What Is a Rehab Loan? Your 2026 Flight Plan for Kalamazoo Fixer-Uppers

Imagine you just found a charming brick ranch in Portage, but the kitchen is stuck in 1974 and the roof is failing. In a market where houses sell in just 15 days, you don’t have time to hesitate. You might be asking, what is a rehab loan, and how can it help you secure this property before another buyer swoops in? It’s a common struggle in Kalamazoo, where the median sale price hit $211,000 in March 2026. You find a house with potential, but the $30,000 repair bill feels like a weight holding you back from takeoff.

We agree that managing two separate loans for a fixer-upper is a recipe for high-altitude stress. This article will show you how to combine your purchase and renovation costs into one monthly payment to help you land your dream home in West Michigan. We are going to explore the specific 2026 flight plan for FHA 203(k) and conventional renovation tools, giving you the GPS needed to navigate today’s competitive seller’s market with confidence.

Key Takeaways

- Learn what is a rehab loan and how it provides the extra lift needed to bundle your home purchase and repair costs into a single, manageable monthly payment.

- Navigate the differences between FHA 203(k) and Conventional renovation paths to choose the right financing for your specific credit score and project goals.

- Unlock hidden inventory in competitive neighborhoods like Edison or Vine by transforming dated fixer-uppers into modern masterpieces.

- Master the renovation timeline, from securing your pre-approval GPS to coordinating with a contractor crew for a smooth landing.

- Gain the confidence of a 1st Class journey by partnering with a seasoned co-pilot who guides you through every step of the renovation process.

What Is a Rehab Loan? The ‘Extra Lift’ for Your Home Purchase

So, what is a rehab loan? Think of it as the extra lift your home buying journey needs when the perfect property is just a few repairs away from being flight ready. At its core, a rehab loan is a single mortgage that covers both the purchase price of the home and the cost of the improvements you want to make. It replaces the high stress scramble of finding separate financing for a fixer-upper with a streamlined, one-and-done solution. You don’t have to worry about maxing out credit cards or draining your savings just to make a house livable.

The primary advantage here is simplicity. You deal with one closing, secure one interest rate, and make one monthly payment. This creates a clear runway for buyers in a low inventory market like Kalamazoo, where the median sale price rose 17.2% year-over-year in March 2026. Instead of fighting over the few turnkey homes available, you can look at the dated properties in West Michigan and see potential. The renovation funds aren’t handed over in a lump sum; they are held in a secure escrow account and released to your contractor as specific phases of the work are completed. This ensures the project stays on course and the money is used exactly where it belongs.

How Rehab Loans Differ from Standard Mortgages

Standard mortgages are grounded by the home’s current condition. If the kitchen is gutted or the roof is leaking, a traditional lender might not even clear you for takeoff. Rehab loans are different because they use the as-completed value. This is the projected market value after all renovations are finished. By focusing on the future state of the property, you can borrow significantly more than the home’s current purchase price. This gives you the financial fuel needed for a total transformation without needing a massive pile of cash upfront.

The Core Benefits: Why Stop Renting and Start Renovating?

One of the biggest wins is the potential for instant equity. It’s common for the final value of a renovated home to exceed the combined cost of the purchase and the repairs, especially in growing areas like Portage. You also get total control over customization. Instead of paying a premium for someone else’s design choices, you pick the cabinets, flooring, and layout that fit your lifestyle. Finally, there’s the peace of mind that comes with safety. Financing major structural or mechanical repairs immediately ensures your home is efficient and sound from day one. This is often a much more stable path than waiting years to qualify for a Home equity loan to fix problems that have only grown more expensive over time.

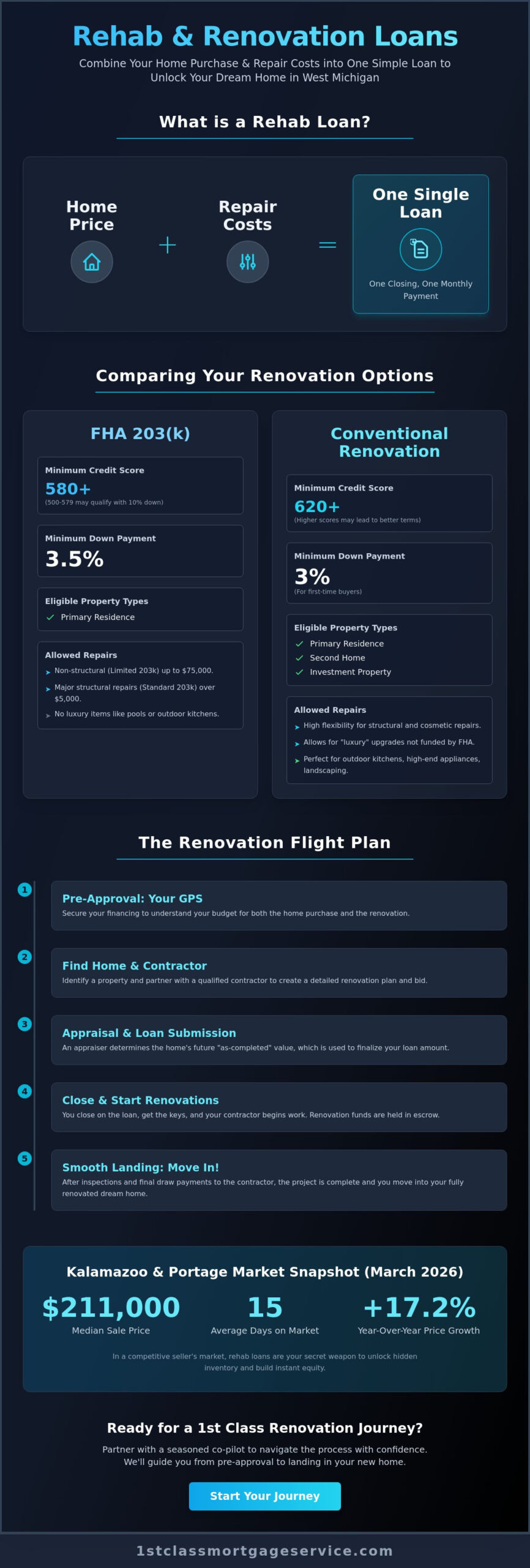

Comparing Your Renovation Options: FHA 203(k) vs. Conventional Loans

Choosing the right flight path is the most critical decision in your renovation journey. While you now know what is a rehab loan in a general sense, you must decide which specific program provides the best lift for your financial situation. The two primary runways for West Michigan buyers are government-backed FHA 203(k) loans and Conventional renovation products like Fannie Mae’s HomeStyle. Each has its own set of flight requirements regarding credit scores, property types, and the scope of work allowed.

The FHA 203(k): The Accessible Flight Plan

The FHA 203(k) is often the most accessible route for buyers who need a little extra help getting airborne. It requires a low down payment of just 3.5% for borrowers with a credit score of 580 or higher. If your credit is lower, between 500 and 579, you can still qualify with a 10% down payment. This flexibility makes it a premier choice for Home Remodel Loans with Bad Credit. The 203(k) Rehab Mortgage Insurance program offers two distinct paths. The “Limited” 203(k) is perfect for non-structural repairs like new flooring or kitchen upgrades up to $75,000. For major structural overhauls, the “Standard” 203(k) handles projects costing $5,000 or more and requires a HUD-approved consultant to oversee the work.

Conventional Renovation: The Flexible Alternative

If you have a credit score of 620 or higher, a Conventional renovation loan might offer a smoother ride. These loans are highly flexible because they aren’t restricted to primary residences. You can use them to renovate a second home or even an investment property. Unlike FHA options, Conventional loans allow for “luxury” upgrades that the government won’t typically fund. This includes items like permanent outdoor kitchens, landscaping, or high-end appliances. For first-time buyers, the down payment can be as low as 3%, and those with strong credit often enjoy lower monthly mortgage insurance costs compared to FHA counterparts.

Deciding between these options depends on your specific cargo and destination. FHA rates as of May 4, 2026, show a national average APR of 6.32%, though 203(k) rates are typically 0.5% to 1.0% higher due to the added complexity. Conventional rates for a 30-year fixed loan averaged 6.28% in early May 2026. If you want to see which program offers the most lift for your specific project, you can explore all your renovation home loans with our team. We’re here to help you weigh the pros and cons so you can make an informed decision for your Kalamazoo or Portage home.

The Renovation Flight Plan: Step-by-Step from Pre-Approval to Landing

Before you can take off, you need a reliable GPS. In the mortgage world, that starts with a pre-approval. This step ensures you know exactly how much house you can afford plus the cost of the renovations. Many buyers ask, what is a rehab loan process like compared to a standard purchase? It requires a few extra checklists, but with the right co-pilot, it’s a controlled ascent. Once you find the property, your contractor becomes an essential member of your flight crew. They provide the detailed bids that the bank uses to calculate your as-completed value. This appraisal validates the future worth of the home; it allows the lender to secure the necessary funds for your transformation before the first hammer swings.

Choosing Your Contractor in West Michigan

Your contractor is the lead engineer of your project. In Michigan, they must be licensed and insured to work on renovation loan projects. You can’t just hire a friend with a truck; the lender needs to see professional credentials to ensure the home’s structural integrity. To clear your pre-flight inspection in underwriting, your contractor must provide a detailed, line-item bid. This document breaks down every expense, from plumbing fixtures to drywall labor. If you’re looking for a team that understands these requirements, check out the Top Renovation Lenders in Kalamazoo & Portage: Your 2026 Flight Plan for Fixer-Uppers to find experts who specialize in these complex files.

Managing the Draw Schedule

One of the most misunderstood parts of what is a rehab loan involves how the money moves. The lender doesn’t hand you a suitcase of cash at closing. Instead, the funds are held in an escrow account and released in stages called draws. As your contractor completes specific milestones, like finishing the rough-in plumbing or installing the roof, they request a payment. For a Standard 203(k) loan, a HUD-approved consultant will visit the site to inspect the progress before any fuel is released. This protects you by ensuring the work meets safety standards before the contractor gets paid. The final landing happens after a successful final inspection. Once the city clears the permits and the appraiser confirms the work is done, your renovation account is closed and you are cleared for full occupancy.

Why Rehab Loans are the Secret Weapon for Kalamazoo & Portage Homebuyers

In the historic streets of the Edison and Vine neighborhoods, many beautiful homes are waiting for a second chance. While these properties often have the “good bones” needed for a long-term investment, their outdated electrical or plumbing systems can scare off traditional buyers. This is where understanding what is a rehab loan becomes your competitive advantage. In Portage, where homes move in just 15 days, the inventory shortage is real. You can bypass the bidding wars on turnkey properties by targeting 1970s ranches that need a cosmetic lift. These homes often sit longer because most buyers can’t see past the dated wallpaper or worn flooring.

In nearby Battle Creek, you might find yourself competing against cash investors who want to flip homes for a quick profit. By using a loan to fix house, you can offer a competitive price and still have the funds to customize the property to your own standards. Fixer-uppers in West Michigan often sit on the market longer than move-in-ready homes; the median days on market in Kalamazoo is 28 days compared to the lightning-fast 15 days in Portage. This gives you a longer runway to conduct inspections and finalize your renovation flight plan without the pressure of an immediate bidding war.

Identifying the Right Property in West Michigan

Finding a “diamond in the rough” requires looking past bad carpet or peeling paint. You want to find homes with solid foundations and functional layouts that simply need modern updates. However, be cautious of “red-tagged” properties. These are homes deemed uninhabitable by the city, and they often won’t qualify for standard rehab financing without significant hurdles. Working with a local Realtor who understands how to spot these issues early is vital. They act as your ground crew, helping you identify which houses are ready for a renovation takeoff and which ones should stay grounded. A smart Realtor knows that a house with a 30% discount due to a failed roof is actually a goldmine when you have the right financing.

Leveraging Local Expertise

National banks often struggle with the nuances of the Kalamazoo appraisal market. A local lender like Treadstone understands the value of a restored historic home in the Vine neighborhood better than a computer algorithm in another state. We take a neighborly approach, coordinating directly with your Michigan contractors to ensure everyone is on the same page. For a deep dive into the specifics of local financing, read our Renovation Home Loans: Comparing Your Best Options in Kalamazoo & Portage. If you are ready to start your journey, get pre-approved with our team today to discuss your specific project goals.

Navigating Your Renovation with a Seasoned Co-Pilot

A renovation project has many moving parts; it is not a flight you want to pilot alone. When people ask our team, what is a rehab loan, they aren’t just looking for a technical definition. They are looking for a partner who can handle the mechanical complexity of as-completed appraisals and the specific timing of escrow draws. Jeremy Drobeck and the Treadstone team act as your seasoned co-pilots, bringing professional authority and neighborly reassurance to every stage of the journey. We specialize in those “outside the box” scenarios that often ground applications at larger, national banks. Whether you are revitalizing a historic home or modernizing a dated ranch, we ensure your financial plan is structurally sound before you ever leave the runway.

Our approach shifts the emotional frequency of the mortgage process. We replace the high-stress barriers of home buying with a supportive, partnership-based relationship. We don’t view your loan as a cold transaction; we see it as a significant life milestone that requires careful handling and empathy. By choosing a local expert who understands the West Michigan landscape, you gain an ally who is deeply committed to the safety and success of your journey. We are here every step of the way to ensure your renovation isn’t a gamble, but a controlled and engineered process.

The 1st Class Mortgage Experience

We believe every homebuyer deserves personalized attention and respect. We treat your mortgage like a 1st Class flight rather than a standard banking transaction. Our crew provides constant transparency and communication to help you navigate the inevitable turbulence of contractor bids and unexpected repair requirements. Jeremy’s 20+ years of experience in Kalamazoo ensures a smooth landing for your home project. We provide the steady, reliable support that turns a complex fixer-upper purchase into a clear path toward homeownership. You can fly with confidence knowing that your co-pilot has handled thousands of similar flights across West Michigan.

Your Next Steps

Ready for takeoff? Your journey begins with a simple pre-flight checklist. You’ll need to gather your standard financial documents, such as tax returns and pay stubs, to establish your baseline lift. Once we have your GPS coordinates set, we can explore which specific renovation program fits your goals and budget. We invite you to explore all options during a no-obligation consultation at our offices in Portage or Kalamazoo. Don’t let a house that needs work stay out of reach when the right financing can get you airborne. Schedule your mortgage consultation with Jeremy Drobeck today and let’s start building the home you’ve always wanted.

Clear Your Path for a West Michigan Home Transformation

You now possess the complete flight plan to bypass the 15 day inventory shortage in Portage and the competitive bidding wars of Kalamazoo. Understanding what is a rehab loan gives you the tactical advantage to see potential where other buyers see only repair bills. By bundling your purchase and renovation costs into one monthly payment, you can secure a dated 1970s ranch or a historic Vine neighborhood gem with the efficiency of a single closing.

Jeremy Drobeck and the Treadstone team provide the specialized expertise in FHA 203(k) and Conventional Renovation loans required for a smooth landing. With more than 20 years of local West Michigan experience, we offer 1st Class service balanced with neighborly reassurance. We’re here every step of the way to ensure your specific home project stays on course from the initial bid to the final inspection.

Start Your Renovation Flight Plan with Jeremy Drobeck today to secure your future in West Michigan. Your dream home is officially cleared for takeoff.

Renovation Financing: Frequently Asked Questions

Can I use a rehab loan to buy an investment property in Battle Creek?

Yes, you can use a Conventional renovation loan for investment properties in Battle Creek, but FHA 203(k) loans are strictly for primary residences. Conventional products like Fannie Mae HomeStyle allow for non-owner occupied projects with a 15% down payment. This flexibility is perfect for investors looking to revitalize the Battle Creek housing stock while building long term equity.

What is the minimum credit score for an FHA 203(k) loan in 2026?

The minimum credit score for an FHA 203(k) loan in 2026 is 580 to qualify for the 3.5% down payment option. Borrowers with scores between 500 and 579 can still gain lift, but they must provide a 10% down payment. We always recommend a consultation to see which flight path fits your specific credit profile and financial goals.

Do I have to live in the house while it is being renovated?

You don’t have to live in the home during a major renovation if it is deemed uninhabitable. In fact, many rehab loans allow you to finance up to six months of mortgage payments into the loan amount. This ensures you aren’t paying both a mortgage and rent while your Kalamazoo home is under construction.

Can I do the work myself to save money on a rehab loan?

Most lenders require licensed and insured contractors to perform the work rather than allowing sweat equity. This policy protects the home’s as-completed value and ensures all Michigan building codes are met. When you’re asking what is a rehab loan benefit, remember that professional labor ensures the structural integrity of your 1st Class investment.

How long does the rehab loan process take compared to a standard mortgage?

A rehab loan typically takes 45 to 60 days to close, which is longer than the 30 day average for standard mortgages. This extra time is necessary to coordinate contractor bids and complete the specialized appraisal. We work hard to keep your flight on schedule, but the added complexity requires a few extra checklists before takeoff.

What happens if the renovation costs go over the initial estimate?

Most renovation mortgages include a mandatory contingency reserve of 10% to 20% of the repair costs to handle unexpected issues. If your contractor finds hidden water damage or electrical problems, these funds act as your safety net. This reserve ensures your project doesn’t stall mid-flight because of a sudden change in the weather.

Are there limits on how much I can borrow for repairs in Kalamazoo County?

Yes, the total amount you borrow is subject to 2026 loan limits. For a single family home in Kalamazoo County, the FHA loan limit is $541,287. Conventional limits are higher, reaching $806,500 in most areas. Your total cargo, including the purchase price and renovation costs, must stay within these established boundaries to clear underwriting.

Can I refinance my current home into a rehab loan to do a major remodel?

You can absolutely refinance your current home into a renovation mortgage to fund a major remodel. This refinance-rehab path uses the future value of your home after the upgrades are finished to determine your loan amount. It is an excellent way to add a second story or a modern kitchen without needing a separate high interest loan.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”