Kalamazoo Amortization Calculator: Planning Your 2026 Mortgage Flight

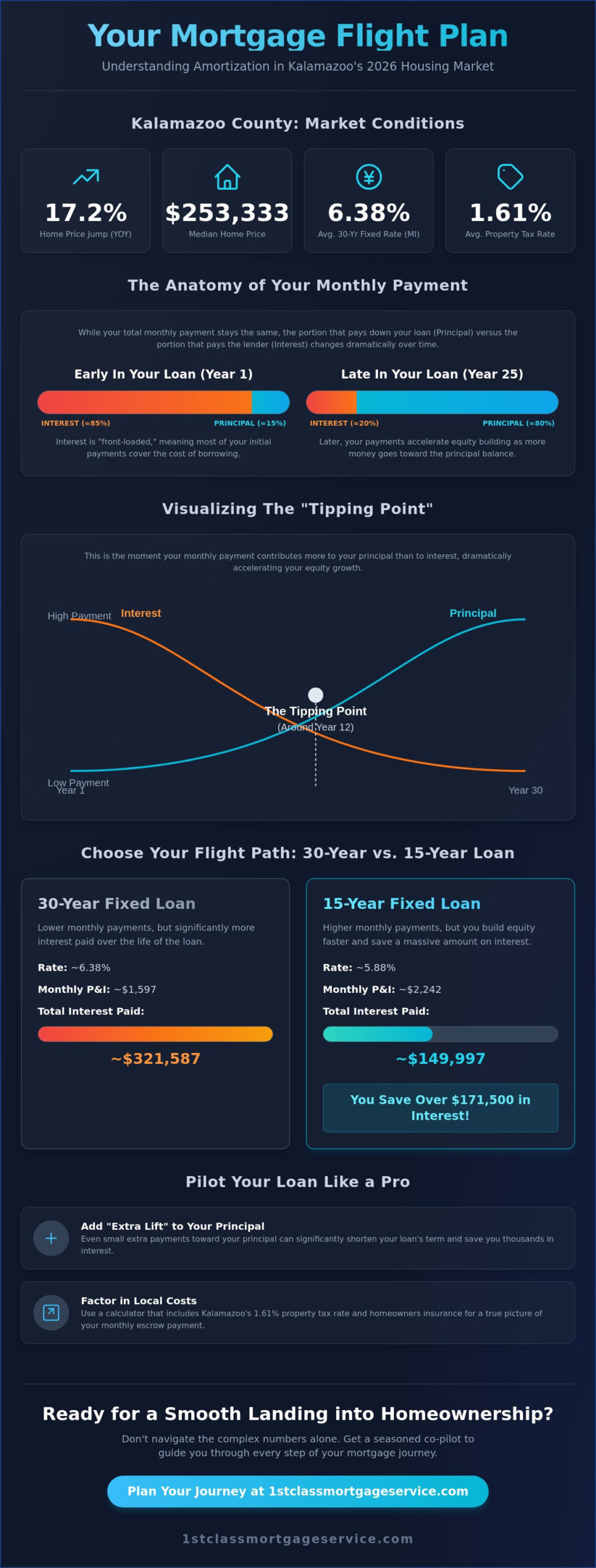

In March 2026, home prices in Kalamazoo jumped 17.2% compared to the previous year, leaving many local buyers feeling like they are flying into a headwind. You might have a handle on the $253,333 median price tag for a Kalamazoo County home, but the real mystery often lies in the cockpit of your long-term loan. It’s common to feel a bit of turbulence when you realize how much interest is front-loaded into those early years of a 30-year fixed mortgage, currently averaging around 6.38% in Michigan. Using a professional amortization calculator is the best way to clear the clouds and see exactly where your money is going every month.

We understand that the math behind property taxes and interest can feel like navigating through thick fog. That is why we are here to help you master your monthly payments and gain total control over your financial flight path. You’ll learn how to decode your repayment schedule, account for the 1.61% average property tax rate in our area, and see exactly how to build equity faster. This guide provides the GPS you need to gain total confidence in your budget for a Battle Creek or Kalamazoo home, ensuring your journey to homeownership stays on a steady, successful course.

Key Takeaways

- Understand how your monthly payment is split between principal and interest over the entire 30-year flight path.

- Use an amortization calculator to visualize how interest acts as “drag” in the early years of your loan before you reach cruising altitude with equity.

- Factor in local Kalamazoo and Portage property taxes to get a complete picture of your monthly escrow, not just principal and interest.

- Learn how small adjustments, like adding “extra lift” to your monthly principal, can significantly shorten your loan’s flight time.

- Discover why a seasoned co-pilot is essential for navigating the complex numbers of the 2026 Michigan housing market.

What is an Amortization Calculator and Why Do Kalamazoo Buyers Need One?

Think of your mortgage as a long-distance flight plan. Amortization is the process of spreading your loan payments over a fixed runway, typically a 15 or 30-year term. While your total monthly payment usually stays level, the internal mechanics of that payment are constantly shifting. In the early stages of your flight, a larger portion of your check goes toward interest. As you progress down the runway, the ratio flips, and more of your money begins to pay down the actual balance of the loan. An amortization calculator is the essential tool that maps this transition, showing you exactly when you will reach cruising altitude with your equity.

In 2026, buyers in Portage and Battle Creek are navigating a market where the median home price in Kalamazoo County has reached $253,333. When you are committing to a 30-year journey, you need to see the total interest cost upfront to avoid financial turbulence. By using an amortization calculator, you can visualize your “equity altitude” before you ever sign the closing papers. Seeing the math early on helps you understand the true cost of the journey, ensuring your budget is built on solid ground rather than guesswork. We want you to feel in total control of your flight path from takeoff to touchdown.

The Anatomy of an Amortized Loan

Every mortgage payment consists of specific components that keep your financial flight airborne. Understanding these parts helps you manage your expectations over the life of the loan. Here is the breakdown of what you’re paying for:

- Principal: This is your cargo. It is the actual amount of money you borrowed to purchase your Kalamazoo home.

- Interest: Think of this as the fuel cost. It is the fee paid to the lender for the privilege of using their capital for the journey.

- Term: This is your flight length. Most Michigan homeowners opt for a 15 or 30-year runway, which dictates how quickly the principal is repaid.

Amortization vs. Revolving Debt

A mortgage is fundamentally different from a credit card “holding pattern.” With revolving debt like a credit card, you can stay in the air indefinitely if you only pay the minimum balance, often without ever reaching a destination. A mortgage, however, is designed to land. Amortization is the scheduled reduction of debt through regular installments of principal and interest. This fixed end-date provides a clear destination for homeowners in St. Joseph or Kalamazoo. You aren’t just paying a bill; you’re following a pre-engineered path that leads to 100% ownership of your property.

The Mechanics of Your Mortgage Flight: How Amortization Works

When you first take off on your homeownership journey, it can feel like you are at full throttle but barely gaining altitude. This is the “front-loaded” interest phenomenon. In the early years of your loan, the bank collects most of its interest upfront. Think of interest as the aerodynamic drag you fight during takeoff. It takes a significant amount of energy to get a heavy plane off the ground; similarly, your early payments are primarily overcoming the cost of the debt itself. An amortization calculator reveals that while your monthly check remains the same, the internal balance is slowly shifting in your favor.

As you continue your flight, you eventually hit the “Tipping Point.” This is the specific month in your schedule where your payment finally applies more money toward your principal than toward interest. From this moment on, your equity builds at an accelerated rate. Every payment made on your Kalamazoo property is a step closer to 100% ownership. You can use an Amortizing Loan Calculator to pinpoint exactly when this transition occurs for your specific loan amount and rate. Seeing this shift on paper can replace the anxiety of a 30-year commitment with a sense of clear, expert guidance.

The 30-Year vs. 15-Year Flight Path

Choosing your runway length is one of the most critical decisions you will make. As of May 2, 2026, the average 30-year fixed mortgage rate in Michigan sits at 6.38%. If you opt for a shorter 15-year flight path, that rate drops to approximately 5.88%. While the 15-year option requires a higher monthly payment, the total interest “fuel” you save over the life of the loan is massive. You can check the current mortgage rates in Kalamazoo to see how even a small shift in percentage points alters the slope of your equity curve. If you are unsure which path fits your budget, consulting with a local mortgage expert can help you weigh the trade-offs between lower monthly costs and long-term savings.

Visualizing the Schedule

An amortization table might look like a complex flight manifest at first glance, but it is simpler than it appears. Focus on three main columns. The “Principal Paid” column shows your progress in actually buying back your home from the bank. The “Interest Paid” column tracks the cost of the “fuel” for that period. Most importantly, the “Remaining Balance” column serves as your true equity marker. You will notice that the principal portion starts small but gains momentum as the years pass. Watching that balance drop month by month provides the reassurance that your financial flight is on a steady, controlled descent toward a successful payoff.

Beyond the Calculator: Local Michigan Factors That Affect Your Monthly Payment

While an amortization calculator is a fantastic tool for mapping your principal and interest, it often leaves out the “cargo” that makes up your full escrow payment. For a buyer in Kalamazoo or Portage, your P&I is just the baseline. To avoid a rough landing when your first bill arrives, you must account for property taxes and homeowners insurance. These variables vary by zip code and can change your monthly “all-in” cost by hundreds of dollars. If you’ve ever wondered what does escrow mean and how it manages these local tax cycles and insurance costs on your behalf, understanding this secure holding system is essential before your first payment arrives. Before you commit to a purchase, it’s vital to understand how much are closing costs in Kalamazoo to ensure your total cash-to-close aligns with your savings.

West Michigan’s unique climate also adds another layer to your insurance premiums. Lake effect snow and heavy spring storms mean your roofing and structural coverage are non-negotiable. As of March 13, 2026, the average cost for homeowners insurance in Kalamazoo is approximately $1,443 per year. We view these costs as essential safety equipment for your flight. Skipping over these details in your initial math is like taking off without checking the weather report. We’re here every step of the way to ensure your budget accounts for every local nuance.

Kalamazoo Property Tax Impact

Michigan’s tax system operates on a unique flight schedule with summer and winter bills. In Kalamazoo County, the average property tax rate is 1.61% of the property’s assessed fair market value. For a home at the median value of $270,403, this is a significant portion of your monthly outflow. If you are buying a home as your primary residence, you should verify if it qualifies for the Homeowners Principal Residence Exemption (PRE). This exemption can provide significant “lift” by lowering your local school operating taxes. Without this in your math, your monthly GPS might lead you toward a budget that is higher than necessary.

Private Mortgage Insurance (PMI)

If your down payment is less than 20%, you will likely need to account for Private Mortgage Insurance (PMI). This adds “weight” to your monthly payment until you reach that 20% equity milestone. You can use your amortization calculator to track exactly when your principal balance will drop low enough to request the removal of PMI. If you are a first-time buyer looking to reach that equity goal faster, exploring MSHDA down payment assistance can provide the extra lift needed at takeoff. These programs are designed to help local families get airborne with less stress and more financial stability.

Shortening Your Runway: Using an Amortization Calculator to Pay Off Your Loan Faster

Just because your flight plan says 30 years doesn’t mean you have to stay in the air that long. You have the power to apply “extra lift” to your principal at any time, which effectively shortens your runway and saves thousands in interest. By plugging different scenarios into an amortization calculator, you can see how adding just $100 to your monthly principal payment can shave years off your total loan term. It’s a simple adjustment that significantly reduces the “drag” of long-term interest costs without requiring a massive overhaul of your lifestyle.

If you receive a large windfall, such as a 2026 tax refund or an inheritance, you might consider “recasting” your loan. This isn’t a refinance; it’s a way to keep your current interest rate while lowering your monthly payment based on a new, smaller balance. While pre-payment penalties are rare in modern conventional Michigan mortgages, it is always wise to double-check your specific note before making large lump-sum payments. We are here every step of the way to help you review these details so you can make the most efficient moves for your family’s financial future.

The Bi-Weekly Payment Strategy

One of the most popular ways to trim the flaps on your mortgage is the bi-weekly payment strategy. Instead of making one full payment every month, you make a half-payment every two weeks. Because there are 52 weeks in a year, you end up making 26 half-payments, which equals 13 full payments annually. That extra payment is applied directly to your principal, potentially reducing a 30-year loan by five to seven years. It is a disciplined approach that turns your standard 2026 budget into a high-performance engine for building equity.

Lump Sum vs. Recurring Principal Additions

When you look at your amortization calculator, you will notice that paying extra early in the flight has a much larger impact than paying extra late. This is because every dollar you pay down today stops the clock on all future interest that dollar would have accrued over the remaining decades. Whether you choose a recurring monthly addition or a single annual lump sum, the goal remains the same: reduce the principal balance as quickly as possible. Verify with your lender exactly how your extra payments are applied to ensure they hit the principal balance rather than just prepaying future interest. If you want a customized plan to pay off your home faster, contact Jeremy Drobeck today for a mortgage consultation.

Your Kalamazoo Mortgage Co-Pilot: Moving from Math to Homeownership

An amortization calculator is a powerful instrument on your flight deck, but data alone doesn’t fly the plane. While the numbers give you a clear view of your 30-year trajectory, they can’t account for the unique crosswinds of your personal financial situation. Jeremy Drobeck serves as your seasoned co-pilot, taking those raw calculations and turning them into a viable, stress-free strategy for homeownership. We believe that every borrower deserves personal attention and respect, regardless of whether you are buying your first condo in Portage or a family home in Battle Creek. Our mission is to lower the high-stress barriers of the 2026 market and replace them with a sense of calm, expert guidance.

We’re here every step of the way to ensure your financial flight remains on course. It’s easy to get lost in the “what-ifs” of interest rates and principal balances, but having a steady, reliable ally makes all the difference. We don’t just view your mortgage as a transactional banking experience; it’s a significant life milestone that requires careful handling and empathy. By moving beyond the digital screen, you gain access to a partnership-based relationship that prioritizes your long-term success over a simple loan approval.

Customizing Your Loan Flight Plan

Standard “out of the box” tools often fail when your situation gets complex. If you are exploring renovation financing to breathe new life into a historic property or looking at a DSCR loan for an investment, a basic amortization calculator won’t show the full picture. These scenarios require a mortgage broker near me who understands the specific mechanics of the Kalamazoo and Portage markets. During your first consultation, we provide a personalized amortization schedule that reflects your actual credit profile and income. This level of preparation and precision ensures that your flight plan is engineered for a smooth journey rather than a gamble.

Take the Next Step Toward Your New Home

It is time to move beyond the math and start your Purchase Mortgage journey in Kalamazoo. We invite you to reach out for a “mortgage GPS” session where we can map out your entire flight path together. Our 1st Class service promise means you’ll receive meticulous care and transparent “straight talk” from pre-approval to closing. We want you to feel in total control of the process, with a clear destination in sight. We’re here every step of the way, from the initial takeoff to the moment you land at your new front door. Reach out today and let’s get your homeownership dreams airborne.

Prepare for a Smooth Landing in Your New Home

Mastering your mortgage math is the first step toward a successful landing. You now understand how the tipping point shifts your payments toward equity and why local factors, such as the average 1.61% property tax rate in Kalamazoo County, are vital to your financial GPS. An amortization calculator is your best tool for visualizing this 30-year journey, but the data is most effective when paired with seasoned local expertise. We want you to feel total confidence as you transition from calculating numbers to holding your new set of keys.

Jeremy Drobeck has provided expert guidance to Michigan families since 2002, specializing in everything from MSHDA programs to complex renovation loans. You don’t have to navigate the 2026 housing market alone. By choosing a partner who offers personalized “1st Class” service, you ensure every detail of your flight is handled with precision. Ready to chart your course? Contact Jeremy Drobeck for your personalized Kalamazoo mortgage flight plan today! We’re here every step of the way to make sure your journey to homeownership is a success.

Frequently Asked Questions

How does an amortization calculator work for a 30-year fixed mortgage?

An amortization calculator uses a fixed mathematical formula to divide your monthly payment into principal and interest portions over 360 months. During the early years of your loan, the interest portion is much higher because it’s calculated based on your large remaining balance. As you pay down the principal, the interest charge decreases, allowing more of your payment to build equity in your home.

Will making one extra mortgage payment a year really help?

Yes, making a single extra payment each year can shorten a 30-year mortgage by roughly five to seven years. This strategy works because the entire extra payment goes directly toward the principal balance. By reducing the principal faster, you prevent interest from accruing on that amount for the rest of your flight, saving you thousands in long-term “fuel” costs.

Does the amortization calculator include Kalamazoo property taxes?

Most standard calculators only show principal and interest, so you must manually add local Kalamazoo costs to see your full payment. In Kalamazoo County, the average property tax rate is 1.61% of the property’s assessed fair market value. You should also factor in the average annual homeowners insurance cost of $1,443 to ensure your budget can handle the full monthly escrow amount.

What is the difference between principal and interest in my monthly payment?

Principal is the “cargo” or the actual money you borrowed to buy your house, while interest is the “fuel” cost paid to the lender. Every month, your payment covers the interest due for that period first. Any remaining funds are applied to the principal. This is why your equity builds slowly at first; the interest “drag” is highest when your balance is at its peak.

Can I use an amortization calculator for an FHA loan in Michigan?

You can use an amortization calculator for an FHA loan, but you must remember to include the Mortgage Insurance Premium (MIP). Unlike conventional loans where PMI eventually drops off, FHA MIP typically stays for the entire life of the loan. This added monthly “weight” is a crucial factor to include when you are mapping out your 2026 flight plan.

What happens to my amortization schedule if I refinance my mortgage?

Refinancing resets your amortization schedule to a new “day one” on a brand-new runway. Even if you secure a lower rate than the current 6.38% Michigan average, a new 30-year term means your payments will be interest-heavy again. We can help you analyze if the monthly savings provide enough lift to justify starting your repayment schedule over from the beginning.

How do I calculate how much interest I will pay over the life of my loan?

To find this, multiply your monthly principal and interest payment by the total number of months in your term, then subtract your original loan amount. An amortization calculator usually displays this “Total Interest Paid” figure as a primary data point. On a $253,333 median-priced home, the total interest over 30 years can be quite surprising if you don’t plan for extra payments.

Why is so much of my early mortgage payment going toward interest?

Interest is calculated based on your current outstanding balance, which is at its highest point when your flight first begins. Since the bank charges interest on what you still owe, the early months require more money to cover the cost of the debt. As your principal balance drops, the interest portion of your payment shrinks, and your progress toward 100% ownership accelerates. When you’re ready to take the next step, working with a local mortgage broker near me in Kalamazoo can help you find the right loan structure to minimize that early interest burden and accelerate your path to equity.

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”