Renovation Loans in Kalamazoo, MI: Your 2026 Home Transformation Flight Plan

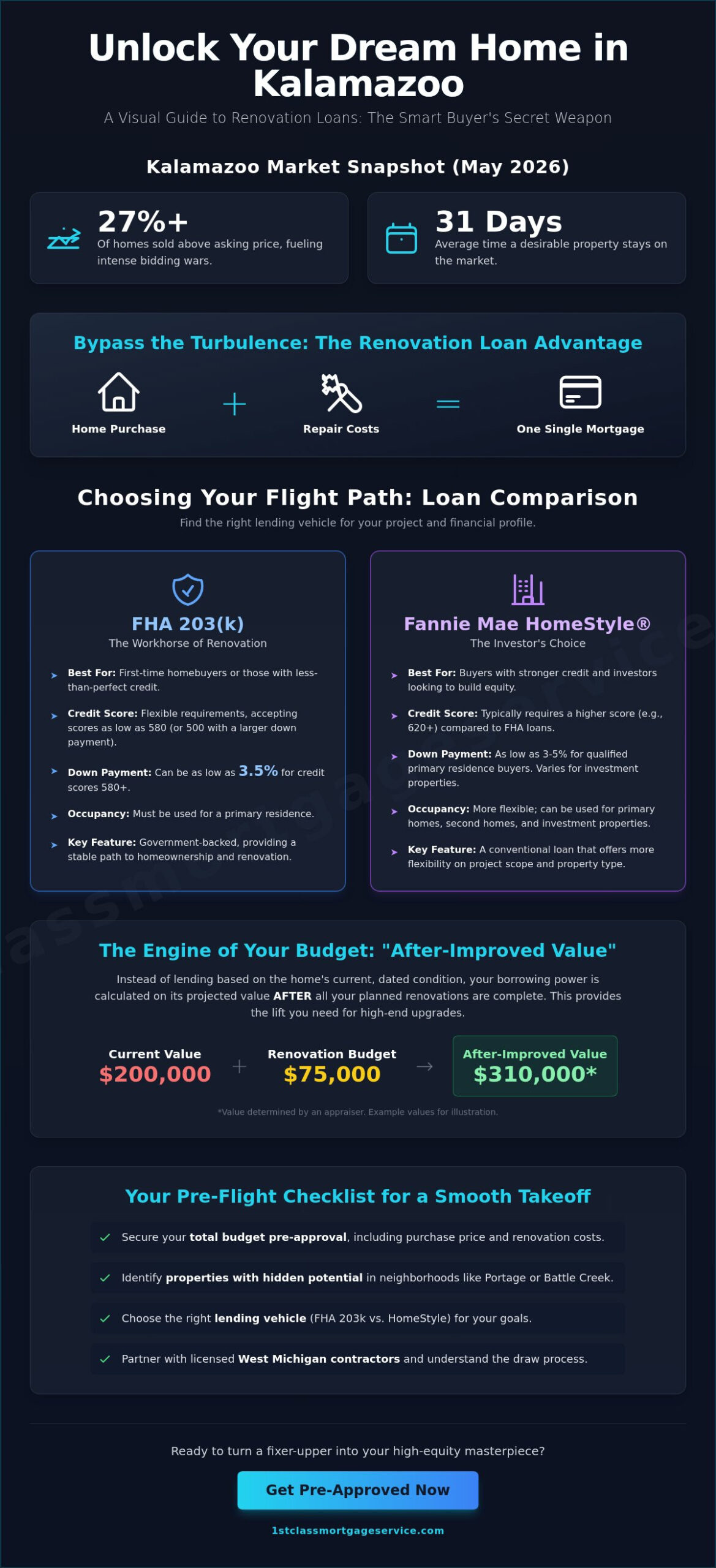

Why join the frantic scramble for a “turnkey” home in Winchell or the Stuart Neighborhood when you can engineer your own masterpiece from the ground up? In May 2026, with over 27% of Kalamazoo County homes selling above asking price, the traditional path to homeownership often feels like flying into a headwind. You’ve likely noticed that the most desirable properties are gone in an average of 31 days; this leaves many qualified buyers grounded. However, renovation loans Kalamazoo MI act as a tactical navigation tool. They allow you to secure a fixer-upper and the funds to modernize it using one simple monthly payment.

We understand that the thought of managing bank draws and licensed contractors can feel like navigating through heavy turbulence. It’s natural to feel torn between the flexible 3.5% down payment of an FHA 203(k) and the investment potential of a Fannie Mae HomeStyle loan. This flight plan simplifies those complexities; we’ll show you how to turn a dated property into a high-equity asset. You will discover how to choose the right lending vehicle, manage the appraisal process based on after-improved value, and finally gain the lift you need to land in the home you’ve always envisioned.

Key Takeaways

- Learn how to combine your home purchase and repair costs into a single mortgage, bypassing the turbulence of bidding wars on move-in ready homes.

- Compare different flight paths like the FHA 203(k) and Fannie Mae HomeStyle to find the right fit for your credit score and project scope.

- Discover how renovation loans Kalamazoo MI utilize an “after-improved value” appraisal to provide the lift needed for high-end upgrades in local neighborhoods.

- Master the logistics of working with West Michigan contractors, including how to manage the draw process and ensure milestones are reached safely.

- Follow a practical checklist for takeoff, from securing your total budget pre-approval to identifying properties with hidden potential in Portage or Battle Creek.

Why Renovation Loans are the Secret Weapon for Kalamazoo Homebuyers

A renovation loan is a specialized financial tool that fuels your home purchase and your remodeling budget in a single closing. Instead of scrambling for separate financing, you secure one mortgage based on what the home will be worth after the work is finished. In the current 2026 market, renovation loans Kalamazoo MI serve as a vital bypass for the inventory turbulence we see in Portage and Battle Creek. While other buyers are stuck in high-altitude bidding wars over move-in ready homes, you can focus on properties that others overlook. This approach lets you build instant equity in historic districts like the Stuart Area or Winchell, turning a tired house into a customized masterpiece.

Choosing this path also provides a significant financial safety net. You won’t need to rely on high-interest credit cards or personal loans to fix a leaky roof or modernize a kitchen. Everything is bundled into one predictable monthly payment. This streamlined process ensures your renovation funds stay protected in an escrow account, only being released as your contractor hits specific milestones. It’s a controlled, engineered way to manage a complex project without the stress of out-of-pocket surprises. You don’t have to worry about running out of cash halfway through the build.

The Kalamazoo Market Advantage in 2026

Our local housing stock in West Michigan is rich with character but often requires mechanical or aesthetic updates to meet modern standards. In 2026, viewing these older homes as “diamonds in the rough” is a strategic necessity. By utilizing renovation loans Kalamazoo MI, you can essentially outmaneuver the competition by seeing value where others see work. You can outmaneuver the competition. These programs provide the lift needed to afford upgrades in rising neighborhoods where property values are climbing steadily. By looking past peeling paint or dated floor plans, you can secure a footprint in a desirable area that might otherwise be out of reach.

Renovation vs. Traditional Purchase Mortgages

The fundamental difference lies in how your borrowing power is calculated. A standard purchase mortgage only considers the home’s current state, which often leaves buyers cash-poor after addressing immediate repairs. In contrast, renovation programs look at the “after-improved value.” This is a common feature of an FHA insured loan, specifically the 203(k) program, which allows you to finance the repairs into the loan itself. This structure provides a steady flight path, ensuring you have the capital to finish the job right the first time without depleting your personal savings.

FHA 203(k) vs. Fannie Mae HomeStyle: Choosing Your Flight Path

Selecting the right loan product is like choosing the correct aircraft for your journey. You need enough power to reach your destination without carrying unnecessary weight. In the competitive landscape of renovation loans Kalamazoo MI, two primary flight paths dominate the horizon: the government-backed FHA 203(k) and the conventional Fannie Mae HomeStyle. Your choice depends on your credit score altitude, the structural complexity of your project, and whether you intend to live in the home or use it as a wealth-building asset.

Each program has specific mechanical requirements that determine your eligibility. While both allow you to wrap repair costs into your primary mortgage, they cater to different financial profiles. It’s about finding the right balance of stability and flexibility. Whether you’re a first-time buyer in a historic Kalamazoo neighborhood or an experienced investor in Portage, understanding these nuances ensures a smooth takeoff.

The FHA 203(k): The Workhorse of Renovation

If your credit history has experienced some turbulence, the FHA 203(k) offers a stable way to gain lift. You can secure financing with a credit score as low as 580 while only requiring a 3.5% down payment. For those with scores between 500 and 579, a 10% down payment is necessary. The 203(k) Rehabilitation Mortgage Insurance Program is divided into two distinct categories based on your project scope.

The “Limited” version is designed for cosmetic updates and non-structural repairs, typically covering up to $35,000 in improvements. It’s perfect for new flooring, kitchen cabinets, or energy-efficient windows. If your vision involves moving walls, adding a second story, or fixing a foundation, you’ll need the “Standard” 203(k). This version requires a HUD consultant to oversee the plan, ensuring the project stays on course from takeoff to landing.

Fannie Mae HomeStyle: The Conventional Alternative

Borrowers with a credit score of 620 or higher often find better conditions with a Fannie Mae HomeStyle loan. This conventional option typically offers lower monthly mortgage insurance costs for those with stronger credit profiles. While first-time buyers can enter with as little as 3% down through the HomeReady program, the standard requirement for most borrowers is 5%.

HomeStyle offers more flexibility for “luxury” items that the FHA might restrict. If you want to install a permanent outdoor kitchen or professional landscaping in a Portage backyard, this is your best route. It’s also a powerful tool for building a portfolio. It allows for second homes and investment property mortgage scenarios that government programs won’t cover. Many Michigan residents also find success by pairing these loans with MSHDA down payment assistance. If you’re ready to see which path fits your specific financial coordinates, you can review our current mortgage programs to find your perfect match.

How the ‘After-Improved Value’ Appraisal Powers Your Budget

The engine of your home transformation is the “After-Improved Value” (AIV) appraisal. Most mortgages only look at what a property is worth in its current state. However, renovation loans Kalamazoo MI use a forward-looking metric. They calculate the loan amount based on the projected value of the home once all renovations are finished. This approach allows you to access significantly more capital than a traditional loan would permit. It’s the difference between financing a small propeller plane and a long-range jet.

This future-value concept provides the lift you need to tackle major projects. To understand the mechanics of this process, many buyers ask, “What Is An FHA 203(k) Loan?” and how it differs from a standard mortgage. The appraiser reviews your renovation plans alongside comparable homes in Kalamazoo that have already been modernized. By analyzing these “after-repair” comps, the lender can justify a higher loan amount that covers both the purchase price and the construction costs.

The HUD Consultant: Your Project Navigator

For more complex projects, you’ll need a seasoned navigator to ensure the flight path remains clear. The HUD Consultant serves as a mandatory project auditor for Standard 203k loans, ensuring every repair meets safety and regulatory standards. They perform a feasibility study to confirm that your renovation dreams align with your actual budget. This professional doesn’t just check boxes; they act as your advocate by identifying potential mechanical issues before they become expensive mid-flight emergencies. Their expertise ensures that your investment in a historic Stuart Area home is structurally sound and financially viable.

Drafting the Contractor Bid for Success

Your contractor’s bid is the fuel for this entire process. Vague ballpark estimates cause immediate turbulence during the underwriting stage. A precise, line-item bid ensures every nail, board, and hour of labor is accounted for to maximize your appraisal value. Our team reviews these bids meticulously to ensure they meet 2026 lending standards and provide enough detail for the appraiser to see the full scope of the value you’re adding. When the documentation is disciplined and transparent, the path to approval is much smoother.

Sometimes the appraisal altitude doesn’t reach your expected height. If the AIV comes in lower than the combined cost of the purchase and repairs, we don’t just abandon the journey. We work with you to refine the renovation scope or identify higher-ROI upgrades that provide better lift. This flexibility is part of our commitment to being your steady ally throughout the entire process. We help you adjust the flight plan so you can still land safely in your dream home.

The Local Runway: Finding Contractors and Managing the Build

Once your financing is cleared for takeoff, your focus shifts to the local runway: the actual construction phase. Managing a renovation is a disciplined process that requires a reliable crew and a clear schedule. In West Michigan, finding the right builder is about more than just aesthetic taste. It’s about technical proficiency with renovation loans Kalamazoo MI. These projects have specific documentation requirements that differ from standard cash-and-carry remodels. You need a partner who understands how to navigate the paperwork as well as they navigate a job site.

The transition from closing day to the final walkthrough involves several moving parts. It’s a journey that requires patience and precision. While the bank handles the capital, your contractor handles the transformation. Keeping these two forces in sync is what ensures a smooth flight. We remain present as your steady ally, helping you monitor progress and manage expectations throughout the build.

Working with Kalamazoo-Area Contractors

Experience with rehab loans is a specialized skill set. You should vet every potential builder for their licensing and insurance status. In Michigan, any residential construction or remodeling project valued at $600 or more requires a state license. Don’t be afraid to ask direct questions before they step onto your Kalamazoo property. Ask about their previous experience with FHA or Fannie Mae draws. A contractor who is comfortable with lender-monitored milestones will keep your project on schedule and under budget. This relationship is the engine of your home transformation; transparency is non-negotiable.

Understanding the Draw Schedule

The draw schedule is the mechanical system that releases funds from your escrow account. Unlike a traditional remodel where you might pay a large deposit upfront, renovation loans protect you by paying in stages. Contractors only receive payment after specific milestones are reached and verified by an inspector. This ensures the work meets quality standards before the capital is released. It’s a safety feature that keeps everyone aligned and moving toward the final walkthrough. Contractors don’t get all the money upfront, which provides the necessary leverage to ensure the project reaches the finish line.

We also build a 10-20% contingency reserve into every loan. This safety buffer is essential when working with Kalamazoo’s historic housing stock, where hidden issues can occasionally appear once walls are opened. If these funds aren’t used, they are typically applied back to your principal balance. If you’re ready to start vetting your project and assembling your team, you can apply for a renovation mortgage today to establish your total budget.

Preparing for Takeoff: Your Renovation Loan Checklist

You’ve mapped the mechanics of the appraisal and selected your preferred loan product. Now it’s time for the final pre-flight inspection. Successfully utilizing renovation loans Kalamazoo MI requires a sequenced approach that ensures every component of your project is airworthy before you leave the tarmac. This checklist serves as your final navigation guide to move from the vision phase into active construction. By following a disciplined schedule, you replace the anxiety of the unknown with the confidence of a well-engineered plan. We’re here to ensure you don’t miss a single detail during this critical preparation phase.

The journey from a “fixer-upper” to a move-in ready masterpiece is a significant life milestone. It requires preparation, precision, and a steady ally who remains present throughout the entire process. As you move through these final steps, remember that the goal isn’t just a house; it’s the creation of a home that fits your life perfectly. Each step in this checklist provides the stability and lift needed for a successful project completion in our unique West Michigan landscape.

The Pre-Approval Engine

A standard pre-approval often fails to account for the added complexity of a renovation mortgage because it doesn’t factor in the future value of the property. You need an engine that calculates your total buying power, including both the acquisition cost and the repair budget. This step establishes your maximum altitude. It prevents you from falling in love with a property that exceeds your financial limits once the renovation costs are added. Contacting Jeremy Drobeck – Treadstone Mortgage is the best way to start your specific Kalamazoo flight plan. He provides the expert guidance needed to calibrate your budget for the 2026 market.

- Find the Property: Look past the superficial flaws like peeling paint in Battle Creek or outdated kitchens in Portage. Focus on the structural integrity and the potential of the neighborhood.

- Secure Your Contractor: Your builder must provide a detailed, line-item bid. This document is the fuel for your appraisal and ensures the lender understands the full scope of your “after-improved” value.

- The Appraisal & Underwriting: This is the final navigation check. The lender reviews the projected valuation and your financial profile to ensure the flight path is clear for closing.

- Closing & Construction: Once the papers are signed, you move from the tarmac to the sky. Your renovation begins, and funds are released according to your established draw schedule.

Final Checklist for a Smooth Landing

Before you reach the sky, ensure your documentation is in order for the 2026 lending environment. This includes tax returns, pay stubs, and the detailed contractor bid we’ve emphasized throughout this guide. You should also confirm your MSHDA Down Payment Assistance eligibility if you’re a first-time buyer in Michigan. These programs provide the extra stability needed for a successful landing. If you’re ready to stop searching for the perfect home and start building it, we’re ready to help you navigate. Ready to renovate? Schedule your Kalamazoo consultation today!

Your Destination is Within Reach

The path to your dream home in West Michigan doesn’t have to be a gamble against high-competition inventory. You’ve discovered how to bypass bidding wars by focusing on a property’s potential rather than its current state. By utilizing the “after-improved value” of a home, you gain the lift needed to modernize older properties while building instant equity. Whether you choose the stability of an FHA 203(k) or the flexibility of a Fannie Mae HomeStyle loan, you’re no longer grounded by what is currently move-in ready.

Successfully navigating renovation loans Kalamazoo MI requires a steady ally who understands the local landscape from Portage to the Stuart neighborhood. Jeremy Drobeck – Treadstone Mortgage provides the seasoned expertise and personalized support required to handle everything from your initial pre-approval to the final contractor draw. You don’t have to manage this complex journey alone. Our team is committed to your success at every altitude of the process. Start Your Kalamazoo Renovation Flight Plan with Jeremy Drobeck – Treadstone Mortgage and take the first step toward your home’s transformation today. Your masterpiece is waiting for its final approach.

Frequently Asked Questions

Can I do the renovation work myself to save money?

Generally, you cannot perform the renovations yourself. Most lenders require that all work be completed by licensed and insured contractors to ensure the property meets safety standards and protects the home’s value. While some programs have very limited “self-help” options, the restrictions are usually so strict that hiring a professional is the most stable path for a successful project.

What is the maximum amount I can borrow for renovations in Kalamazoo?

Your maximum loan amount depends on the specific program and the 2026 lending limits for Kalamazoo County. For an FHA 203(k) loan, the single-family limit in our area is $541,287. Conventional HomeStyle loans allow for a higher ceiling with a conforming limit of $806,500. Your total budget includes the purchase price and the renovation costs combined into one mortgage.

How long does it typically take to close on a renovation loan?

You should plan for a closing timeline of 45 to 60 days. This duration is longer than a standard purchase because it requires extra steps like contractor vetting and a specialized appraisal. We act as your navigator during this period, ensuring all paperwork and inspections stay on schedule so your flight to homeownership remains on course.

Can I use a renovation loan to buy a foreclosed property in Portage?

Yes, these loans are ideal for purchasing foreclosed or distressed properties that might not qualify for traditional financing. Because the loan is based on the home’s future value, you can secure a property in Portage that needs significant repair. This allows you to stabilize a “diamond in the rough” and turn it into a high-equity asset immediately.

Are there specific credit score requirements for Michigan renovation loans?

You typically need a minimum credit score of 580 for an FHA 203(k) or 620 for a conventional HomeStyle mortgage. Your credit score serves as an altimeter for your interest rate; higher scores generally provide more lift with lower monthly costs. We help you review your financial coordinates to determine which flight path offers the most stability for your specific situation.

What happens if the renovation costs end up being higher than the original bid?

We build a mandatory contingency reserve of 10% to 20% into your loan budget to handle unexpected cost overruns. This safety buffer ensures that if your contractor discovers hidden issues, you have the capital to address them without stalling the project. If these funds aren’t used by the time of the final walkthrough, they are typically applied to your principal balance.

Can I include new appliances in my renovation loan budget?

Yes, you can include appliances as part of your renovation budget if they are permanent fixtures in a larger remodel. This is a great way to modernize your kitchen while keeping all your expenses under one monthly payment. It’s important to finalize these selections during the bidding phase so they are included in the appraiser’s final valuation of the property.

Is a renovation loan better than a Home Equity Line of Credit (HELOC)?

A renovation mortgage is usually the superior choice for a new purchase because it provides capital based on the home’s future value. A HELOC requires you to already have significant equity in the property, which isn’t possible when you’re just buying a fixer-upper. Renovation loans Kalamazoo MI allow you to create that equity from day one rather than waiting years to build it.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”