old to legally sign the contract. Beyond that, your birth year is irrelevant to your eligibility. Lenders are strictly prohibited from using your age as a reason to deny your application or to offer you less favorable terms. Your financial journey is judged by your stability, not your age.

Understanding the Equal Credit Opportunity Act (ECOA)

This federal protection acts as a steadying force for senior borrowers. The Equal Credit Opportunity Act ensures that your flight plan toward homeownership is judged solely on your financial merits. Under this law, it’s illegal for a lender to discriminate against an applicant on the basis of age. For borrowers over 60, the Equal Credit Opportunity Act serves as a legal shield that prevents lenders from factoring in your age or making assumptions about your future income. Lenders must treat your application with the same individualized care they would give to a borrower decades younger.

Lenders aren’t allowed to ask about your health or your life expectancy. They cannot speculate on how long you might be around to make payments. Instead, they must focus on your current altitude, which includes your credit score, your existing assets, and your verifiable income. Whether that income comes from a traditional paycheck, Social Security, or a pension, it’s the stability of those funds that matters. Your ability to repay is the primary instrument they use for navigation, regardless of the number of candles on your last birthday cake.

Why Michigan Homebuyers Choose 30-Year Terms Later in Life

Opting for a 30-year term is often a strategic move for those entering their retirement years. While a shorter term might seem appealing to clear debt quickly, the 30-year path offers the most lift for your monthly budget. By spreading the repayment over three decades, you keep your monthly obligations at their lowest possible point. This preserves your liquidity, allowing you to use your retirement savings for travel, healthcare, or supporting family rather than tying it all up in housing costs.

In Michigan, where the median home price saw a 4.0% increase in March 2026 compared to the previous year, building equity remains a sound investment. A 30-year Purchase Mortgage or a Refinance Mortgage allows you to benefit from this appreciation while maintaining a predictable, low-stress payment. It’s about control. You have the freedom to pay more toward the principal if you choose, but you aren’t locked into a high-pressure monthly commitment that could cause financial turbulence during your retirement years.

How Lenders Evaluate Borrowers Over 60: Stability Over Age

When you prepare for a home loan, think of the lender as a flight engineer. They aren’t concerned with how many years you’ve been flying; they’re looking at the health of your engine and the depth of your fuel reserves. If you’ve been asking am I too old to get a 30-year mortgage in Michigan, it’s helpful to understand that underwriters prioritize stability over a birth date. In 2026, Michigan lenders focus on your Debt-to-Income (DTI) ratio as the primary instrument for navigation. This ratio measures your monthly debt obligations against your gross monthly income to ensure you have enough lift to cover a new mortgage payment without straining your retirement lifestyle.

Credit score requirements remain a vital part of the pre-flight check. For most Conventional Mortgage options in Michigan, a score of 620 is the baseline, though a score above 740 often unlocks the most favorable rates. While your income source might change as you transition away from a traditional career, your credit history serves as a record of your reliability. A seasoned credit profile can actually make your application more attractive, proving to the bank that you’ve managed financial commitments successfully over many decades.

Calculating Income from Retirement Accounts

Transitioning to retirement income doesn’t mean losing your qualifying power. Lenders view Social Security and fixed pensions as high-quality fuel because they are incredibly reliable. When using a Purchase Mortgage framework, we also look at your Required Minimum Distributions (RMDs) from 401(k) or IRA accounts. As long as you can show these distributions will continue for at least three years after your loan closes, they count toward your qualifying income. This “3-year rule” is a standard safety protocol used to ensure your financial flight path remains stable through the early years of the mortgage.

The Role of Assets in Your Loan Approval

Sometimes, a high net worth can provide the necessary momentum even if your monthly pension seems modest. Underwriters can use “asset depletion” strategies to help you qualify. This involves calculating how much monthly income your total nest egg could theoretically provide over the life of the loan. Earned income represents wages from active employment, while passive retirement income encompasses distributions from Social Security, pensions, and investment accounts that flow steadily without the need for daily labor. By converting your savings into a recognized income stream, you can often secure a larger loan than your Social Security check alone would suggest. If you’re ready to see how your specific assets can help you qualify, speaking with a local mortgage expert can help clarify your options.

Strategic Advantages and Risks of a 30-Year Mortgage in Retirement

Deciding to carry a mortgage into your sunset years is a strategic choice that requires a steady hand on the controls. While the legal answer to am I too old to get a 30-year mortgage in Michigan is a clear “no,” the financial answer depends on your specific goals. A 30-year term acts as a stabilizer for your monthly budget. It ensures that your fixed income isn’t swallowed by housing costs, leaving you with enough fuel for leisure, travel, or unexpected home repairs. Inflation also works in your favor here. You’re essentially paying back your loan with future dollars that may have less purchasing power, while your property value in the Michigan market continues to build equity.

There’s also the benefit of the mortgage interest deduction, which remains a relevant factor for many Michigan taxpayers in 2026. For many retirees, the true risk isn’t the debt itself, but the danger of being “house rich and cash poor.” Tying up your entire net worth in bricks and mortar leaves you with no emergency landing strip if life throws a curveball. A 30-year mortgage keeps your assets liquid and accessible, providing a level of financial maneuverability that an all-cash purchase simply can’t match.

Liquidity vs. Home Equity

Maintaining a healthy cash reserve often outperforms owning a home outright, especially if your retirement accounts are earning a steady return. If your investments are growing at a rate that exceeds your loan’s interest, you’re effectively flying with a tailwind. Before you decide to liquidate your 401(k) to buy a home, it’s wise to review the current mortgage rates in Kalamazoo. If the spread between your investment growth and the cost of debt is favorable, keeping that cash in the market provides a much safer safety margin than a paid-off house you can’t easily spend during an emergency.

The Reality of Interest Costs Over 30 Years

Some borrowers worry about the total interest paid over three decades. It’s true that a longer flight path requires more total fuel in the form of interest payments, but it offers the maximum amount of flexibility. Many Michigan seniors choose the 30-year term for the low mandatory payment but choose to pay it off like a 15-year loan whenever they have extra funds. This gives you a manual override; you can accelerate the payoff during years with high investment returns and throttle back to the minimum payment if your medical expenses or other costs rise. Managing the psychological weight of debt is a personal journey, but having the option to lower your overhead is a powerful tool for long-term peace of mind.

Alternatives to the Traditional 30-Year Term for Michigan Seniors

While the 30-year term is a fantastic stabilizer for many, it isn’t the only runway available for your retirement. If you’ve spent years asking, am I too old to get a 30-year mortgage in Michigan, you’ll be glad to know that the runway is wide open. However, your specific destination might require a different type of engine. For homeowners who want to modify their current residence to accommodate changing physical needs, a standard loan isn’t always the best fit. You might instead consider a Renovation Mortgage. This tool allows you to finance essential safety upgrades, like walk-in tubs or ramp access, ensuring you can age in place with dignity and comfort without depleting your savings.

The Family Opportunity Mortgage Explained

One of the most powerful, yet underutilized, tools in our Michigan market is the Family Opportunity Mortgage. This program allows adult children to purchase a primary residence for their elderly parents who may not have the traditional income to qualify on their own. The beauty of this flight plan is that it secures “primary residence” interest rates, which are typically lower than investment property rates. It’s a neighborly way to keep the family close while ensuring your parents have a safe, high-quality home. If your goals are more about building a real estate portfolio than housing a family member, you can explore our DSCR Loan Guide for investment-focused strategies.

15-Year vs. 30-Year: Which Flight Path is Yours?

Choosing between a 15-year and a 30-year term is a matter of balancing speed and comfort. As of May 20, 2026, the average 15-year fixed mortgage rate in Michigan sits at 5.88%, which is notably lower than the 30-year average of 6.74%. A 15-year term is a high-performance engine that burns through debt quickly, saving you thousands in interest over the life of the loan. It’s an excellent choice if you plan to retire in the next decade and want to enter that phase of life with full ownership.

However, the 30-year term remains the safest path for preserving monthly cash flow. You can always pay more toward your principal when you have the extra funds, giving you manual control to reach clear skies on your own timeline. Navigating the “break-even” point is easier when you have a seasoned guide to help you compare the long-term interest savings against your current liquidity needs. If you’re ready to explore these specialized flight paths, our team is here to help you find the right fit for your family’s future.

Navigating Your Late-Career Mortgage with a Local Expert

Choosing a mortgage in your sixties or seventies requires more than just a standard application; it requires a seasoned navigator who understands the specific landscape of the Michigan housing market. National call centers often treat borrowers like data points on a spreadsheet, missing the nuance of a life well-lived. They might see your retirement as a risk, but a local expert sees it as a period of hard-earned stability. When you ask, am I too old to get a 30-year mortgage in Michigan, you deserve an answer that accounts for the local “weather patterns” in Kalamazoo and Portage. Local lenders understand our regional property values and the specific ways Michigan taxes and insurance impact your long-term flight plan.

Jeremy Drobeck – Treadstone Mortgage specializes in these complex pre-flight checks. We believe that your experience is an asset, not a hurdle. By focusing on individualized care, we help you prepare for a smooth landing in your new home. This involves looking beyond the surface-level numbers to find the most efficient way to use your Social Security, pensions, and investment accounts. Our goal is to ensure your mortgage provides the necessary lift for your lifestyle without creating unnecessary turbulence in your retirement years.

The Treadstone Difference: Professional Authority, Neighborly Care

We don’t view a home purchase as a cold transaction. It’s a significant life milestone that requires careful handling and empathy. Our commitment to you includes end-to-end support throughout the entire duration of your loan. You won’t be passed off to a different department once the papers are signed; Jeremy Drobeck – Treadstone Mortgage remains your steady ally from the initial consultation to the moment you get your keys. This partnership-based relationship is designed to lower the high-stress barriers of lending, replacing anxiety with the calm confidence that comes from expert guidance. We take pride in building a flight plan that respects your history while securing your future.

Next Steps for Your Michigan Home Journey

Preparation is the key to a successful departure. To begin your journey, you’ll want to gather the specific documents that prove your financial altitude. This typically includes your Social Security award letters and recent pension statements. We’ll also help you review your asset depletion options to see if your 401(k) or other “fuel reserves” can be used to strengthen your qualifying power. Our team will perform a detailed DTI check to ensure your monthly payments remain well within your comfort zone.

- Gather your Social Security and pension award letters for 2026.

- Organize your 401(k) or IRA statements to review RMD schedules.

- Identify your target Michigan neighborhood to calculate accurate property taxes.

- Schedule a one-on-one session to map out your debt-to-income ratio.

Ready to start your journey? Connect with Jeremy Drobeck – Treadstone Mortgage today for a personalized mortgage flight plan.

Your Future Flight Plan Starts Here

Your age is a reflection of your experience; it’s not a limit on your potential for homeownership. Federal and Michigan laws ensure your path remains open, focusing on your financial stability rather than the date on your birth certificate. By utilizing 30-year terms, you can maintain the liquidity needed to enjoy your retirement without sacrificing the security of a permanent home. It’s about maintaining control over your cash flow while building equity in a home that fits your lifestyle.

The question am I too old to get a 30-year mortgage in Michigan is a hurdle we help you clear with ease. Whether you’re looking at a Purchase Mortgage for a new residence or considering a Refinance Mortgage to lower your monthly overhead, the right strategy is about precision. Jeremy Drobeck – Treadstone Mortgage has served as a steady, reliable navigator in the Kalamazoo and Portage markets since 2002. As an expert in MSHDA and senior lending strategies, the team provides the professional authority and neighborly care you need for a smooth landing.

Schedule Your Personal Mortgage Flight Plan with Jeremy Drobeck – Treadstone Mortgage to secure your future today. You’ve earned this milestone. We’re here to help you reach it with total confidence.

Frequently Asked Questions

Can a bank deny me a 30-year mortgage because I’m 75?

No, a lender cannot legally deny your application based on your age. Federal laws and Michigan’s Elliott-Larsen Civil Rights Act prohibit age discrimination in housing and financing. If you are asking, am I too old to get a 30-year mortgage in Michigan, the answer is that your credit score and income stability are the only factors that matter. We focus on your ability to repay the loan rather than the number of years on your birth certificate.

How do lenders calculate Social Security income for a mortgage?

We typically “gross up” Social Security income by 125% because it is often non-taxable. This adjustment provides extra lift to your qualifying power, reflecting your true spending capacity. For example; if you receive $2,000 monthly, we may count it as $2,500 for your Debt-to-Income calculation. This ensures your retirement benefits are valued fairly during the underwriting process, making it easier to secure a Purchase Mortgage or Refinance Mortgage.

Is it better for a senior to get a 15-year or 30-year mortgage in Michigan?

It depends on whether you value speed or comfort. A 15-year term offers a faster route to full ownership and lower interest rates, which averaged 5.88% in Michigan in May 2026. However, a 30-year term provides the most stability for your monthly cash flow. Many seniors choose the 30-year path to keep their mandatory obligations low, allowing them to manually accelerate payments only when their budget has extra room.

What is a Family Opportunity Mortgage and how does it help seniors?

This specialized program allows adult children to purchase a home for their elderly parents while benefiting from “primary residence” interest rates. It’s an excellent tool for families who want to keep parents nearby without the high costs of investment property financing. This arrangement provides professional-grade financing and stability for the parents, ensuring they have a safe, high-quality home in a community they love, like Kalamazoo or Portage.

Do I need a larger down payment if I am a retiree?

No, retirees are subject to the same down payment requirements as any other borrower. You can secure a Conventional Mortgage with as little as 3% down or an FHA Mortgage with 3.5% down. If you are a veteran, you might even qualify for a VA Mortgage with 0% down. Your retirement status doesn’t change the engine mechanics of the loan; it only changes how we verify the fuel in your tanks.

What happens to the mortgage if the borrower passes away before the 30-year term ends?

The mortgage remains tied to the property, and the responsibility usually passes to your estate or your heirs. They can choose to keep the home and continue making payments, sell the property to pay off the balance, or refinance the debt. Federal law protects family members, allowing them to take over the existing mortgage without a credit check in many cases. This ensures a smooth transition and prevents the flight from being grounded.

Can I use my 401(k) or IRA assets to qualify for a mortgage in Michigan?

Yes, your retirement accounts are valuable fuel reserves for your loan application. We can use your Required Minimum Distributions (RMDs) as steady income or employ an “asset depletion” strategy. This method converts your total nest egg into a monthly income figure for the bank to see. As long as we can verify these distributions will continue for at least 36 months after closing, they provide significant lift to your qualifying power.

Are there special Michigan first-time home buyer programs for seniors?

Yes, the MSHDA Down Payment Assistance program is available to any Michigander who hasn’t owned a home in the last three years. This includes seniors who are re-entering the market or moving to a new area. MSHDA provides a steadying force by helping cover closing costs, which can range from 2% to 5% of the purchase price. We are experts in navigating these state-specific programs to help you find the most efficient path to your new front door.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”