Conventional vs USDA Loan Michigan: Your 2026 Mortgage Flight Plan

What if your home’s rising value wasn’t just a figure on a statement, but the high-performance engine that finally shuts down your high-interest credit card debt? With median home prices in Portage reaching $320,000 in early 2026, you’re likely sitting on significant equity, yet your monthly budget might still feel like it’s caught in heavy turbulence. We understand the stress of watching interest rates climb while you weigh the risks of securing debt against your family’s home. It’s a high-stakes decision that requires more than just a calculator; it requires a seasoned navigator who values your financial safety.

This guide provides a professional flight plan for using home equity to consolidate debt in Portage MI. You’ll learn how to leverage the 5.2% increase in local home values to streamline your cash flow and secure a single, manageable monthly payment. We will preview the current Michigan landscape for refinance mortgages and home equity tools, helping you improve your credit score through lower utilization. By the end of this journey, you’ll have the expert guidance needed to transform your home’s value into financial lift, ensuring your household’s economy stays on a steady and predictable course for years to come.

Key Takeaways

- Learn how to re-navigate your high-interest liabilities by transforming your home’s equity into a strategic engine for long-term financial stability.

- Discover the specific advantages of using home equity to consolidate debt in Portage MI, comparing the sustained lift of a refinance mortgage against secondary credit lines.

- Master the math behind your monthly cash flow to identify the exact break-even point when swapping 24% interest rates for more efficient mortgage terms.

- Understand how local appraisal trends in Kalamazoo County impact your borrowing power and provide a sturdy foundation for your financial flight plan.

- Follow a clear, step-by-step checklist to gather your data and prepare your credit for a successful takeoff toward a single, manageable monthly payment.

Navigating High-Interest Debt: Is Your Portage Home Equity the Lifeline You Need?

Think of your current financial situation as a flight path. When you are carrying high-interest credit card balances, it is like attempting to gain altitude with the landing gear stuck down. You are burning excessive fuel just to stay level without making any real progress toward your destination. Debt consolidation isn’t simply a way to move numbers around on a spreadsheet; it is a strategic re-navigation of your liabilities. By using the value already built into your property, you can swap out the heavy drag of high-interest debt for the steady lift of a mortgage-backed loan.

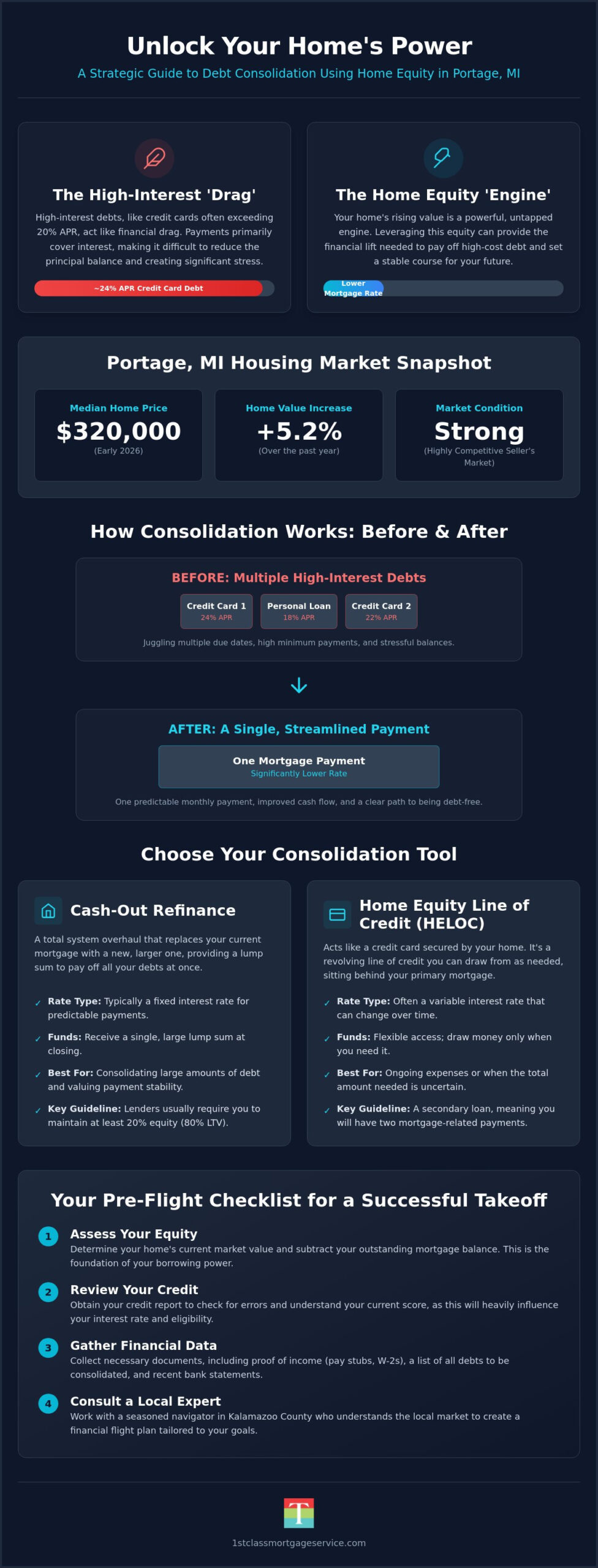

In the Portage market, many homeowners are sitting on a hidden engine of wealth they haven’t yet tapped. With the median sale price for homes in Portage reaching $320,000 as of May 2026, the equity available to local families has grown significantly. If you have maintained at least 20% equity in your home and are struggling with balances on cards or personal loans, using home equity to consolidate debt in Portage MI could be the maneuver that stabilizes your entire financial future. It allows you to leverage your home’s stability to pay off creditors and move forward with one manageable monthly obligation.

The Burden of High-Interest ‘Drag’

Credit card interest rates frequently exceed 20% APR, which creates a mathematical stall. When the majority of your payment only covers the interest, your principal balance barely moves. This creates immense psychological stress as you juggle multiple due dates and rising minimums. As we move through July 2026, the stability in the Michigan housing market offers a critical window. Evaluating your equity now, before any potential shifts in the broader economy, ensures you are using your strongest asset while its value is at a peak. Consolidating into a single payment doesn’t just save money; it clears the mental runway for other life goals.

Why Portage Homeowners are Well-Positioned

The West Michigan real estate market remains remarkably resilient. Home values in Portage increased by 5.2% over the past year, providing a sturdy collateral base that most lenders view favorably. Because Portage is considered a highly competitive seller’s market, appraisals are reflecting strong current values, often giving homeowners more borrowing power than they realize. Jeremy Drobeck – Treadstone Mortgage serves as your local navigator in Kalamazoo County, helping you determine if a refinance mortgage or other equity tool is the right fit for your specific journey. You don’t have to guess at the mechanics of your home’s value when you have a neighborly expert ready to check your flight data.

The Mechanics of Consolidation: Cash-Out Refinancing vs. HELOCs

Choosing between a cash-out refinance and a Home Equity Line of Credit (HELOC) is like selecting the right aircraft for your specific mission. Both vehicles allow for using home equity to consolidate debt in Portage MI, but they operate with very different flight mechanics. To understand What Is Debt Consolidation? in a local context, you must first look at your Loan-to-Value (LTV) ratio. Most Michigan lenders require you to maintain a 15% to 20% equity cushion after the transaction. For a cash-out refinance, staying at or below an 80% LTV is the industry standard to ensure your financial flight path remains stable and secure.

The primary difference lies in how you receive and repay the funds. A refinance replaces your entire existing mortgage with a new, larger loan, giving you a lump sum to pay off high-interest creditors. Conversely, a HELOC acts as a secondary booster, sitting behind your primary mortgage as a revolving line of credit. While a refinance offers the peace of mind that comes with a fixed interest rate, a HELOC provides flexibility, allowing you to draw only what you need. Understanding these components is essential before you commit to a long-term course correction.

Cash-Out Refinance: A Total System Overhaul

A Purchase Mortgage baseline is completely reset during a cash-out refinance. As of July 2026, the 30-year conventional refinance rate in Michigan sits at approximately 5.990%. This is significantly lower than the 20% or higher APR found on most credit cards. By touching your primary mortgage, you lock in a predictable monthly payment for the next 15 to 30 years. The downside is that you are resetting the clock on your home loan, which is why calculating the long-term interest cost is a vital part of your pre-flight prep. Reviewing current mortgage rates will help you decide if a total overhaul offers the most lift for your household budget.

HELOC: The Tactical Maneuver

If you have a small amount of high-interest debt, a HELOC might be the more tactical choice. It allows you to target specific balances without disturbing the low interest rate on your primary mortgage. In July 2026, national average HELOC rates are hovering around 7.04%. These tools feature a draw period, often ten years, where you only pay interest on what you use. Once that phase ends, you enter the repayment period. It is a flexible option, but because the rates are typically variable, they can fluctuate with the market. This tool is often safer for homeowners who have a clear, short-term plan to ground their debt quickly without a full system restructure.

Calculating Your Flight Path: Comparing Interest Rates and Monthly Cash Flow

Before you commit to a major navigational change, you need to see the actual flight data. Imagine you are carrying a $30,000 credit card balance at a 24% APR. That single debt creates a monthly interest charge of roughly $600 before you even begin to reduce the principal. By rolling that balance into a refinance mortgage at 6% or 7%, your monthly interest cost drops to approximately $150. This isn’t just a minor adjustment; it is a fundamental shift in your financial aerodynamics. Using home equity to consolidate debt in Portage MI allows you to exploit the massive gap between unsecured and secured interest rates, giving your monthly budget much-needed breathing room.

This maneuver also repairs your structural financial integrity by improving your Debt-to-Income (DTI) ratio. Lenders look at your monthly minimum obligations compared to your gross income to determine your stability. When you collapse five or six high-interest payments into one lower mortgage payment, your DTI improves instantly. The Federal Trade Commission guide on home equity highlights how these loans use your residence as collateral to secure more favorable terms. Additionally, your credit score often sees a significant boost because paying off revolving credit card balances lowers your utilization rate, which is a vital factor in credit scoring models.

Visualizing the Savings

A typical Portage homeowner can often save $500 or more every month through this transition. While you should always consider the long-term interest costs of extending a loan, the immediate impact on cash flow provides the stability needed to build an emergency fund or invest for the future. Interest Rate Arbitrage is the process of replacing high-cost debt with lower-cost capital to capture the spread as immediate monthly savings.

Factoring in Closing Costs

You must factor in the fuel required for this journey. Refinance closing costs in Michigan typically range from 2% to 5% of the loan amount as of July 2026. In Kalamazoo County, this includes a recording fee of $30 and an appraisal fee that generally falls between $400 and $700. Many homeowners choose to roll these costs into the new loan balance to avoid out-of-pocket expenses at the closing table. While some lenders advertise a no-cost refinance, remember that those expenses are usually accounted for through a slightly higher interest rate. Calculating your break-even point, the moment where your monthly savings exceed the cost of the loan, is the final check before you clear for takeoff.

The Local Portage Perspective: Home Values, Appraisals, and Timing

Homeowners often hesitate because they worry about a potential market correction. While national headlines can be alarming, the local reality in West Michigan tells a different story. Portage is currently a very competitive seller’s market, with properties often selling in as little as 10 to 24 days. Using home equity to consolidate debt in Portage MI is a move backed by this regional strength. When demand remains high and inventory stays low, your home’s valuation rests on a much more stable foundation than properties in less sought-after regions. This competitive environment ensures that your appraisal is likely to reflect the true, robust value of your investment.

Timing your consolidation depends heavily on your specific neighborhood and the local school district’s reputation. The Portage Public Schools district continues to be a primary driver of property value, ensuring that even if national trends fluctuate, our regional pocket remains desirable. Working with a lender who understands these local nuances is vital. They can help you determine if your home’s current valuation provides enough lift to cover your liabilities while maintaining that necessary 20% equity cushion. It is about finding the right window of visibility to ensure your long-term safety.

Navigating the Portage Appraisal

The appraisal is the moment where your financial flight plan meets reality. Local appraisers in Kalamazoo County look closely at recent sales in established neighborhoods like Woodbridge or Haverhill to determine your home’s worth. To prepare, ensure all minor repairs are completed and your home is presented in its best light. Document any recent upgrades to your mechanical systems or interior finishes. If an appraisal comes in lower than expected, don’t panic. A seasoned navigator can help you review the data or suggest a different loan product that might better fit your current equity levels.

Proposal A and Your New Payment

Michigan’s Proposal A is often a source of confusion during a refinance. Some worry that a new loan will “uncap” their property taxes, leading to a massive payment spike. In reality, a refinance or cash-out loan is not a transfer of ownership, so your taxable value remains capped. It is essential, however, to verify that your Homestead exemption is active to keep your primary residence taxes at the lowest possible level. Jeremy Drobeck – Treadstone Mortgage provides the local insight needed to navigate these tax nuances without disruption. Check your Portage home’s consolidation potential today.

Preparing for Takeoff: How to Start Your Debt Consolidation Journey

Transitioning from financial theory to tangible savings requires a disciplined approach to your application. While the previous sections detailed the mechanics and math of your home’s value, this final stage focuses on the precise steps of execution. Successful execution of using home equity to consolidate debt in Portage MI depends on your readiness to move through the final checklists. By organizing your documentation now, you ensure your file moves through the system without hitting unnecessary holding patterns or administrative delays.

The first step is a thorough inventory of your current liabilities and an honest look at your credit health. Your credit score acts as your clearance for takeoff, determining your eligibility for specific programs like fha loans michigan or conventional refinance mortgages. Once you have a clear picture of your balances, a consultation with a local specialist allows you to run a side-by-side comparison of different loan structures. After selecting your path, you will lock in your interest rate and initiate the appraisal and title search to bring your new financial plan to the closing table.

The Navigator’s Checklist

Transparency is the most effective way to prevent mid-flight turbulence. When your lender has a complete view of your financial landscape, they can anticipate hurdles before they become obstacles. Prepare a digital or physical folder with your two most recent W2s, tax returns, and pay stubs. You will also need current statements for every debt account you intend to pay off. Setting a realistic timeline of 30 to 45 days from application to payoff helps you manage your expectations and coordinate your final payments to creditors with confidence.

Why Jeremy Drobeck – Treadstone Mortgage is Your Portage Co-Pilot

Experience matters when you are restructuring your home’s most significant liabilities. Jeremy Drobeck – Treadstone Mortgage brings over 20 years of local expertise to every transaction, ensuring that your consolidation is handled with professional precision. Because our processing and underwriting are handled locally in West Michigan, your application remains in the hands of neighbors who live and work in your community. This proximity allows for faster communication and a more personalized approach to complex scenarios that national call centers often struggle to navigate. Schedule your debt consolidation flight plan with Jeremy Drobeck – Treadstone Mortgage today to secure your financial future.

Clear the Runway for Your Debt-Free Future

Your home is more than just a shelter; it is the most powerful engine in your financial hangar. By using home equity to consolidate debt in Portage MI, you can finally silence the alarm bells of high-interest credit cards and replace them with the steady hum of a single, manageable monthly payment. We’ve explored how the 5.2% rise in local home values provides the necessary lift to ground your liabilities and improve your credit utilization. This strategy isn’t just about paying off bills; it’s about re-engineering your cash flow to work for your family’s future instead of your creditors.

Jeremy Drobeck brings over 20 years of local Portage mortgage expertise to your journey. As a division of Treadstone Mortgage with deep West Michigan roots, our team specializes in navigating the complex refinance and debt consolidation scenarios that larger, distant lenders often overlook. We’re committed to being your co-pilot from initial application through final funding. Start Your Debt Consolidation Flight Plan with Jeremy Drobeck today. You have the equity and the plan; now it’s time to take off toward the financial freedom you deserve.

Frequently Asked Questions

Is it a good idea to consolidate debt with home equity in 2026?

Consolidating debt with home equity is a strategic choice in 2026 if your monthly budget is stalled by high-interest credit card rates that often exceed 20% APR. With Portage home values having increased by 5.2% over the last year, many local families have the necessary equity to swap expensive “drag” for a lower-interest mortgage payment. It is a smart maneuver for those who have a disciplined plan to avoid running up new balances after their cards are cleared.

How much equity do I need to consolidate debt in Portage, MI?

Most lenders in Michigan require you to maintain a 15% to 20% equity cushion in your home after the new loan is finalized. For a cash-out refinance, this typically means your total loan amount cannot exceed 80% of the home’s appraised value. If your Portage home is valued at the local median of $320,000, you would generally need to keep at least $64,000 in equity to qualify for the most favorable terms.

Will consolidating debt with a mortgage lower my credit score?

You might see a minor, temporary dip in your score due to the initial credit inquiry, but the long-term impact is usually a significant boost. By paying off several high-interest credit cards, you drastically lower your revolving credit utilization ratio, which is a major factor in your credit health. Most homeowners find that their score gains altitude quickly once the single, manageable mortgage payment replaces multiple maxed-out accounts.

What are the risks of using a Cash-Out Refinance for credit cards?

The primary risk is that you are moving unsecured debt, like credit cards, into a loan secured by your primary residence. If you encounter financial turbulence and cannot make your mortgage payments, your home could be at risk of foreclosure. It is vital to ensure that your new monthly “flight path” is comfortably within your budget and that you have addressed the spending habits that created the initial debt.

Can I consolidate debt if I have a low credit score in Michigan?

You can still explore using home equity to consolidate debt in Portage MI even if your credit score isn’t perfect by looking into an FHA mortgage. These government-backed programs often have more flexible credit requirements than conventional loans. While a lower score might result in a slightly higher interest rate, the savings compared to 24% APR credit cards are still substantial enough to provide significant financial lift.

How long does the debt consolidation loan process take in Portage?

The journey from your initial consultation to the final payoff of your creditors typically takes between 30 and 45 days. Because we utilize local processing and underwriting through Treadstone Mortgage, we can often navigate the process more efficiently than large national banks. This timeline includes the time needed for a local appraisal, title search, and the mandatory three-day right of rescission period required for most refinance transactions.

Are the interest payments on a debt consolidation mortgage tax-deductible?

Under current 2026 tax laws, interest paid on home equity debt is generally only deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. If you use the equity to pay off credit cards or personal loans, the interest is typically not tax-deductible. You should always consult with a qualified tax professional in the Kalamazoo area to understand how these rules apply to your specific situation.

What happens if my Portage home appraisal is lower than expected?

If your appraisal comes in low, we don’t necessarily have to ground your flight plan; we simply adjust the coordinates. We can look at reducing the amount of debt you are consolidating or check if a different loan product allows for a higher loan-to-value ratio. In a competitive market like Portage, we can also request a reconsideration of value if there are more recent comparable sales in your neighborhood that the appraiser missed.

Latest Blog Post

Conventional vs USDA Loan Michigan: Your 2026 Mortgage Flight Plan

The “obvious” choice for your mortgage might actually be the most expensive path if you don’t account for the unique terrain of the West Michigan housing market. While you might assume a massive down payment is the only way to avoid financial turbulence, comparing a Conventional vs USDA Loan Michigan reveals that the right flight plan often involves much less upfront cash than expected.

We understand that staring at a map of geographic eligibility or weighing monthly mortgage insurance costs can feel like flying through heavy fog. It’s frustrating when you’re ready to move but feel grounded by confusing requirements. This guide will help you compare these options with the precision of a seasoned navigator. You’ll learn how to identify if your dream neighborhood is USDA-eligible, how the 2026 loan limit of $832,750 impacts your Conventional path, and how the $119,850 income limit affects your USDA eligibility. By the end of this flight plan, you’ll have the expert coordinates needed to choose a loan that offers maximum lift for your West Michigan home journey.

Visit Jeremy's Blog