DSCR Loan Requirements 2026: The Investor’s Pre-Flight Checklist

What if your personal tax returns weren’t the deciding factor for your next rental property? It’s a common frustration for Michigan investors who find their growth grounded by the strict dscr loan requirements and debt-to-income ratios of traditional banking. You know your rental math works, yet the heavy documentation feels like it’s keeping you stuck on the tarmac. At Jeremy Drobeck – Treadstone Mortgage, we believe your portfolio deserves more lift and less red tape.

Success also depends on the type of aircraft you’re flying. Standard single-family rentals (SFR) are the easiest to clear for departure, but 2-4 unit properties and larger multi-family buildings are also eligible. Each property type has its own nuances, but the goal remains the same: steady cash flow. Unlike some forms of commercial real estate financing that might focus on a business’s global cash flow—such as the nationwide structured financing provided by Allstate Capital Group—a DSCR loan keeps its eyes fixed on the specific rental income of the subject property. This specialized focus is what allows you to scale your portfolio beyond the limits of traditional banking.

In this guide, you’ll learn how to master these specific metrics so you can qualify based solely on property performance. With interest rates for domestic investors currently ranging from 6.125% to 9.125%, knowing the exact flight path to a 1.25 ratio is essential for scaling your wealth. We’ll preview the credit benchmarks, the 20% down payment standards, and the 3 to 6 months of liquid reserves needed to keep your investment journey airborne. Whether you’re targeting a $236,274 single-family home in Kalamazoo or a multi-unit in Battle Creek, this checklist ensures a smooth landing for your next deal.

Key Takeaways

- Discover how to scale your portfolio without the burden of personal income tax returns by qualifying solely on property cash flow.

- Master the specific dscr loan requirements for 2026, including the credit score benchmarks and debt coverage ratios needed for a successful takeoff.

- Learn to calculate your property’s “lift” using the PITI plus HOA formula to ensure your rental math meets lender standards.

- Compare the scalability of DSCR loans against the 10-loan conventional limit to find the right aircraft for your long-term investment goals.

- Gain a local advantage in the Kalamazoo and Portage markets by partnering with a seasoned co-pilot who understands the nuances of Michigan real estate.

Understanding DSCR Loans: The Investor’s Flight Path to 2026 Growth

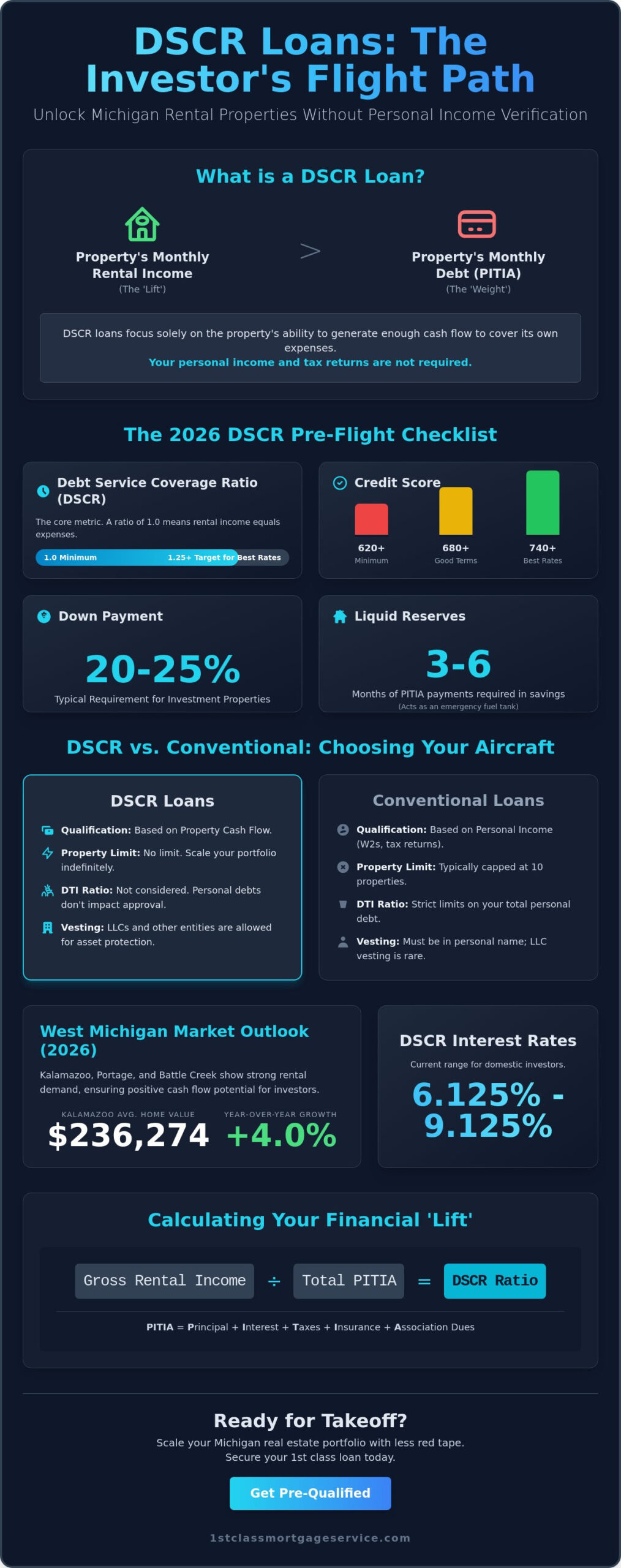

Scaling a real estate portfolio requires more than just a good eye for property; it requires the right financial engine. For years, investors hit a ceiling when their personal debt-to-income ratios became too heavy for traditional banks to handle. The core of this program is the Debt Service Coverage Ratio (DSCR), a mathematical calculation that measures if a property’s rental income can comfortably pay its monthly mortgage obligations. It is the primary metric for investor lift, shifting the focus from your personal bank account to the property’s actual cash flow.

Lenders classify these as Non-QM or “Investor Cash Flow” loans. They don’t follow the rigid flight plan set by federal agencies. This means you don’t have to provide years of tax returns or proof of personal income to qualify. If the property’s rent covers the mortgage, taxes, and insurance, you’re usually cleared for takeoff. As we move through 2026, this shift from “personal income” to “property income” qualification has become the standard for investors who want to move fast without the baggage of traditional documentation. For a comprehensive overview of how these programs work in Michigan, the DSCR loan guide for Michigan real estate investors in 2026 breaks down every requirement you need to know before applying.

Why Investors Choose Non-QM over Conventional Financing

Conventional loans often ground investors once they reach the 10-property limit. It’s a hard cap that stops many portfolios mid-flight. DSCR loans remove this barrier, allowing you to scale indefinitely. Because these loans don’t use a Debt-to-Income (DTI) constraint, your personal car payments or primary mortgage won’t block your next investment purchase. Additionally, meeting dscr loan requirements allows for LLC vesting. This is a critical safety feature for professional investors who want to protect their personal assets while growing their business, a luxury rarely found in the conventional world.

The 2026 Market Outlook for West Michigan Investors

The landscape in West Michigan remains a prime runway for growth. As of March 31, 2026, Kalamazoo’s average home value hit $236,274, marking a steady 4.0% increase over the previous year. In Portage and Battle Creek, rental demand continues to outpace supply. This demand is vital because it ensures your DSCR math stays positive even with current interest rates.

With DSCR rates for domestic investors currently ranging from 6.125% to 9.125%, the “break-even” ratio is tighter than it was three years ago. Lenders now typically look for a ratio of 1.25 to offer the most competitive pricing, though a 1.0 ratio is often the baseline for approval. DSCR loans act as the extra lift your portfolio needs to bypass the turbulence of personal income limits and reach higher altitudes of wealth. We’re here to help you navigate these numbers and ensure your investment strategy stays airborne in this competitive Michigan market.

The 2026 DSCR Loan Requirements: Your Pre-Flight Checklist

Before any pilot pushes the throttle for takeoff, they run through a rigorous pre-flight checklist. Your investment journey in West Michigan is no different. Meeting the dscr loan requirements in 2026 isn’t about proving how much you earn at your day job. Instead, it’s about proving that both you and the property are ready for the journey. Lenders typically require a solid baseline of 3 to 6 months of liquid reserves. These reserves, covering Principal, Interest, Taxes, Insurance, and Association dues (PITIA), act as your emergency fuel tank if a tenant vacates unexpectedly. This safety margin ensures you can maintain the property without mid-flight stress.

Success also depends on the type of aircraft you’re flying. Standard single-family rentals (SFR) are the easiest to clear for departure, but 2-4 unit properties and larger multi-family buildings are also eligible. Each property type has its own nuances, but the goal remains the same: steady cash flow. Unlike some forms of commercial real estate financing that might focus on a business’s global cash flow, a DSCR loan keeps its eyes fixed on the specific rental income of the subject property. This specialized focus is what allows you to scale your portfolio beyond the limits of traditional banking.

Credit Score and Down Payment Minimums

In 2026, your credit score acts as the “flaps” on your wings. A higher score allows for a shorter runway, meaning a lower down payment. While some programs allow for a FICO as low as 620, most investors aim for a 660 to 680 floor to secure better terms. If you want the most efficient lift, a score of 740 or higher unlocks the lowest rates and maximum leverage. Expect to bring a 20% to 25% down payment to the closing table. This equity stake provides the stability needed to keep the investment airborne through market shifts. If you’re unsure where your current score lands, you can explore your options with a quick consultation to see which program fits your goals.

Property Eligibility and Appraisal Standards

Not every property is cleared for the DSCR flight path. Lenders prefer “warrantable” condos and standard residential builds. You might encounter turbulence with rural properties, unique “hobby” farms, or non-warrantable condos that don’t meet specific investor ratios. The most critical document in this process is the appraisal, specifically the 1007 Rent Schedule. A professional appraiser doesn’t just look at the home’s value; they determine the “fair market rent” based on local Kalamazoo or Portage data. If the appraiser’s rent estimate doesn’t meet the dscr loan requirements, the loan may need a larger down payment to balance the math. We work closely with you to review these numbers early, ensuring your property is ready for a smooth landing.

Calculating Your Ratio: How Lenders Measure Your Financial Lift

The math behind your mortgage shouldn’t feel like a guessing game. While conventional lenders obsess over your personal paystubs, DSCR lenders look at the property’s ability to generate its own lift. To meet dscr loan requirements, you must understand how a lender calculates your Debt Service Coverage Ratio. It’s a simple division problem, but the components within the denominator can make or break your approval. By working with experienced investment property mortgage lenders, you can ensure your “flight math” is accurate before you ever submit an application.

The DSCR Formula: Navigating the Numbers

The basic formula is Gross Rental Income divided by Total Debt Service. In this context, “Total Debt Service” includes your Principal, Interest, Taxes, and Insurance (PITI), along with any mandatory Homeowners Association (HOA) fees. For instance, if your property in Kalamazoo generates the average local rent of $1,256 as of March 31, 2026, and your total PITI plus HOA is $1,000, your ratio is 1.25. A 1.25 ratio is considered the “gold standard” for 1st Class service because it provides a 25% safety margin above the property’s debt obligations.

While many lenders set a hard floor at 1.00, some “No Ratio” programs exist for investors with significant down payments and high credit scores. Short-term rentals, like those found near the lakes in St. Joseph, are often treated differently. Lenders may use a 12-month average of AirDNA data or actual historical records rather than a standard long-term lease agreement to determine the property’s income potential.

Strategies to Improve Your Ratio Before Applying

If your initial math shows a ratio below 1.0, don’t worry. You can still adjust your flight plan to meet dscr loan requirements. The most direct way to boost your ratio is to “trim the weight” by increasing your down payment. A larger down payment reduces the principal loan amount, which lowers your monthly interest and principal payments. This simple adjustment can often turn a struggling deal into a cash-flowing asset.

You can also shop for better insurance rates. A $50 monthly saving on your premium might seem small, but it directly lowers the denominator and can nudge a 0.98 ratio into qualifying territory. Finally, look for value-add opportunities. If a small renovation allows you to justify a higher market rent on the appraiser’s 1007 form, your ratio will climb accordingly. We’re here every step of the way to help you analyze these adjustments so your portfolio stays on a steady climb toward your goals.

DSCR vs. Conventional Financing: Which Aircraft Fits Your Portfolio?

Choosing your financing vehicle is a strategic decision that determines how fast your portfolio can climb. Conventional loans are like heavy cargo planes; they offer lower interest rates but require an exhausting amount of documentation. For the week ending April 30, 2026, conventional 30-year fixed rates averaged 6.30%. In contrast, DSCR loans currently range from 6.125% to 9.125%. While the “fuel cost” in interest is higher, the dscr loan requirements allow you to bypass the mountain of tax returns and paystubs that often ground conventional applications. This speed is what allows professional investors to move from offer to closing in record time.

Sometimes, your investment goals are more personal than a standard rental play. If you’re looking to house an elderly parent or a disabled adult child in a property valued near the Kalamazoo average of $236,274, you might consider a Family Opportunity Mortgage in Kalamazoo. This niche program provides a different flight path by allowing for owner-occupied rates on a second home, which can be a vital alternative when the property math doesn’t fit a traditional DSCR model.

The Trade-offs: Rates vs. Documentation

DSCR loans are the “express lane” of the mortgage world. Because qualification rests on the property’s cash flow, you won’t need to provide W2s or personal income verification. This streamlined process is a relief for self-employed investors who have significant write-offs on their tax returns. However, you must navigate specific trade-offs like prepayment penalties. These are common in the DSCR space and are designed to ensure the lender’s “flight” remains profitable for a set duration. In 2026, you’ll also decide between a stable 30-year fixed rate or an Adjustable-Rate Mortgage (ARM), depending on your projected hold time for the property.

Scaling Your Portfolio with Multi-Property Loans

Conventional financing typically caps your growth at 10 properties. Once you hit that ceiling, your expansion is grounded. DSCR loans offer unlimited scaling potential because they don’t rely on your personal debt-to-income ratio. You can even utilize “blanket” DSCR loans to group multiple properties in Portage or Battle Creek under a single mortgage. This simplifies your monthly management and allows you to use cash-out refinances to fund the “runway” for your next acquisition. If you’re ready to see which aircraft fits your current fleet, contact us for a custom flight plan today. We’re here to help you navigate the dscr loan requirements and ensure your portfolio stays airborne.

Navigating the Kalamazoo Investment Market: Securing Your 1st Class Loan

Investing in West Michigan requires more than just a spreadsheet; it requires local boots on the ground from Kalamazoo to St. Joseph. Jeremy Drobeck – Treadstone Mortgage serves as your Seasoned Co-Pilot, ensuring you don’t just meet the dscr loan requirements, but that you thrive within them. While “big box” lenders offer a cold, transactional experience, we provide the personal attention and respect your portfolio deserves. We’re here every step of the way to ensure your financial flight is smooth and your landing is precise.

Local Market Insights for Portage and Battle Creek Investors

The stability of the Kalamazoo rental market is anchored by the consistent student housing demand near Western Michigan University, providing a reliable runway for multi-unit investments. In Portage and Battle Creek, local appraisal knowledge is the difference between a stalled application and a successful takeoff. An appraiser who understands the West Michigan landscape will provide a more accurate 1007 Rent Schedule, which is vital for your math. We also help you navigate Michigan-specific property tax uncapping. This local tax rule can significantly increase your expenses after a title transfer, and failing to account for it can cause unexpected turbulence in your cash flow.

Your Mortgage Consultation: Starting the Flight Plan

Ready to clear your next deal for departure? Your initial mortgage consultation is the first step in building a reliable flight plan. To get started, bring a property address, an estimated monthly rent, and a snapshot of your credit score. We’ll review the latest dscr loan requirements to find the program that offers the best lift for your specific goals. Whether you’re targeting a turnkey single-family home or a value-add duplex, we’ll map out the path to success. Our “1st Class” promise means you’ll receive transparency, precision, and end-to-end support throughout the process.

Navigate your next investment with a 1st Class consultation and see how easy scaling your portfolio can be when you have the right co-pilot at your side. We’re ready to help you reach new altitudes in your real estate journey.

Clear Your Portfolio for Takeoff in 2026

Mastering the dscr loan requirements is the key to unlocking a scalable real estate business without the drag of personal income limits. You’ve seen how property cash flow and precise ratios provide the lift needed to bypass traditional documentation barriers. By focusing on the property math rather than your personal W2s, you ensure your portfolio remains in a steady climb. This strategy allows you to move past the 10-loan conventional limit and treat your investments like the high-performing assets they are.

With 20+ years of West Michigan mortgage expertise, Jeremy Drobeck – Treadstone Mortgage, a division of Neighborhood Loans (NMLS #222982), specializes in these Non-QM and Investor Cash Flow programs. We don’t just process paperwork; we act as your seasoned co-pilots to navigate the complexities of local appraisals and Michigan-specific tax codes. It’s time to trade the frustration of debt-to-income caps for the unlimited runway of DSCR financing.

Schedule Your DSCR Flight Plan Consultation with Jeremy Drobeck today. We’re here every step of the way to make your investment dreams airborne.

Frequently Asked Questions

What is the minimum DSCR ratio required for an investment loan in 2026?

The minimum ratio is typically 1.0, meaning the property’s rent equals its debt. However, most lenders prefer a 1.25 ratio to provide a safety margin and unlock the most competitive interest rates. In 2026, hitting this 1.25 benchmark is your best bet for a smooth landing with premium terms. We’ll help you calculate this “flight math” during your initial consultation to ensure your deal is cleared for takeoff.

Can I get a DSCR loan with a 620 credit score?

Yes, you can qualify with a 620 credit score, though it usually requires a larger down payment. To get the best lift and lowest rates, investors should aim for a score of 740 or higher. Meeting the dscr loan requirements with a lower score is possible, but it may change your loan-to-value (LTV) ratio. We’re here to help you evaluate your credit “flaps” and find the right program for your journey.

Do DSCR loans require personal income verification or tax returns?

No, DSCR loans do not require tax returns, W2s, or paystubs. Qualification is based entirely on the property’s ability to generate its own income. This “express lane” is perfect for self-employed investors who have significant tax write-offs that might ground a conventional application. It allows you to maintain a high altitude of growth without the documentation barriers of traditional banking. We focus on the property’s performance rather than your personal paycheck.

How much down payment is typically required for a DSCR mortgage?

A 20% to 25% down payment is standard for most dscr loan requirements in 2026. Some specialized programs might allow for 15% down if your credit score is above 740 and the property has exceptional cash flow. This equity acts as your safety net during market fluctuations. It ensures you have enough “fuel” in the property to withstand any temporary vacancies or maintenance needs while keeping your portfolio airborne.

Are DSCR interest rates higher than conventional mortgage rates?

Yes, DSCR interest rates are typically 0.75% to 2.0% higher than conventional rates. As of April 30, 2026, conventional rates averaged 6.30%, while DSCR rates often fall between 6.125% and 9.125%. Investors view this extra “fuel cost” as a fair trade for the ease of documentation and unlimited scaling. The higher rate is offset by the ability to close deals faster and grow your portfolio without personal income caps.

Can I use a DSCR loan for a short-term rental or Airbnb property in Michigan?

Yes, short-term rentals are fully eligible for DSCR financing in Michigan markets like Kalamazoo and St. Joseph. We use AirDNA data or historical rental records to verify the property’s income potential. This allows you to leverage the high-yield “lift” of vacation rentals to grow your wealth faster. It’s a popular strategy for investors looking to maximize their cash flow in the competitive West Michigan landscape while skipping traditional debt-to-income hurdles.

What happens if my property’s DSCR ratio is below 1.0?

If your ratio is below 1.0, you may still qualify through a “No Ratio” loan program. These programs typically require a higher down payment, often 30% or more, to offset the risk of the property not covering its own debt. It’s a great way to secure a property in a high-appreciation area where rents haven’t caught up yet. We can help you adjust your flight plan to ensure your application still reaches a successful landing.

Is there a limit to how many DSCR loans one investor can have?

There is no limit to the number of DSCR loans an investor can hold. Unlike conventional financing, which grounds you after 10 properties, DSCR programs allow for an unlimited runway. This is why professional investors use these loans to scale their portfolios into dozens or even hundreds of units. You can keep adding “aircraft” to your fleet as long as each property meets the cash flow standards and you have the required reserves.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”