The 50-Year Mortgage: A Tempting Trap That Could Ruin Your Financial Future

Are you dreaming of homeownership but feeling the pinch of rising interest rates and housing costs? You might come across a seemingly attractive solution: the 50-year mortgage. On the surface, it promises lower monthly payments, making that dream home feel within reach. But don’t be fooled. What looks like a lifeline can quickly become a financial anchor, dragging you down for decades.

Are you dreaming of homeownership but feeling the pinch of rising interest rates and housing costs? You might come across a seemingly attractive solution: the 50-year mortgage. On the surface, it promises lower monthly payments, making that dream home feel within reach. But don’t be fooled. What looks like a lifeline can quickly become a financial anchor, dragging you down for decades.

Let’s be clear: The 50-year mortgage is not just a long loan; it’s a path to financial ruin for most people.

The Illusion of Affordability: How a Small Monthly Saving Leads to a HUGE Loss

The allure is simple: a lower monthly payment. Who wouldn’t want to save some money each month? But this small saving hides a truly staggering cost over the lifetime of the loan. It’s the classic “penny wise, pound foolish” scenario on a monumental scale.

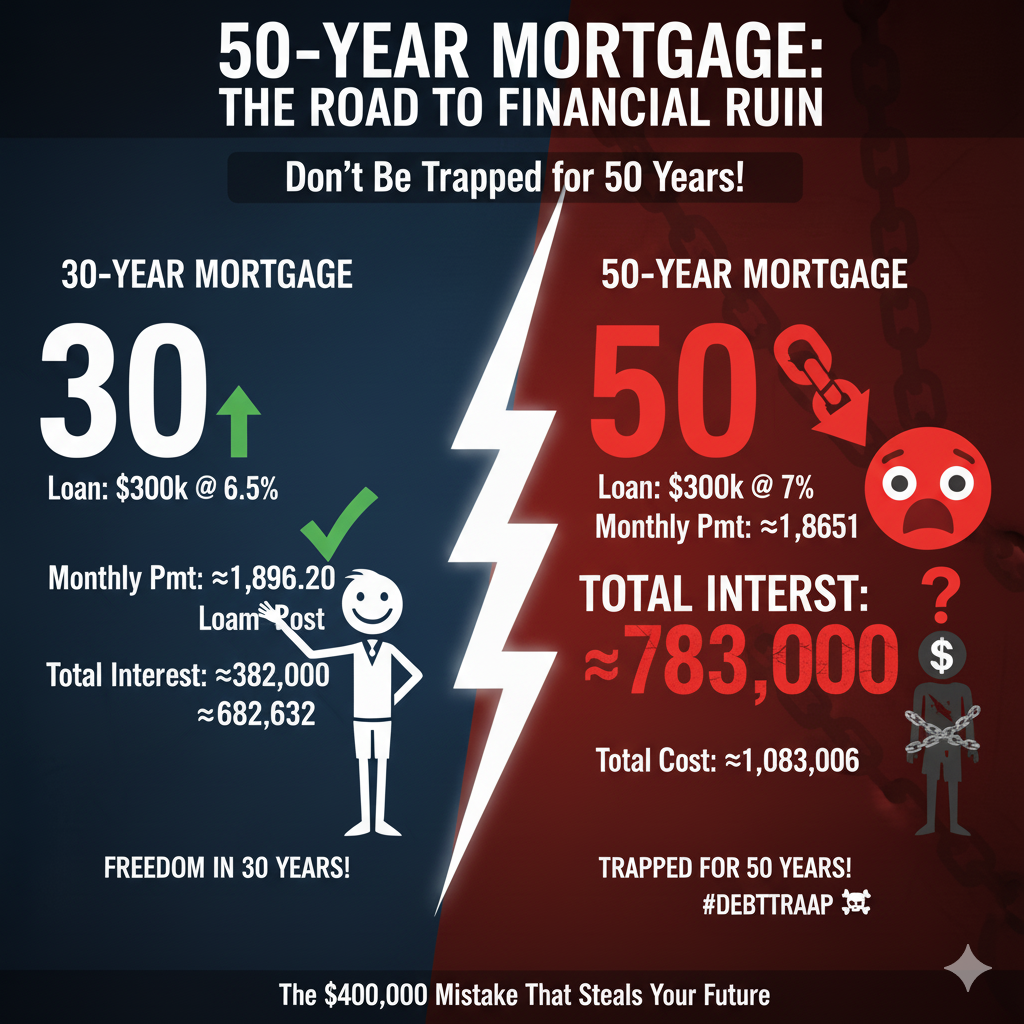

Let’s break down the numbers with a realistic example: a $300,000 loan.

| Loan Term | Interest Rate (APR) | Monthly Payment (Principal & Interest) | Total Interest Paid | Total Cost (Principal + Interest) |

| 30 Years | 6.5% | $1,896.20 | $382,632 | $682,632 |

| 50 Years | 7.0% | $1,805.51 | $783,306 | $1,083,306 |

Take a hard look at those figures. For a mere $90.69 per month in “savings,” you are committing to paying an additional $400,674 in interest!

This isn’t just a number; it’s nearly half a million dollars that evaporates into the pockets of the lender, instead of building your wealth. It’s the difference between paying $682,632 for your $300,000 home and paying over $1 MILLION.

Why the 50-Year Mortgage is a Wealth Killer

-

Massive Interest Accumulation: This is the biggest offender. Stretching a loan over 50 years means you’re paying interest for an additional two decades. The compounding effect is brutal, leading to hundreds of thousands of dollars in wasted money.

-

Delayed Financial Freedom: Imagine being in your 70s or 80s and still making mortgage payments. A 50-year loan can push your mortgage obligation well into your retirement years, potentially draining your retirement savings and limiting your quality of life when you should be enjoying financial freedom.

-

Limited Equity Growth: In the early years of any long-term mortgage, a significant portion of your payment goes towards interest, not principal. With a 50-year loan, this effect is amplified, meaning you build equity at an even slower rate. This makes it harder to refinance or sell if you need to, and you’ll have less capital to leverage for future investments.

-

Higher Overall Interest Rates: Lenders often charge a slightly higher interest rate for longer loan terms because they’re taking on more risk over a longer period. As seen in our example (7.0% vs. 6.5%), even a small increase in rate magnifies the already devastating interest accumulation.

The Bottom Line: Choose Financial Freedom, Not Lifelong Debt

While the appeal of a lower monthly payment is strong, especially in a challenging market, the 50-year mortgage is almost always a raw deal for the homeowner. It steals your future wealth, prolongs your debt, and severely limits your financial flexibility.

Instead of stretching out your debt, explore other options:

-

Save for a larger down payment to reduce your loan amount.

-

Look for a more affordable home that fits a 15 or 30-year mortgage comfortably. In our above example simply spending $15,000 less on a home would reduce the payment by that $90 per month.

-

Improve your credit score to qualify for better interest rates.

Don’t let a seemingly small monthly saving cost you hundreds of thousands of dollars and decades of financial freedom. Educate yourself, do the math, and choose a mortgage that supports your long-term financial health, not one that traps you. Most importantly call me for preapproval and honest advice!

Latest Blog Post

HOW TO PROTECT YOUR MORTGAGE RATE WHEN CLOSING GETS DELAYED

![]() Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Are you under contract on a home with an expiring rate lock? Need a rate lock extension?

Yesterday, a buyer called me in a total panic. They locked in their mortgage interest rate 30 days ago while shopping for a home near the Westwood neighborhood. Everything moved along fine until the seller asked to push closing back by ten days to finish clearing out their garage.

The buyer asked me, “Jeremy, if our rate lock expires before we close, will our interest rate jump up? Will our monthly payment go through the roof?”

I told them straight up: “Take a deep breath! An expiring rate lock will not ruin your deal, and you will not lose your low rate!”